2025 Performance (+123%) & 2026 Portfolio

Hi everyone!

Welcome to our first end of year review. Today’s update aims to give you a good view of what happened last year, and share the portfolio entering the year (updated for mid January).

If you have questions on some of the positions or the thought process, don’t hesitate to reach out. We will cover:

2025 review

Overall performance

Main winners & losers

Corresponding insights & mistakes

2026 portfolio

Positions and rationale on Jan 1st

Update as of Jan 17th (after rebalancing)

Watchlist

2025 Review

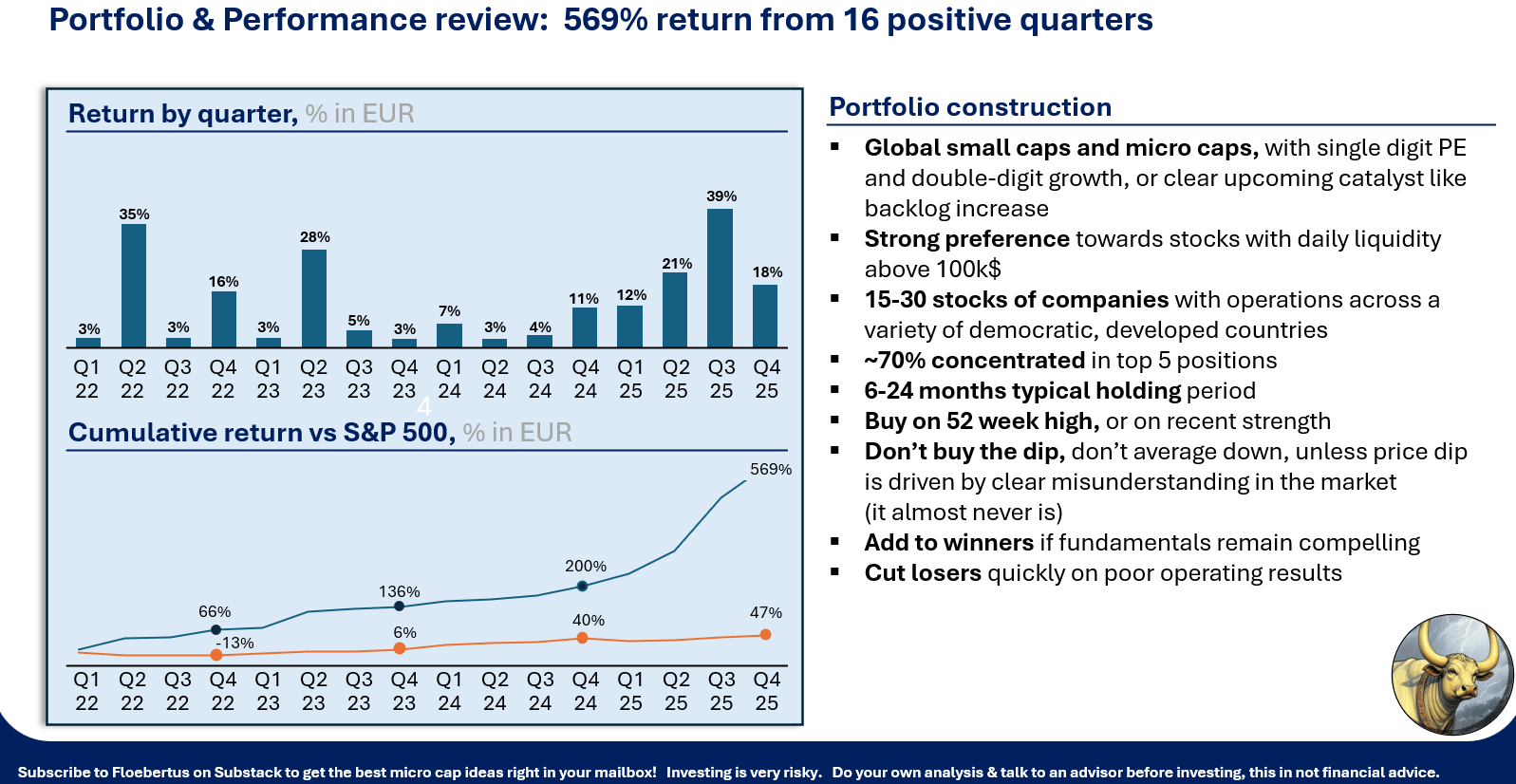

The portfolio did exceptionally well in 2025, with a 123% return across the positions. It was great to scratch a 100% return year off the bucket list, but we should not expect this to be repeatable (of course haha).

Looking at the past 4 years, it’s becoming clear that we have a big advantage. We have the privilege to invest in exceptional companies which are too small for institutional investors to research, and this enables us to get exceptional returns.

The thesis on some of these investments is very interesting, for example OKP Holdings being primed to win most of Singapore’s upcoming tenders for its large cycling path expansion. This type of thesis is where we can really go deep and build unique insight. (at the time of the write-up)

Others are very simple, for example Soilbuild just winning a huge order book of tenders, or Huationg already having the order book and showing clear hiring (based on LinkedIn figures) to execute on it. These are situations where scouring through annual reports and filings across a huge universe of companies, leads to finding a few with a clear advantage and a very plain thesis.

Whatever the complexity though, the goal is to stack returns here. We don’t have to get too cute if it’s not needed. This has worked pretty well over the past 4 years.

Notice that the chart starts at Jan 1st, 2022. Before that, we were focused on large- caps and consistently underperformed the S&P500. We came to respect the efficiency of the large-cap market, and the strength of the US economy. This is why we still like to compare our performance to the S&P, rather than MSCI World.

Beating the index in large-cap stocks is hard because you’re competing with ~1000 analysts at the big banks teaming up to find and resolve market inefficiencies.

In small and micro-caps though, they can’t participate because their wallets are too big to step in and out of small companies/stocks. As said, this is where we have an advantage, and we think this advantage will remain there for the coming years.

Winners

The biggest winners in 2025 are below, showing the positions contributing more than 1% of the overall 123%.

We recognize 3 main groups

Singapore construction +42%

Some of the most economically favorable countries, and best ran countries in the world, have extremely low stock market valuations. The world has forgotten them. Prime examples of this are Poland and Singapore. In Singapore, construction is set to do well in 2025/2026/2027, as the country awarded record projects in 2025 at ~53 bn SGD. The many micro-cap construction companies in the country are seeing their growth and margins rebound after the post covid slump.

Gold miners +38%

As described in the November 2025 update, and in the Serabi write-up, the price of gold has gone up so quickly, that small mining stocks could not keep up and provided a large opportunity while catching up and doubling in slow motion.

The slow motion was driven by the lack of investor appetite for mining stocks, the large operational leverage (making profits rise faster than revenues) and rebalancing of existing investors leading to large sales.

We have become a participant in the rebalancing, reducing gold miner exposure from ~55% to 35% in December 2025. At some point, this is needed, and it just shows again why the opportunity exists.

Clearly, the rise in gold prices has helped a lot here. This was luck, but also matches earlier patterns. As we can see below, in the past 25 years, once gold started a run, it has typically continued for a couple years. Double digit returns follow double digit returns. The current run might be getting a bit long lived though.

Gold vs USD since 2000 Other Hyper-growers +13%

In a sense, almost all the companies in the portfolio in 2025 were hyper-growers. Companies growing >30%.

These are often companies which deliver such good results, that the market needs several quarters to realize, digest and price in the good news. These will often share increasingly good news along the way, providing existing investors the opportunity to buy more at higher prices but cheaper valuations along the way.

A hyper-grower isn’t typically a better investment than a value stock, but does more often trade inefficiently, just because it is changing more rapidly (in revenue/profitability), because it’s hyper-growing…

Next to these themes, there were some other smaller one-off wins:

Matsa Gold, trading well below the value for which they will very likely sell the Devon Pit to AngloGold Ashanti. This investment was like a merger arb, although it wasn’t the whole company that was being sold.

DBA Group, trading at 4-5x owner’s earnings, hidden behind amortization of goodwill related to past acquisitions. The extra cashflow hiding behind this amortization, will not show up in earnings soon, but does allow the company to acquire small companies representing ~5-10% extra revenue growth every year.

Zoomd sentiment became so bad, it had sold down to 3-4x earnings at 70% growth. This was mainly driven by tariff fears. Some investors in 2025 acted like we didn’t already have a tariff scare in 2018. We were lucky to pick up some shares around the Q2 bottom.

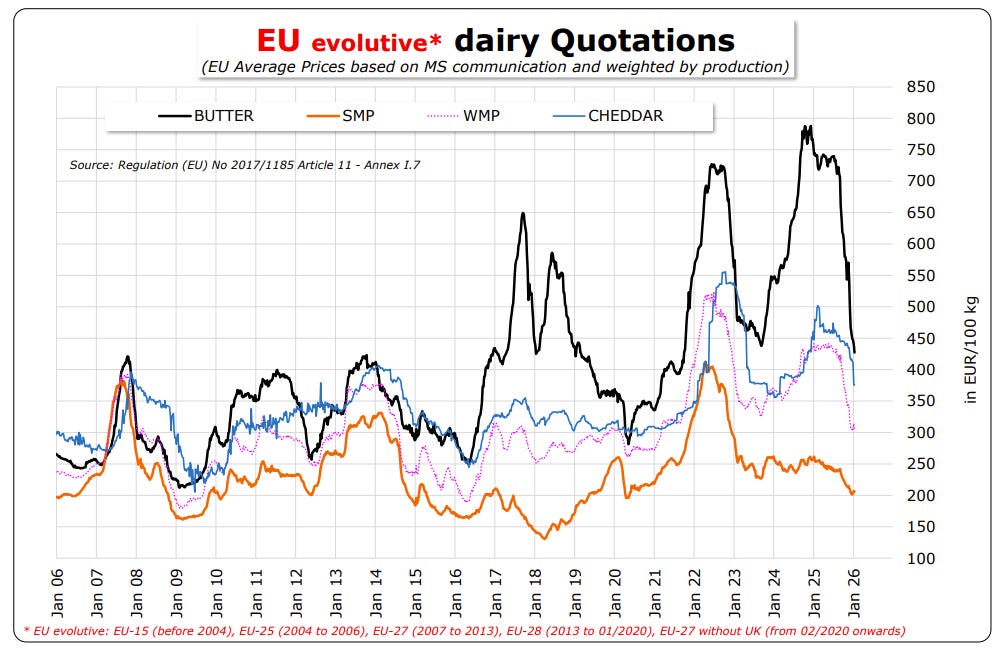

Vilkyškių Pieninė. Throughout 2024, prices of dairy commodities (cheese, cream, protein powder) rose significantly in Europe. This was mainly driven by rising prices of raw milk in many European countries. The rising milk prices were caused by years of unfriendly government policies towards European farmers (Nitrogen policy, etc…) and global warming reducing milk yields in Southern Europe, making the supply side fragile while demand increased significantly.

In the Baltic countries though, milk prices didn’t rise much at all. In fact, the government there is proud and supportive of the dairy sector. The dairy sector also doesn’t create much environmental harm as the region is much less densely populated. Baltic dairy yields were not impacted by global warming at all, the local climate is much colder.

Raw milk cannot be shipped internationally because it goes bad in 24-48 hours, explaining the differences in national milk prices. Cheese, cream and other products though, have 1-12 month shelf life, and therefore exist in a global market.

This created a big advantage for Baltic dairy processors (cheese producers).

They saw rising pricing power in the European market, but with flat input costs at home in the Baltics. This led to large margin expansion for the Baltic cheese producers like Vilky, which the market only caught up on as results were getting reported in H2 2024 and H1 2025.

We’re surprised these companies stocks are not falling, as cheese and butter prices have come back to earth, and the spread between Baltic and central European milk prices has normalized in the past ~6 months.

European prices of dairy commodities (Source: European Commission)

Before closing on the winners, we have to make an honorable mention of Intellego of course. The company recently turned out to be probably mostly fake.

We first heard about this company in ~2022. They seemed like a scam. Almost nothing on LinkedIn, strange product, and most customers based in China. We decided not to take a position.

In the ensuing years, Intellego grew very quickly, providing clear guidance, delivering on the guidance, having insiders buy shares, having a large deal with Henkel, finally taking Deloitte as their accountant…

We decided to take a small ~2-3% position at ~7x forward earnings in early 2025. Shares had just sold off after weak Q3 2024 earnings, but management was buying shares and raising 2025 guidance.

As expected, management bought more stock at the Q3 post earnings dip, and the stock quickly doubled (2-3x) in a couple of months, after which we sold most of the position. There’s no point holding such a strange company at 20x earnings.

Recently, it turned out that Intellego very likely is largely a fabricated accounting scam, and the remaining 0.5% position will likely get written off.

We think the lesson here is to be much more careful when a companies ecosystem is not clearly visible (employees, customers). Especially if the employees are not visible, that’s a big red flag.

Even if Deloitte is the auditor, if the CEO is buying stock, and if large FMCG are lining up as customers… Employees (on LinkedIn or media of corporate events) are the hardest to fake…

Losers

Now that everyone has dropped off after the lengthy discussion about cheese and butter, we can talk about the losers and the mistakes.

A mistake, is where the standard process is not respected or fails. This should be analyzed and should lead to increased execution discipline, or process improvement.

A loser though, is where money is lost on a position. If the process was followed, we should not be too harsh on losers, as they are unavoidable.

We should look at the losers to find mistakes and process improvements, although not forget that Intellego for example, was a mistake as well, although it was a profitable one.

Below is an overview of the losers in 2025:

Going through:

Simply Solventless fell about 50% in June 2025, upon announcing changes in accounting treatment of part of their revenue recognition and part of their expenses.

The company had been recognizing part of its incoming raw material shipments as revenue (!) because they were handling the shipment from the supplier. They also had been capitalizing too much of their production overhead into inventory, making operating expenses look lower…

Both of these are not only completely unacceptable, their correction also showed a company that was much less interesting and will likely not win the fierce competition for the Canadian cannabis consumer.

BIG MISTAKE to buy this with >1y inventory on hand being an agricultural products company. Clearly something was wrong. Good to realize it immediately and get out at ~21 CAD ct versus today’s ~11 CAD ct.LGI Homes and Excellence sa, where not really mistakes but did go down a bit due to volatility. Both have meanwhile recovered. We sold Excellence for the multi bagger in Zoomd and bought more LGIH on the dip making it a nice contributor for 2026 so far. Can’t really call either a mistake.

4Mass reported a string of bad results in 2025. We think what happened is they moved from hypergrowth mode to normal mode, and this changes 2 things:

First, investors give the stock a lower multiple as it’s not growing extremely fast anymore

Second, retailers are not begging the company for product, because all the shelves are full and shortages have been mitigated. The retailer then turns around and starts asking for discounts, while looking for alternative competitor or private label products

This creates a double whammy for the hyper-growth company seeing growth, margins and P/E multiple decline. We should expect this to happen and should keep an eye on BSH as a potential victim of this phenomenon in 2026. So far BSH’s car products seem to attract limited local competition though, but this is certainly something to keep an eye on.

Important to remember here that well-filled shelves, and supply matching up to demand, can shift the balance from producer to retailers.

2026 Portfolio

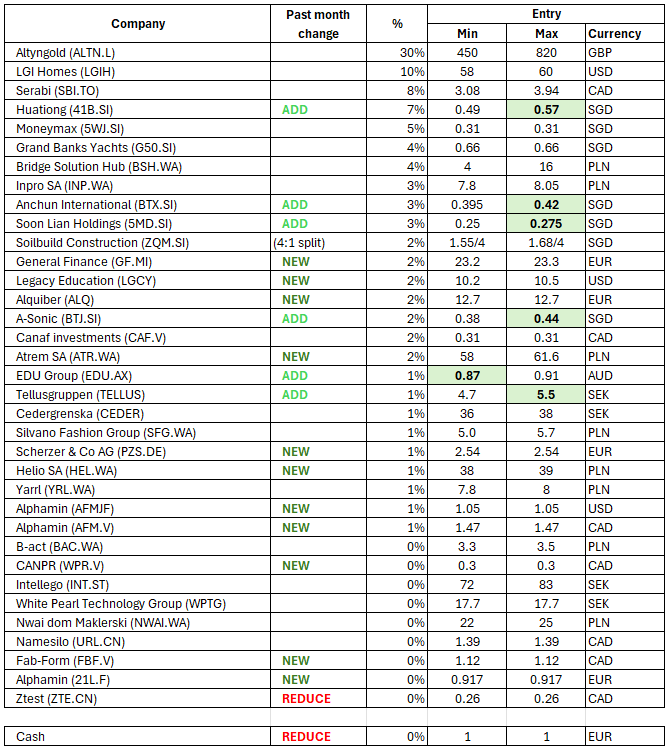

Below is the current portfolio mid January.

There’s a lot of information on many of the positions in the review of the 2025 write-ups, and the latest thoughts on many of them are covered here:

Anchun and A-Sonic were covered in the “Appetizers” post on January 1st. We were a bit wary writing about them as they only have ~10k$ liquidity, but after the post, they didn’t move at all. So we bought some more using increased conviction after writing the post on both of them.

Other ADD/NEW positions not covered in the posts above. We’re still increasing our understanding and knowledge on many of these:

Soon Lian Holdings. This small company delivers Aluminum parts to the semiconductor industry and mentioned datacenter demand as a tailwind in early 2025. We think they trade below the value of the Aluminum they have on their books (estimate), and they consistently do well in periods of high demand for semiconductors and Aluminum. (because of FIFO and because high prices often indicate high demand). We think their earnings will roughly double in 25H2-26H1 vs year before, to where they were in 2021-2022. It’s not a very transparent company but it trades below 5x earnings before this (potential) tailwind.

General Finance. This Italian receivables factoring company is building a multi-year track record of >20% growth, far outpacing competitors. We think management is just running a very tight ship, running the business in a very effective way, and taking every opportunity in earnings calls to differentiate themselves from competition. We used to own a small position in early 2025 at 15 EUR but let it go for one of the Singapore names. Happy to come back to General Finance much higher, but still trading at ~10x 2026 earnings with ~30% growth. The track record, the investor presentation and the earnings call make us think they really know what they are doing.

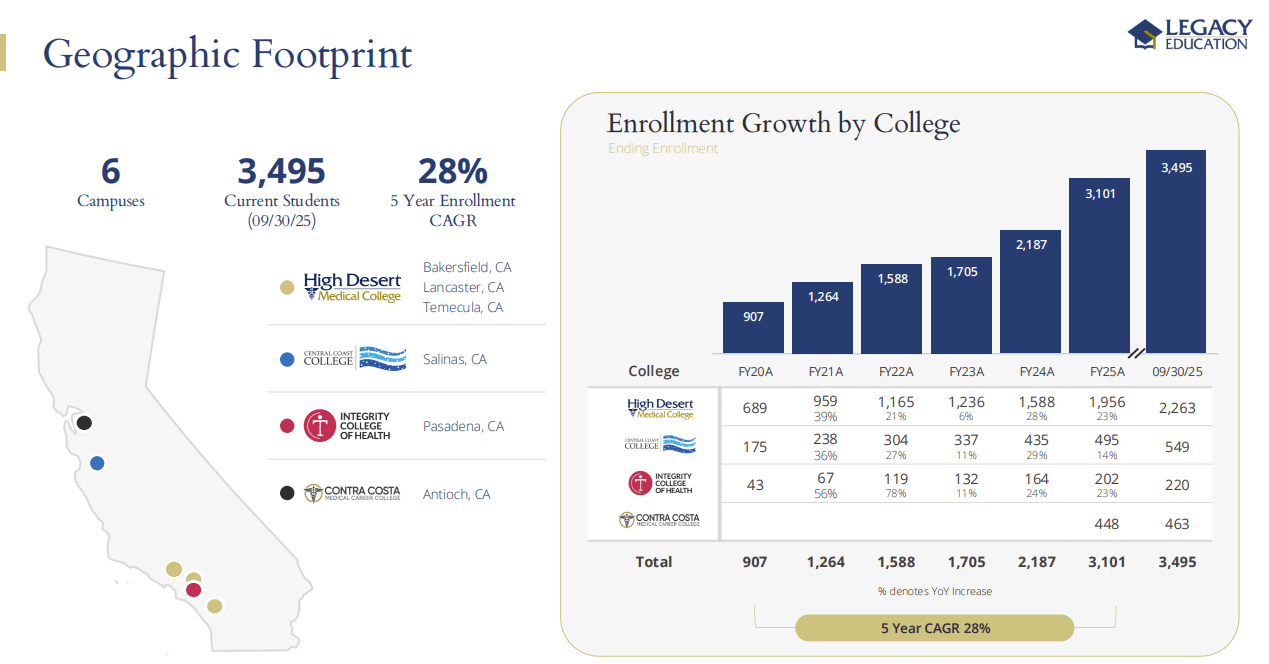

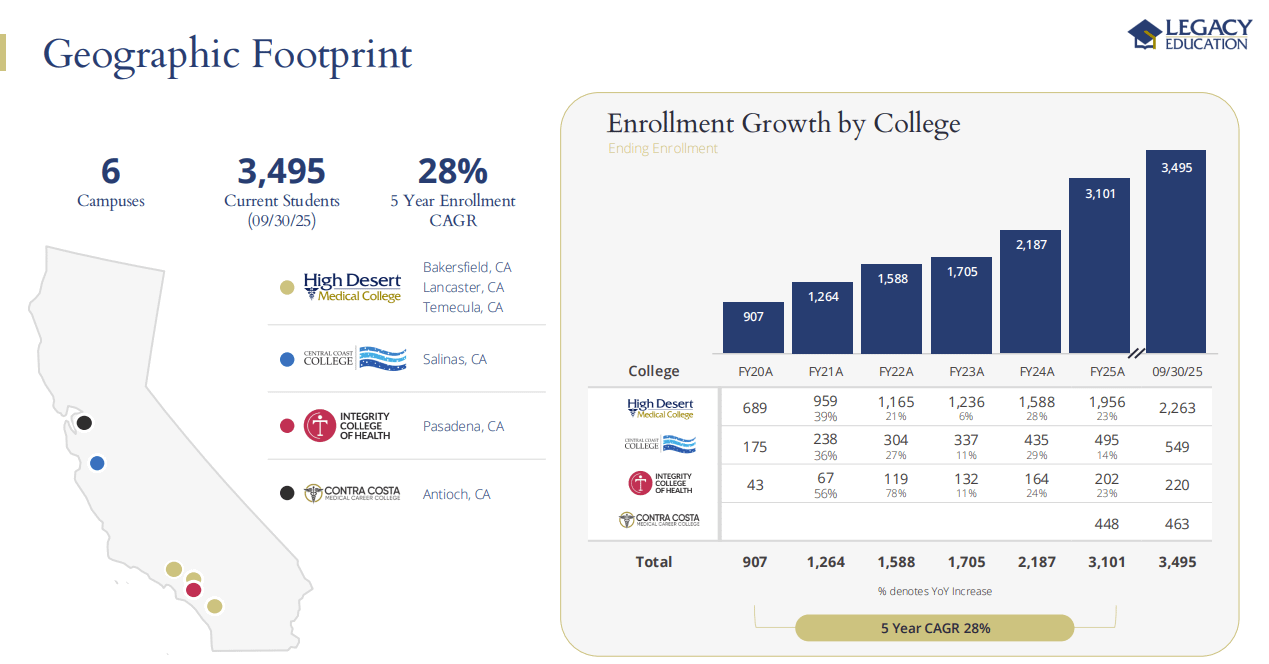

Legacy Education. With education companies, we get a good preview of next 12 month results, because we can see school enrollment. LGCY is a California nursing school, in which organic enrollment has grown 19%, through the introduction of new classes and courses.

(Organic ending enrolment was (3495-463) for 30/09/25 vs 2539 for 30/09/25.)

Legacy Education Enrollment growth While revenue in Q1 2026 (Sept) grew almost 40%, net income was stable due to higher operating expenses (~1% bad receivables, higher management comp, one-off expenses to start the year with extra school equipment, post merger integration… ).

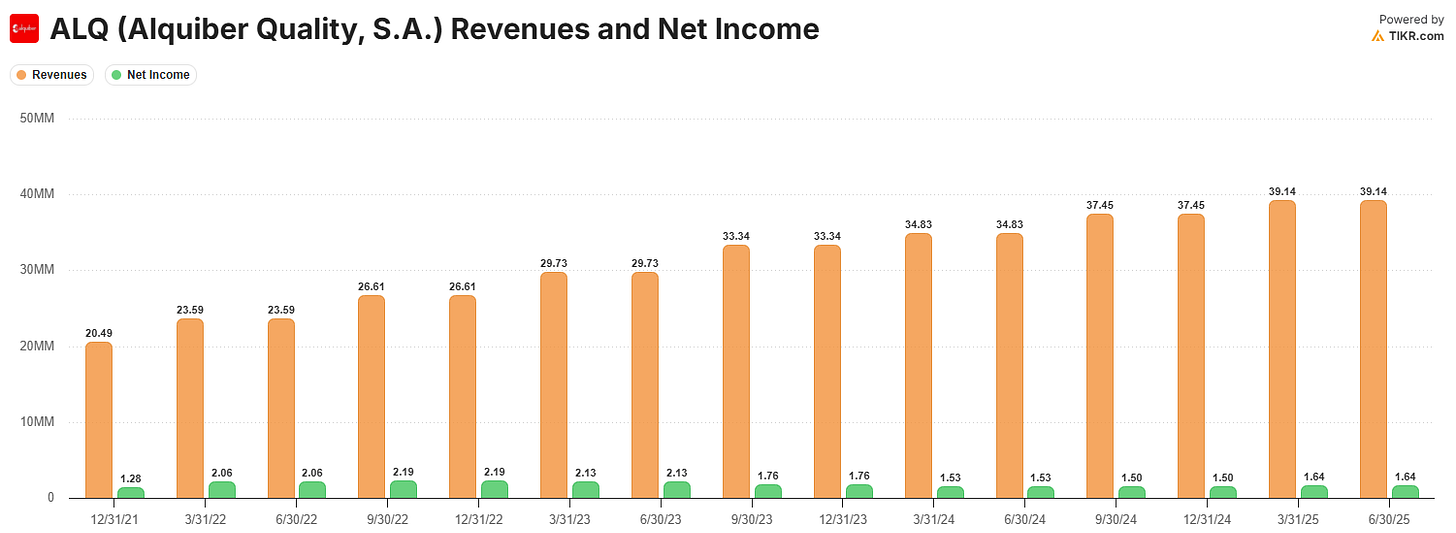

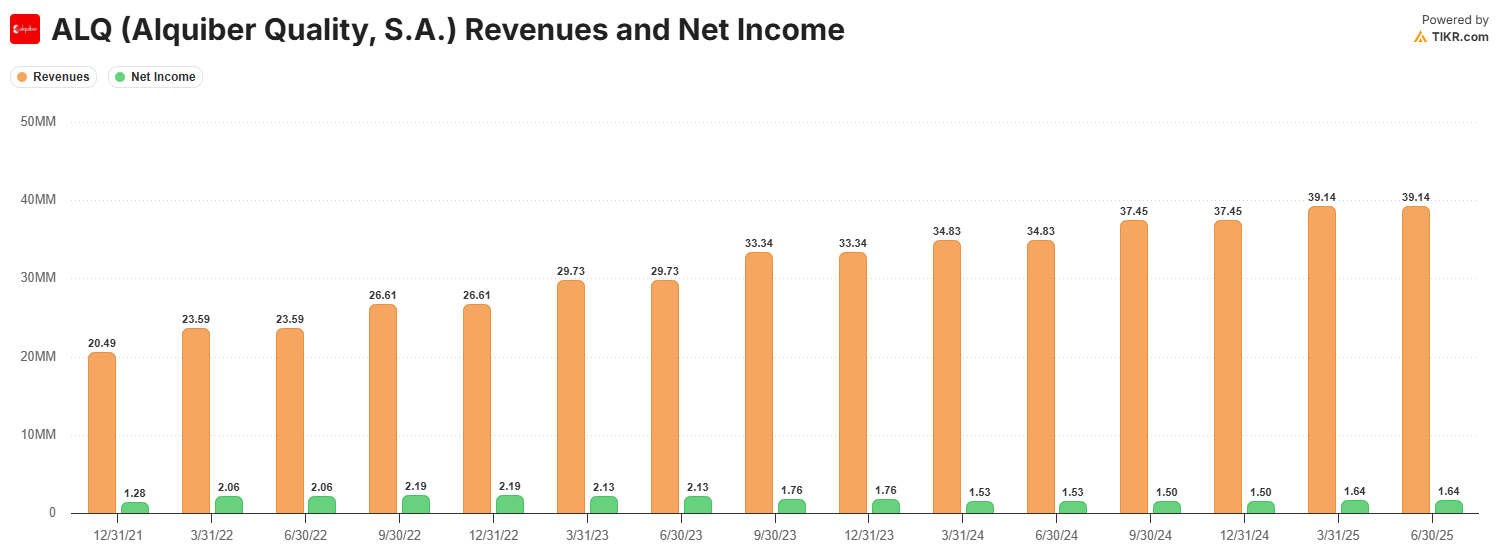

Management suggested margins will expand through 2026 but the market didn’t really like the results. We did like this at 10-15x 2026 CY earnings for a US company with 6 years of double digit growth serving an aging demographic and actually doing something good for the world.Alquiber Quality is a very consistent Spanish car leasing company which has grown 15-25% per year for many many years. They have entered the Italian market recently which we think together with the shift to EVs, will lead to a growth acceleration, offsetting slightly higher interest expenses caused by rolling their large debt. This is not going to be a shocking stock, but is a very consistent performer typically.

Alquiber’s Revenue & Profit evolution Atrem is a Polish (electrical) engineering company which is benefitting and will continue to benefit from every big trend out there. (AI, energy transition, the Polish investment package from the EU, …). We think they grow revenue 30-60% in 2026, and will keep a very strong growth trend beyond that as well, justifying a slightly higher 15-20x forward fair value P/E multiple.

Helio sa is introducing healthy snacks in Poland, and recently pre-announced that Q4 2025 was their 3rd consecutive quarter of >30% revenue growth. The company trades at ~10x earnings and is regularly buying back stock and paying dividends, while investing in organic expansion. Recent growth is largely driven by increased sales of packaged dried fruits, produced on new equipment, which is still being optimized before bringing its full margin contribution.

More on Atrem, Helio, BSH and Yarrl here:EDU Group & Tellus Gruppen are both private schools as well, but not comparable to Legacy Education given the large regulatory risk embedded in both of these.

EDU: Australian school based on immigration for education. We need to brush up the calculations a bit before sharing them, but their T3 2025 student enrollment, and 2026 price increase suggest 25-40% growth in 2026 at a 5x P/E multiple on 2026 earning.

That sounds crazy cheap, but the Australian Labour Party (which provides the minister of education) seems to want to partially ban or scale down their immigration based system.

The recent events on Bondi beach may provide the minister with the necessary momentum to finally pass a law on capping education driven immigration.

We think the likelihood of a material adverse impact is ~40%, making this a very risky bet. If adverse policy doesn’t come, EDU’s profit and P/E multiple likely both double in the next 3-4 years.Tellus Gruppen is a Swedish school like Cedergrenska, but a bit smaller. Shares are even cheaper than Cedergrenska at ~3.5x TTM owner’s earnings, and they actually grow 2-3% organically. The company has funded a 2023 or 2024 acquisition with debt and shares + warrants, expecting to re-pay some of the debt from the warrant income. As the warrants have expired worthless in Dec 2025, they are sitting on ~25m SEK short term liabilities which we don’t think they can repay from operating cash flows. Likely a new debt or shares placement is coming. If it’s shares it might move them to 4x P/E, but they will still appear underpriced.

Scherzer & CO is a German special sits and micro-cap investing company buying back shares at 70% of NAV. They are buying back their own stock aggressively, potentially forming a rising floor under the stock.

Alphamin is a well-known producer of tin, which is used mainly in solder and electric vehicles. The price of tin rose aggressively over the past days, elevating Alphamin’s 2026 potential profits.

It’s sitting below 3x 2026 profits at current Tin prices. Since entry into this position last week though, tin is down ~12% in a short term correction. We will get out of this position, if in the coming weeks, the uptrend in tin is not shown to clearly resume to new highs, or if we find a better stock to participate in the upside in tin.

CanPR and Fab-Form, 2 tiny new positions

CanPR is a growing platform for Canadian immigration with a nice founder with past successful exits.

Fab-Form supplies smart construction products that enable builders to save wood and concrete. It will do well again at some point when construction improve (and lumber prices rise), but it might take some quarters or years.

Sales:

We sold a tiny part of the ZTE position to resolve a tiny negative cash balance due to rounding errors or transaction costs.

Watchlist

The near term future purchases (if any) will likely be additions to existing positions. There’s really nothin better than “doubling down” at higher prices when a company you know well does something amazing.

We’re always looking at new companies, here’s some examples we’re still getting to understand a bit better:

Bioxyne (BLS), Enogia, FSA Group, Porto aviation, Performance Technologies, Profile Systems and Software SA, Soditech SA, Tarczynski, FNM spa, Makolab, Auxly, Cannara, Instabank, Integrated Wind Solutions, Malvern International, Mediazest, Wiseway, DH Group Nyilvánosan, Pasquarelli, Xtant Medical Holdings, Directa sim, Made Tech, Logic instrument, ATC Cargo, DWS (Diamond Estates Wines & Spirits Inc.), YesAsia, Humm Group, Budapesti Értéktozsde Nyilvánosan, Primoco AUV

Be careful, bull market genius

This was another wonderful quarter. We started writing “returns of x positive quarters in small cap investing” a few years ago, and x just keeps incrementing, now to 16.

Please note that while this did happen and all 16 quarters had positive returns, you should read that as a bit of a joke, because concentrated investing as we do, comes with volatility, and no one should expect having positive results over any short-term period, whether it’s days, weeks, months, quarters or years. We’re all getting fat and happy and this is exactly when the market likes to punish investors that stop putting in the work to find and understand the best companies and stocks out there. Take positions carefully and with conviction.

Thank you for reading!

Disclaimer: This is not investment advice, please speak to your adviser before investing, and please do your own work analyzing the company.

Congrats on the great year! Do you use any software to track your portfolio for better reporting btw?

Hi Floebertus, many thanks for this update!

I had a look at General Finance and noticed the following potential red flags, I wanted to ask your opinion about them:

1) CEO controls around 41% of the shares, but has 59% of the voting rights. Are shares with multiple voting rights common practice in small caps or is it something we should pay attention to?

2) A big part of the CEO's shares, owned by his holding company, have been pledged to secure bank loans. Is there a risk of forced selling in case the parent holding gets into financial troubles?

3) There seems to be an open trial from a customer (Leali Steel S.p.A) and a judge ruled General Finance to pay them a compensation of 9.3M plus 4.7M of interests and expenses, although apparently the sentence was suspended in the appeal trial. Do you think this could be a significant risk in case they finally lose in court?