>100% growth at 9x earnings... Does it last?

A unique pharma producer with rocketing sales, and unanswered questions.

Bioxyne Limited

Ticker: BXN (ASX) Price: AUD 0.045

Fully Diluted Shares Outstanding: ~2.23 billion

Market Cap: 100 mAUD (~65 mUSD)

Net cash: 6.7 mAUD

Overview

Bioxyne is an Australian pharma co making medicinal cannabis products (pastilles, flower, vapes, oils). They make their own brands and ~200 private label brands (e.g. for pharmacy chains).

The company also holds Australia’s first GMP licence for MDMA and psilocybin, and is providing these drugs to hospitals as part of medical trials.

It’s interesting because

They grow >100% p.a. since 2022, within a fast-growing medicinal cannabis market. Revenue grew from 2m in 2022 to ~65–75 mAUD in FY26 (guidance).

Strong execution across each of their pillars for success.

The team has built an efficient GMP production facility, pioneered new product categories like pharmaceutical cannabis gummies, and is working with regulators to expand sales into Germany, the UK and LatAm.Shares are undervalued at ~8x FY2026 earnings. At 100 mAUD market cap and 6.1 mAUD net cash, the stock trades at ~8x our FY2026 net income estimate of ~12.5 mAUD. For a company growing revenue at 100%+, this looks cheap.

MDMA and psilocybin provide future upside not in the price. Bioxyne has fulfilled 400+ patient doses for clinical trials. Revenue is sub-1 mAUD today, but the global psychedelic therapy market is projected at 14 bUSD by 2032. This is free optionality.

What do they do?

Bioxyne operates across four segments:

Australian medicinal cannabis (~29 mAUD FY25 revenue)

Manufactures pastilles, flower, vapes and oils on a B2B/CDMO basis for ~200 private label brands and pharmacy chains.International CBD (~1.5 mAUD FY25)

Six years of UK/European presence through the Dr Watson wellness brand, with a 78,000-consumer database. Provides distribution infrastructure for the medicinal cannabis push.International medicinal cannabis (0 mAUD FY25, ramping in FY26)

Exporting GMP flower to Germany (~6 mAUD initial contract with Farmakem/ADREXpharma, 2.9 mAUD invoiced Q2 FY26) and the UK (~2.5 mAUD first shipment). Flower is 95% of the German market. Management aspires to ship ~10 tons to Germany in 2026 at ~2–2.5 AUD/gram. Czech and Scottish facilities in development.MDMA and psilocybin (<1 mAUD FY25 revenue)

Holds Australia’s first GMP license for both substances. 400+ patient doses fulfilled for clinical trials and authorized prescribers. 5–10 year horizon for significant scale. The global psychedelic therapy market projected at 14 bUSD by 2032.

History and leadership

Sam Watson has founded what the company now represents, and has listed it through a reverse merger in 2023.

Sam and other insiders collectively hold ~60–65%, and have quickly grown the revenue, the capabilities and the relationships of the company over the past years:

Feb 2024: Obtained Australia’s first GMP license for MDMA and psilocybin

Aug 2024: First pharmaceutical cannabis gummies under TGA GMP

Aug 2024: Increased gummy capacity by 3x

FY2025: Revenue 30.4 mAUD (up 216%), first profitable and fcf positive year

Aug 2025: FY26 guidance of 65–75 mAUD revenue, 11.5–13.5 mAUD EBITDA

Q1 FY25 (Sep 2025): First contract from Germany (5 mAUD)

Q2 FY26 (Dec 2025): Record 17.2 mAUD quarterly revenue (p&l to be posted)

Nov 2025: Received permit for UK factory (want to copy paste Australia)

Dec 2025: Released MDMA capsules for clinical trials (PTSD treatment)

Dec 2025: 1 mAUD agreement with customer is LatAm

Feb 2026: Hired UK plant and Quality manager

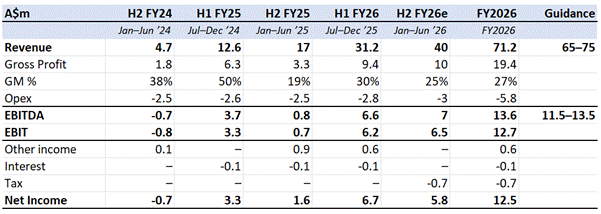

Financials

Bioxyne has so far reported FY 2025 (July 24 - June 25) statements, and has shared their FY26 H1 revenue and cash flow report, in true Australian style.

FY2026 (Jul ’25–Jun ’26): I use H1 FY26 actuals and estimate ~40 mAUD H2 revenue based on management’s 65–75 mAUD guidance. For the rest of the P&L I use current opex growth rates, factoring in some operating leverage as Australian facility is now fully operational. I used a lower gross margin for H2 (25% vs 30%) as I expect a larger share of revenue to come from the lower-margin international flower segment.

This gives ~71 mAUD revenue, ~14 mAUD EBITDA, ~12.5 mAUD net for FY2026, just above guidance: 65–75 mAUD revenue, 11.5–13.5 mAUD EBITDA. In 2025, Bioxyne delivered revenue more than ~10% above guidance.

Competitive advantages

Cost advantage. BXN sources from >20 cannabis growers globally, and has built the world’s largest medical cannabis gummy facility, in the worlds most cost competitive Cannabis production country.

Strong product development. BXN pioneered pharmaceutical cannabis gummies under TGA GMP. Pastilles went from 4.8% to 25%+ of Australian cannabis prescriptions in a year.

Global footprint. The Australian facility is EU GMP certified, enabling direct supply into Europe, UK, Canada and Singapore. New facilities in the Czech Republic and Scotland will bring manufacturing closer to European customers.

International expansion

The company is taking its first steps into international markets, most importantly Europe, using the supply network of their currently unprofitable CBD business:

Germany: ~6 mAUD supply agreement with Farmakem/ADREXpharma for 1,600kg GMP flower. 2.9 mAUD invoiced in Q2 FY26. The German market is €1B+/year with 1m+ patients. Flower is 95% of the market, probably making it a low GM% market over time.

UK: ~100,000 patients today, expected to reach 420,000 within two years. First medicinal cannabis shipment was ~2.5 mAUD

Other EU: Czech facility and Scottish facility in development, reducing lead times from the current 2–8 weeks for export/import permits.

Warning

What really annoys me here, is the lack of follow-on announcements related to Germany. The company has not detailed guidance across segments, but their inventory comments in the Q2 report suggest they want to ship ~10-15mAUD in products into Germany in H2 FY26. Reaching that would mean they are currently shipping follow-on orders, but a press release confirming that is missing.

Valuation

At 100 mAUD market cap and 6.1 mAUD net cash, BXN trades at ~8x our FY2026 net income estimate of ~12.5 mAUD.

Applying a 13–15x ex-cash P/E to those earnings puts fair value at 169–194 mAUD market cap, or AUD 0.076–0.087 per share. That’s 69–93% upside from today.

Risks and unknowns

Australia’s medicinal-only focus

Australian regulations restrict BXN to medicinal cannabis. If European countries change regulations to fully allow cannabis, then Bioxyne will actually no longer be allowed to export from Australia. The UK factory will be up in a year though and will mitigate this.Competition

Although Bioxyne has built a nice pastilles business, the competition in the cannabis sector is ruthless. There’s too many competitors to name, and they are all setting up GMP facilities in Europe to chase the 100-200% growth seen in key countries. I think their current Australia business is relatively safe, but the international expansion is hard to predict.Growth in Germany?

Bioxyne has supplied ~5 mAUD worth of medicinal cannabis to the German market in H1 2026. We don’t have any visibility on continued orders, although German Dr. Watson product reviews are solid, and the Q2 comments about new German regulations pushing products through pharmacy chains instead of e-commerce are very positive. I just don’t understand the lack of PR here.European gummies?

Although gummies are a natural form for medicinal cannabis, none of the European countries has allowed them so far, leading most “patients” to smoke their cannabis. Allowing gummies would provide an amazing opportunity for Bioxyne to use the expertise they have built up.

Other European countries and the USA

Several countries are moving closer to a clear framework on medicinal cannabis, providing potential (long term unavoidable) TAM growth for Bioxyne.

Summary

Sam Watson is growing Bioxyne into a unique pharma player, leading the way in medicinal cannabis, mdma and psylocybin. The company will reveal it’s earnings next week, and I think its very cheap at ~8.0x FY2026 earnings.

I think these earnings will have a positive impact on the stock, but further success will depend on positive evolution of their international business, in particular continued demand and follow on orders in Germany.

If the story continues, to be confirmed in the call on 26th of February, then the growth at high ROE can be valued at 13–15x earnings, or AUD 0.076–0.087 per share, or 69–93% upside vs todays price.

Disclosure: Long but keeping a very close eye and might change position quickly if for example Germany turns out to be stalled. Please check out the company before investing.

Disclaimer: This publication’s authors are not licensed investment professionals. Nothing produced by the Floebertus team should be construed as investment advice. Investing involves serious risks, including risk of capital. Do your own research before investing, and size your positions appropriately, in line with your own conviction and your own knowledge.

This is a very risky bet because everything may change on a butterfly effect.But upside is there.