Alquiber Quality

Compounder trading at 5x true earnings, hidden by over-depreciation

Today we will discuss a company that always looked extremely boring to me. It always delivered 10-20% growth while trading at 8-9x earnings. Very boring, until I realized… Wait a second…

You guys are hiding half of your earnings power… True P/E is more like 5x, and the true earnings are likely going to show up in the 2026 reports.

Let’s take this company for a ride…

Overview

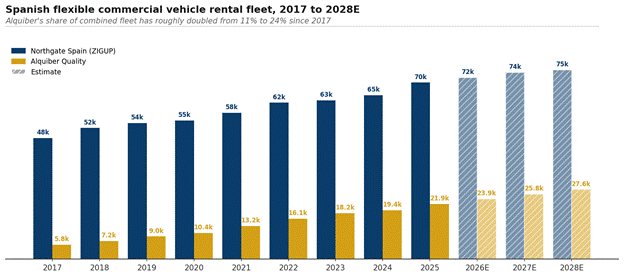

Alquiber rents out 22.000 vans and other commercial vehicles to SME’s in Spain.

The company is interesting because:

They grow double digit revenues, take market share, deliver consistent profits…

They look cheap at 9x P/E on 2025 reported net income of 8 mEUR (74m mkt cap)

They are cheaper at 5.5x P/E, after removing consistent fleet over-depreciation

Their reported net income likely jumps from 8, to 14 - 16 mEUR in 2026, driven by higher revenue from rental and fleet disposals

Briefly: The company is interesting because it owns 22,000 cars, and depreciates them too fast, down to 21% of purchase value in just 5 years. This results in large gain on sales when they retire and sell the cars.

In reality, they should depreciate at least 26% slower, resulting in 50-100% higher reported earnings, and a P/E of 5.5x conservatively. The company is hiding its real earnings inside the depreciation of its cars… That’s great for taxes, but investors better pay attention…

1. Long-term growth, founder-led

Miguel Angel Acebes is a veteran of vehicle rental. In 1980, he founded Fualsa, Spain’s first flexible commercial rental company. He sold Fualsa to competitor Northgate in 2002, staying on as CEO for 3 years.

After his non-compete expired in 2009, he bought Alquiber together with his daughter. They spent the last 15 years growing the same business while competing with Northgate again in the Spanish market.

Alquiber is focused on medium-term, flexible vehicle rental, mainly of vans like Fiat Ducato. The type of van a florist or a restaurant owner would use. Flexible vehicle rental is growing quickly in Spain, as small business owners switch from owning to renting their vans, enabled by a competitive and flexible vehicle renting eco-system.

Alquiber has achieved double-digit growth in revenue and profit in recent years, driven by expanding market and increased market share.

The company’s fleet and go-to-market strategy is comparable to that of Northgate, although Alquiber tends to focus on slightly larger and more differentiated vans, including earthworks cranes and other equipment.

Alquiber is founder-led and owned, vs Northgate being owned by its corporate acquirer. It looks likely that Alquiber will continue taking market share in Spain. I don’t know exactly how they do it, but they always seem to outperform Northgate…

2. Looks cheap at 9x P/E

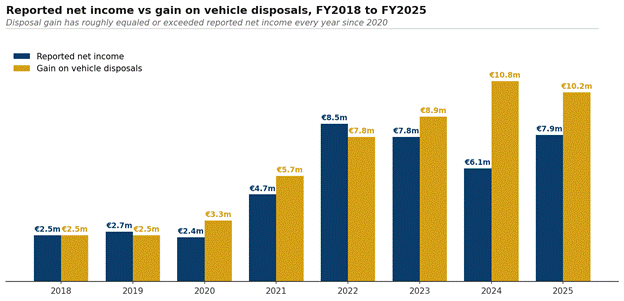

Alquiber recently reported record 8 mEUR in net income for 2025, and trades at an undemanding 74 mEUR market cap, or 9x 2025 net income.

Looking at the source of the profits though, we see that they can be attributed to “Gain on sale” of obsolete vehicles. Alquiber retires each vehicle at about 5-6 years old.

We could look at this chart and say: “That’s terrible earnings quality”. The business is not profitable and only makes money selling the vans at the end of their useful life…

This is a fast-growing company though, so the cars they are disposing of now, only represent a small fraction of their fleet. If the fleet was more mature, disposals would be much larger.

The gain on sale on the small group of cars disposed of, is the tip of a larger iceberg of cars in operations, which are being depreciated too quickly. Alquiber’s accounting is taking value out of each of its 22.000 cars, making earnings and book value look lower than they really are.

3. Understating earnings, depreciating too quickly

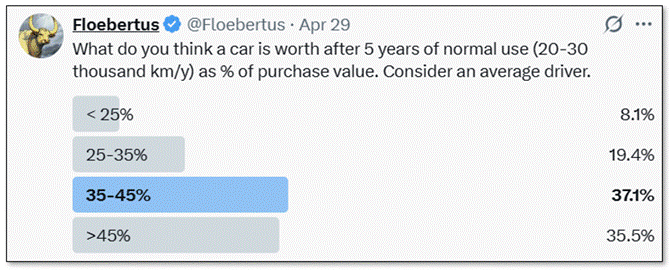

Alquiber depreciates their fleet at 18% in the first 3.75 years and 9% in the years after. According to this depreciation schedule, an Alquiber van is worth only 21% of its value after 5 years. This feels extremely low, at least according to Fintwit:

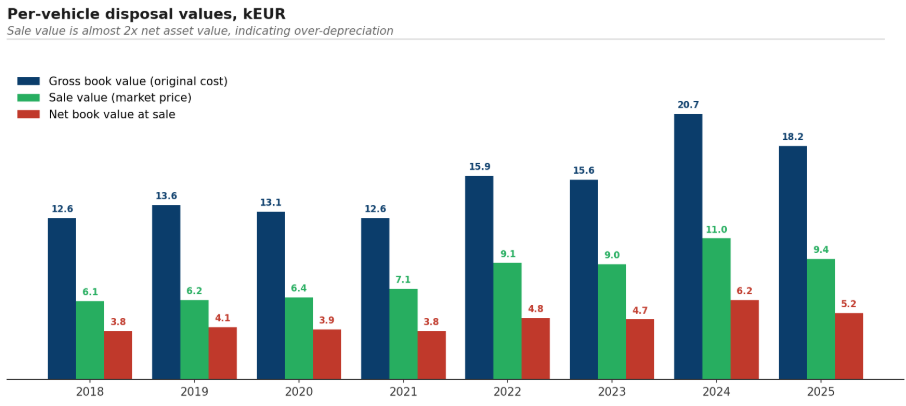

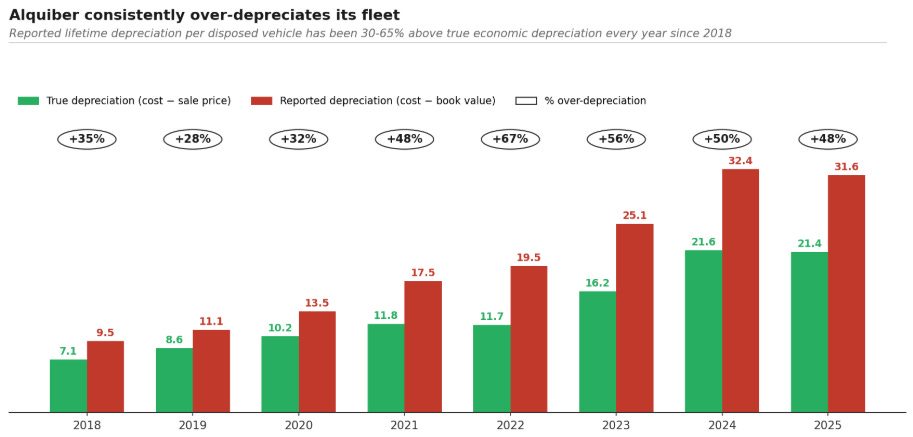

Comparing the realized market value to the gross and net book value of the cars sold, we can understand how much depreciation should have been, versus how much it was.

Twitter was right. The average car sold in 2025 (4.2 years old), was sold at 52% of its original value, indicating a 5 year old car would realize about 35-45% of its value.

Flipping this data the other way around, this means actual depreciation over the lifetime of cars sold in year x, was higher than true depreciation:

On average, Alquiber depreciates its fleet about 40-50% too quickly. One could say here, wait a second. Didn’t used car prices go up a lot during Covid? Yes, they did, but have come down since. They are up ~3% per year since 2019, nothing unusual:

A comparison vs Northgate parent ZIGUP, also shows Alquiber’s over-depreciation

Alquiber in 2025 depreciated gross fleet value at a rate of 18%

ZIGUP depreciated gross fleet at 13% in 2025

Again Alquiber records over 35% higher depreciation than its competitor.

I will use 35% as conservative over-depreciation number for Alquiber today

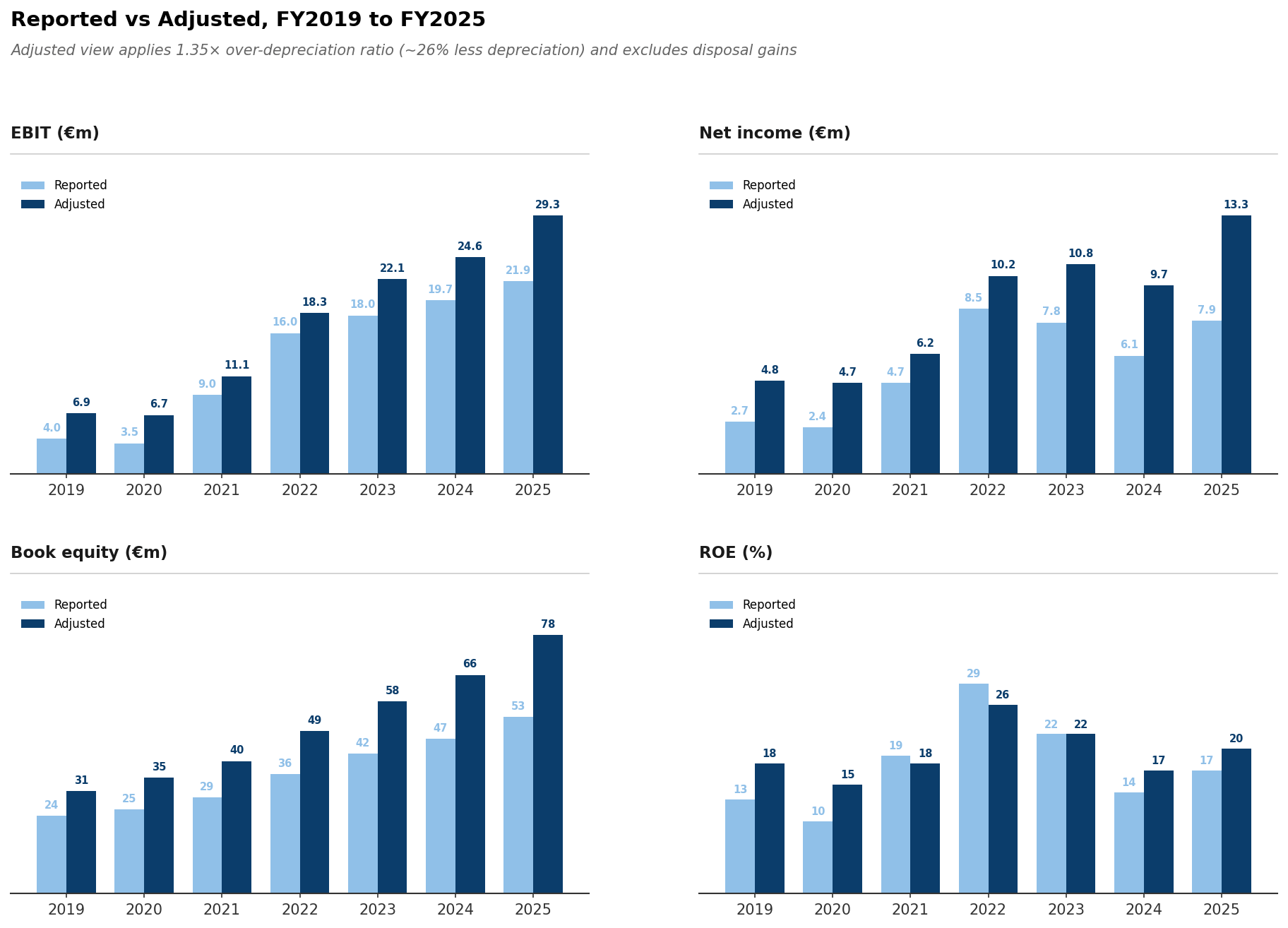

True earnings power

Three different approaches (Twitter estimate, gain on sale analysis, peer comparison) indicated that Alquiber’s depreciation is at least 35% too high.

The chart below adjusts this by calculating a 26% (x 100/135) lower depreciation value, getting the resulting book value, net income, and ROE for the company. (setting disposal gains to 0)

Alquiber had a true earnings power of 13 mEUR in 2025 (vs €8m reported), and therefore trades at about 5.5x adjusted P/E (vs 9x reported).

4. Reported net income likely to jump in 2026

Modelling Alquiber’s net income suggests reported net income might almost double in 2026, from €8m to €12-16m. This is driven by 2 factors:

The fleet is aging leading to slightly lower depreciation per car

More cars getting disposed of, leading to higher disposal gains

This is true at least in theory. In practice, management might delay disposals, depending on how demand in the rental market behaves vs. demand in the used car market.

The good thing is, if they delay disposals, this will push more cars into the 9% and eventually 0% depreciation rate, and if they don’t delay disposals, this will push higher disposal gains…

The company can only keep “hiding” its true earnings power by continuing to grow high teens %. Otherwise the fraction of more mature and disposed cars will grow compared to the newer cars.

Cohort survival math

Looking at Alquiber’s historical fleet purchases, and annual fleet sizes, I can model the survival rate of the cars in Alquiber’s fleet, as a function of the cars years in service.

I’m assuming here, that cars less that 3 years old don’t get sold off. They can only leave the fleet through accidents, at a rate of 1-3% per year:

For example, for 2025, they have 21913 cars, which is the 4615 they purchased in-year multiplied by 99% survival, plus the 3873 purchased in 2024 multiplied by ~97% survival, multiplied … etc., all the way back until 2018, assuming all the cars bought in 2017 and older are all retired…

Solving these equations for x_1 to x_4, gave a survival vector, that helps model the number of cars, and the amount in each age group, for any given year.

RMS solving gave x_1= 10%, x_2=14%, x_3=20%, x_4=83%, which just means that after 4 years, 83% of cars are still in fleet, but after 5 years, this drops to only 20%. It looks like they suggest replacement at about 4.5 years, which the customer either accepts immediately retiring the car, or doesn’t accept keeping the car active until the end of the lease term. So this leads to many cars getting taken out at 4-5 years old.

Survival and depreciation model

Using the solution for X above, I now know how long I should expect cars to remain in Alquiber’s fleet and what the variability around that is.

Based on this, I can calculate depreciation for each year, using the fleet size in each age group for each year.

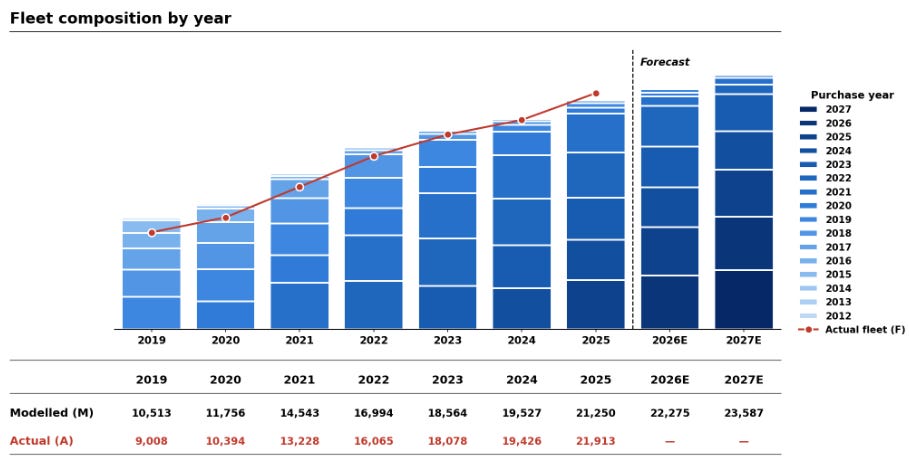

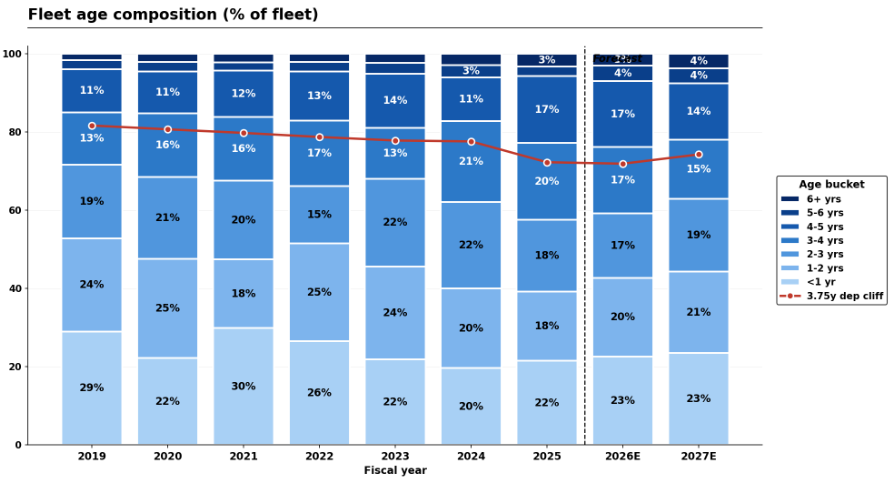

Rather than working through the matrix formula’s, let me show what this looks like visually. Applying the survival rate found above to the historical purchases, I can calculate the fleet size by year, including age groups:

Red is the actual size of the fleet, and the blue blocks are the modelled fleet size, split into different age cohorts grouping cars of the same purchase year.

This model’s prediction for how many cars Alquiber has at year end (sum of the blocks), works well for most years. 2025 has a larger model error though. The rental market was doing great in 2025, driving Alquiber to retain significantly more cars, and to dispose of less cars than in 2024. This is quite unusual and leads to actual fleet size being higher than what would be expected by the model.

More important to the thesis, I can show the % cars in each age group for each year at year-end. The red line here indicates what % of cars is younger than 3.75 years, which is a threshold for reducing depreciation. As the line goes down in 2025, I could expect slightly lower depreciation in 2026.

Observations on the modelled %s shown above

The fleet is getting slightly older. The top cohorts, especially with cars 4-5 years old is growing in importance

Disposal rates are expected to increase in 2026, as 17% of cars are in the 4-5 years old bucket. These are modelled numbers by the way. In reality this fraction is even bigger, driven by low disposal rates in 2025.

A key reason the fleet is aging, is 2021 purchases. The bottom block in 2021 shows they purchased a lot of vehicles through 2021 coming out of Covid, and those are now nearing their typical disposal age for Alquiber.

So What?

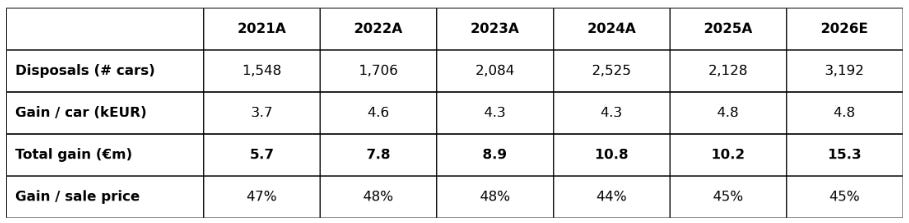

2026 will have ~50% higher disposals and disposal gains, because according to the model, at end of 2025 they have over 50% more cars in the 4-5 year age group.

In reality, Alquiber retired less cars in 2025, so the 2026 effect could be even larger.

Estimating 50% higher disposals than 2025, and a similar gain per car, gets:

This will likely cause 2026 net income to be 5-6 mEUR higher than 2025 net income, mainly driven by higher disposal gains, complemented by higher rental revenues and EBIT, as the business continues growing.

P/E on estimated 13-14 mEUR net income in 2026 is then 5x - 5.5x on reported earnings.

Risks

Used vehicle prices. Gains depend on used cars holding ~50% of cost after 5 years. LEZ tightening and EU 2035 phase-out could drag prices 10-15% lower. I have already incorporated 10% lower prices into the thesis by using 35% over depreciation instead of 40-50%. Still, the company is highly levered to used vehicle prices.

Spanish construction softening. ~30% of customers construction-exposed. Recession hits utilization and used prices simultaneously.

EV transition. Almost all of Alquiber’s fleet are currently ICE. It’s likely that in 5-10 years they will transition to EV. This may create different competitive dynamics or different customer preferences.

Higher interest rates, can form a headwind on earnings as the company is highly levered. The leverage is less problematic than it may seem though, as the company has highly liquid collateral in the form of over-depreciated vehicles.

Summary

Alquiber is a stable grower in the Spanish commercial vehicle market. While already cheap at 9x P/E, we argue that true earnings are understated because of excessive fleet depreciation.

We think this disconnect will temporarily reverse in 2026 mainly driven by the retirement of larger 2021 (post-covid) vehicle cohorts, driving reported earnings up to 13-14 mEUR.

At an undemanding 2026 P/E of 10-11x, Alquiber provides a potential 100% upside from todays 13.8 EUR share price.

Disclosure: Long. Please check out the company before investing.

Disclaimer: This publication’s authors are not licensed investment professionals. Nothing produced here should be construed as investment advice. Do your own research before investing.

Hi Floe, smart post. One question; on the sbc article Burry showed how Tech companies pump ammortization years to pump profits, here is a kind of opposite, why this situation?

Another great write up, Thanks

Who do they sell their used vehicles to ? In a way, you could think of that as a 'customer.' Any chance they won't continue to get above book value on future sales ?