~60% growth in data centers, at ~5x P/E

A micro-cap just posted the most beautiful earnings reports in modern history

Here’s why we like the company we will cover today:

Growth is 58% yoy (H2 2025), driven by data center demand

Backlog is exploding (New orders were 50% above revenue)

Gross margins are increasing (Better mix + operational improvements)

Capacity increases in March 2026, driven by a new factory

Insiders own ~80%, recently raised growth capital at a 5% premium

Stock is cheap at ~5x 25H2 annualized P/E (ex-cash of 30%)

We were following this company for a while and noticed their small capital increase at a premium in Dec 2025, but at that time couldn’t see a great investment case yet.

Let’s dig in.

Lincotrade & Associates Holdings Limited

Ticker: BFT (SGX) Price: SGD 0.29

Fully Diluted Shares Outstanding: 182m Market Cap: SGD 53m (USD ~41m)

Focus

Lincotrade is an interior construction company based in Singapore. They upgrade or build a broad set of residential, commercial and public buildings (from apartments and hospitals, to now increasingly offices and data centers).

The company focuses on 3 segments:

Commercial. Upgrading offices, hospitals and data centers. They improve the overall design, layout, and technical facilities like ventilation, fire safety, air conditioning, cooling…

Residential. Upgrading or building new houses and flats, with a focus on interior design, but also technical aspects like refurbishing buildings to adapt ceiling heights etc…

Show-flats. Setting up attractively outfitted demo flats to drive sales (~ legacy business)

In recent years’, the commercial segment has become very dominant at >90% of revenue, driven by accelerating demand in data centers. This is boosting the company’s overall gross margins, as Commercial has ~15% GM vs ~5-10% in Residential and Show-flats segments.

The “Commercial” projects not only have high urgency, but also have a much larger scale, driving up both pricing power and execution efficiency for Lincotrade.

Management

Lincotrade was co-founded in 1987 by Jimmy (Tan Jit Meng) and Jackie (Soh Loong Chow) who still run it today and have brought it public in 2022 together with millionaire investor Wee Henry and COO Tan Chee Khoon.

All 4 still own their original shares, for ~80% of the company. The rest is mainly owned by retail investors.

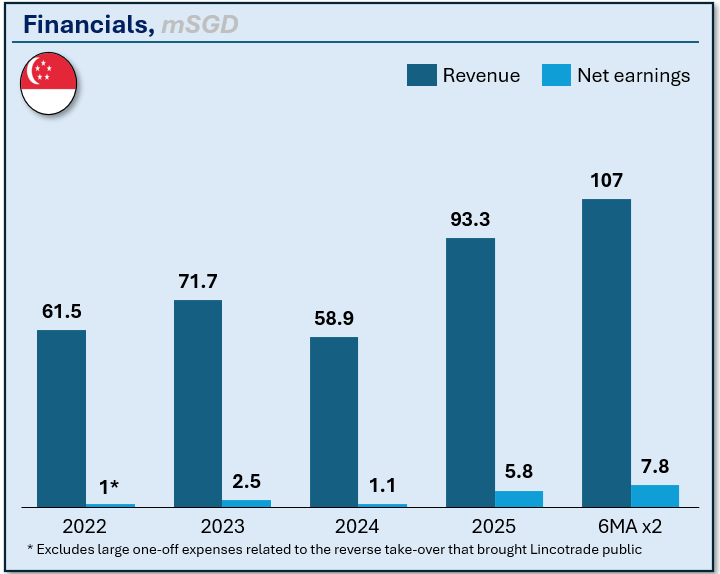

Financials

Lincotrade has been growing very well since IPO, but the recent results show a true growth and profitability inflection, with net income rising >400% in H1 FY26 which we like to just call H2 2025 CY for easy understanding.

That recent growth and profitability look sustainable, given:

Increased pivot towards Commercial projects

Over the past 2-3 years, the company has made a systematic shift toward offices, hotels, malls, and data centers which support the current margins.

New Tuas factory to enable the growth

As of March 2026, Lincotrade plans to relocate their assembly to their new factory in Tuas. The factory has a higher capacity and includes a 204-bed worker dormitory and solar panels to drive efficiency.Continued demand in Singapore construction & data centers

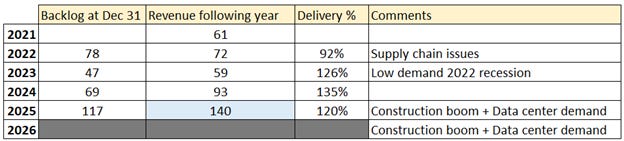

Singapore’s building authority projects SGD ~50bn new construction demand in 2026, like 2025 and up from ~44 bn in 2022-2024. Construction is expected to normalize in 2027 while data center demand is expected to continue growing until at least 2030.Record Order Book (Doubled in 12 months, driven by 140 mSGD new orders)

Let’s look at what their current backlog suggests in terms of forward revenue growth:

The company typically delivers more than their backlog in a year. Average project lead time is 9-10 months. Previous award announcements confirm this. The only exception we can find is 2022, a year of supply chain delays.

Applying a ~120% delivery factor to their current order book, leads to an estimated 140 mSGD revenue in the 2026 calendar year, much higher than the current 107m run rate used in the valuation above. If the current 15% gross margin persists, this will bring additional operating leverage and ~10-14m 2026 net income…

This puts into perspective the 7.7m net income we are using by annualizing the past 6 months. Looks aggressive now, might look conservative in the future.

Valuation

We like to use a 10-12x ex cash fair value P/E multiple for double digit growth companies.

This puts Lincotrade at 0.49 – 0.57 SGD per share, for ~ 100% upside vs today.

(7.5m x [10 to 12] + 14m, or ~ 89 – 104m market cap)

The 12x P/E is not necessarily a sell target. More like a “should trade there quickly unless there’s a dead mouse under the carpet” type target. Then when it gets there and the mouse hasn’t appeared (or is alive and well), we consider if we have a new better idea or not.

Risks

Lumpy project demand. Projects are lumpy and customer concentration is not disclosed but seems limited to ~15-20% for 1-2 major projects. Overall demand may cool down 2027-2030.

Execution. As projects are getting larger, they could become harder to execute and take longer. Doesn’t seem to be happening, as the recent 29 mSGD data center ordered in November will be completed in <12 mo.

Margins. The next 6 months will prove if the company can expand from their modest 8% net income margins, or if they re-rate to prior years’ lower 2-3% net income margins. In the prior years, a big part of the business was residential and show-flats though.

Management. Jimmy and Jackie are changing roles a bit with Jackie taking over the CEO role and Jimmy staying around in an executive management role. This can sometimes flag collaboration issues, but we think here the opposite is the case as the 2 have worked well together for ~40 years now.

Summary

This company is very likely growing double digits in the coming 24 months, justifying a double-digit P/E multiple which would make this a double. Do some work on this company before investing rather than just diving in based on what a stranger on the internet thinks though.

Thank you for reading!!

Disclosure: Long. Please check out the company before investing.

Disclaimer: This publication’s authors are not licensed investment professionals. Nothing produced here should be construed as investment advice. Do your own research before investing.

Great write up, Floe!

Stock went up 16% on Friday...from you buying? :) I think P/E is close to 7 now.

I have a learning question since I'm new to microcaps-- who are the marginal buyers?

For large caps, the price discovery machine is well-oiled. Analysts publish targets, index funds rebalance, quant funds screen for factor exposure, activist investors push for changes. So the market is usually good at finding and correcting mispricings. But for the S$50m Catalist-listed Singapore construction subcontractors, who are "discovering" the correct price and chipping in? Us? :)

Just wondering what are the mechanisms for price to go up for this type of stocks.

Hey, You say Lincotrade has been growing very well since IPO. The stock chart at first glance doesn't really seem to relfect that imo ;).

Let's say the whole AI bubble burst somehow, how bad would that affect Lincotrade's data center revenue?

I also have a hard time putting the rightfull P/E on this company because there's the aspect of cyclicality in construction.