Appetizers

Two tiny SGX listed companies, growing, profitable, trading below cash, buying back stock

In theory, my job in finding great investments, is to constantly flip rocks, go through filings and reports, and see as many companies as possible in a short amount of time to find some that are obviously mispriced…

In practice though, I often find myself distracted… My favorite part of investing, is the story each company has. Going through these stories sometimes helps us understand something more about the reality every companies faces and handles in their own way.

It’s in that mode of distraction, that I have looked deeper into 2 companies, that I should usually discard at hand, due to low liquidity (~10k$/day)… I have loved discovering their story and have invested a small sum in both.

They are too small though, to put a lot of money into due to low liquidity.

We’ll call them appetizers… Small bites before something bigger arrives…

Today’s 2 companies both:

Are Singapore listed

Are founder-led, over 25-year old businesses

Have more net cash than their market cap (& Negative EV)

Are growing and profitable

Are actively buying back stock

Trade near 52 week highs

Have liquidity of only ~$10k/day (buyer beware)

Let’s have a look - I will try to keep it concise…. As we have work to do finding the real big fish after this little detour…

1. Anchun International Holdings ($BTX.SI)

Anchun is a technology company that provides reactor equipment, services and chemical catalyst products, to global chemical players, mainly to convert coal into hydrogen and other gasses, play around with those gasses and turn them into methanol and ammonia.

Founder Xie Zhong started the company in 1993 as “Anchun Energy Savings”, using 15 years of experience teaching chemistry at Hunan University in China. He has meanwhile handed over the CEO role, but his passion for technology remains in the company, shown by their large R&D focus resulting in the over 100 technical papers and patents the company has published and obtained.

Anchun’s proprietary reactors are optimized for creating iso-thermic reactions that generate H2 from CO & H2O. Most chemical reactions in the process of generating H2 (and ammonia), release substantial heat. Until ~10 years ago, most equipment design would accept this, leading to incomplete chemical reactions, because closer to the exit of the reactor, the temperature would be so high that the reactions catalysts would decay and production of byproducts like hydrogen sulfide would increase… Anchuns isothermal reactors maintain a constant temperature throughout the reactor, enabling a better result (more pure reaction and more energy-efficient).

Anchun is mainly present in China, where coal gasification provides way to produce artificial fertilizer in the absence of natural gas. China converts coal into syngas, then H2, ammonia and finally nitrates (aka Urea) used in fertilizers

As most of Anchun’s tech is used in the artificial fertilizer industry, they are heavily exposed to Urea prices and investments. This caused the stock to get killed from 2013 to 2017 as Urea prices dropped about 50%.

The company has since focused on reducing fertilizer exposure, which finally seems to be working, as 49% of 2024 revenue was non-fertilizer, and 74% of current orderbook is non-fertilizer. This non-fertilizer revenue seems to mainly represent “green” energy projects in China but also in the Netherlands, Turkey, Thailand, and Africa.

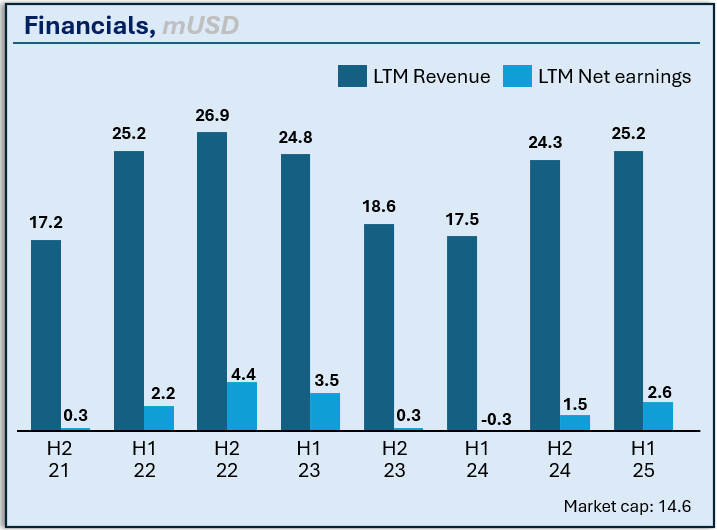

Looking at the financials, below are the companies LTM Revenue and Net Income for the past 8 reported periods. We see financials coming down a bit after Urea spiked in 2021-2022 at the start of the Ukraine war, and then picking up again in the 2 most recent half years.

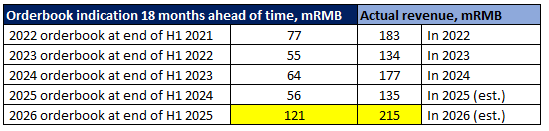

It’s easy to estimate H2 2025 revenue, because Anchun basically tells us their current orderbook and planning and resulting future revenue recognition. For H2 25, the company plans to deliver 58.5 RMD (8.4 mUSD) in revenue from orders confirmed before H1 2025. In practice, some additional design orders and catalyst orders likely come through leading to ~60-65m RMB for H2 2025 making full-year 2025 revenue ~135 mRMB (19.3 mUSD).

Looking at 2026 though, the company had already planned deliveries of 121m RMB as of end H1 2025, which is much larger than usual at the mid point of the prior year, as you can see below. This suggests above 210 mRMB (30 mUSD) in revenue for 2026:

Given they already have these orders, much of it will likely be recognized in H1 2026 already, at which point, we are looking at a company that will have just posted 30-40% organic growth, driven by green energy projects, and has a strong orderbook for the rest of 2026...

Looking at the valuation, Anchun trades at a P/E of 5.5x on TTM earnings. As suggested above, H2 2025 might be down year over year, but 2026 will likely be a record year.

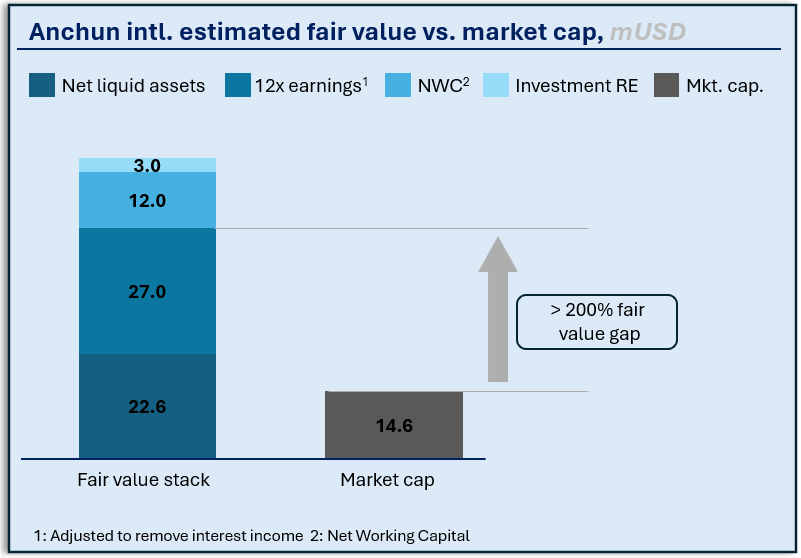

From a balance sheet point of view, things get a bit crazy:

Market cap is ~15mUSD (19 mSGD with 0 options/warrants/pref./perf. shares)

Cash & cash equivalents is ~23 mUSD (no debt)

Net working capital is ~12 mUSD

(Almost exclusively contract assets aka work partially done but not billed yet)

Fair value imho is ~12x net operating earnings + net cash equivalents. This would give

= 12x ( 2.65 net earnings - 0.4m interest income) + 23m cash & cash eq

= 49.6 mUSD

which implies >200% upside versus the current market cap of 14.6 mUSD. Per share fair value in SGD is estimated at ~1.4 SGD.

Finally, Anchun has a 10% buyback authorization outstanding, and bought back just over 1% of their shares in November-December 2025. I think the buybacks likely were the result of a shareholder contacting the company and them being happy to take over the shares through on-market share repurchases. This suggests further buybacks may be spotty rather than consistently recurring.

Disclosure: I am an investor in Anchun but sized it small to leave space for the main course.

Disclaimer: This is not investment advice, please speak to your adviser before investing, and please do your own work analyzing the company.

2. A-Sonic Aerospace ($BTJ.SI)

I need to hurry up a bit here, as the next company is close to getting to zero EV. That sounds like they are going bankrupt or something, but of course, zero EV just means that the company has its full market cap and debt in cash, meaning no value is given for the enterprise, and we just get it for free.

Also, appetizers shouldn’t take you more than 10 mins to read, so let’s make it relatively quick to the finish here. A-sonic was started in the 90s by Jenny and Janet Tan, initially as “Janco Aviation”, a distributor of airline control systems for Boeing airplanes.

While the sisters initially branched out from airplane control systems to engines and other airline parts, it became clear to them over the years, that their true skill was not sales of Boeing spare parts, or even expertise in airline parts, but rather in global distribution and logistics.

They re-named the company from Janco to “A-Sonic”, for “A-rated Solutions On-time, leveraging on our Network, working with Integrity and Commitment to provide customer satisfaction” and started a Logistics branch which now represents 99% of the business.

A-Sonic now helps individual and corporate customers ship goods from point to point globally, setting up the optimal combination of transport methods, and driving efficient custom clearance for simple products as well as complex products (e.g. food, batteries, radio-active parts, etc…).

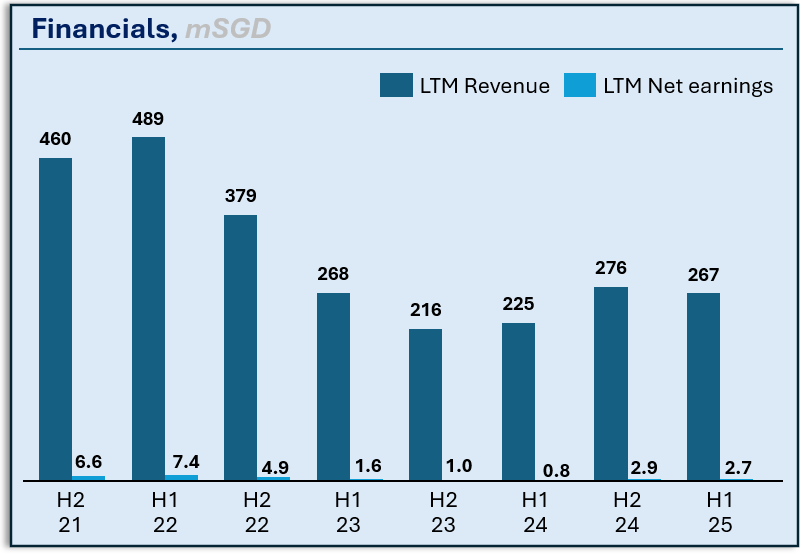

A-Sonic’s revenue and profits have been weak in recent years. There was always a problem on the global stage, from 2022 post-covid weakness in demand, to the Chinese economy falling into a recession, to the recent tariff troubles. Over the past 12 months though, revenues were ~20% higher than the year prior, driven by a slightly stronger global consumer, driven by subdued inflation fears, leading to ~11% higher global airfreight volumes.

The company books most revenue around Thanksgiving and Christmas, and is highly dependent on global trade as well as economic growth driving higher and more creative consumer expenditures… For example, more people will ship a new BMW into the USA in a good economic year vs. during a crisis, and this is the kind of unusual activity A-Sonic helps manufacturers or other logistics and fulfillment companies with.

H2 2025 is very interesting for A-Sonic, because on August 29th, 2025, the USA ended the “de minimis” exemption for shipment of small packages into the country. This regulation used to be in place and exempted all packages with <$800 value (like your $16 Temu “Soft cabbage novelty blanket”) from full customs documentation and full customs clearance. Customs documentation and clearance is now needed for all packages without exemption.

This seems horrible for global airfreight volumes, and global logistics players. In fact several companies halted shipments of parcels into the US for multiple days and weeks when the regulation was introduced, given the unpredictability of the resulting situation (stringency, waiting times, disorder… at US customs).

It’s potentially great for A-Sonic though, as a large part of their business is to enable fast-tracked and seamless customs clearance, enabled by ~600 employees with offices across 13 countries, bringing expertise, experience and a network to drive frictionless logistics. More friction likely means more business for A-Sonic, at least short term. And more is coming, because Europe has already introduced similar regulations ending their “de minimis” exemptions as well.

It’s hard to predict the exact positive/negative impact on A-Sonic. We do know though, that similar to last year, A-Sonic’s CEO has turned on the Buy-Back machine, buying back 1.5% of shares outstanding in Q4 2025, most of which happened in December (~1%).

CEO Janet Tan already owns over 60% of the business, but is adding to that stake through those buy-backs. Note that H2 2025 is behind us, so good/bad results have been achieved, but have not been published yet. Mrs. Tan clearly thinks the shares are undervalued, making a great H2 very likely.

Mrs. Tan thinking A-Sonic is undervalued also became very clear already in 2021. At the time, she bought over 1 million shares from her sister, in a private transaction at 0.80 SGD per share, while the shares were trading at 0.57 SGD on the SGX exchange.

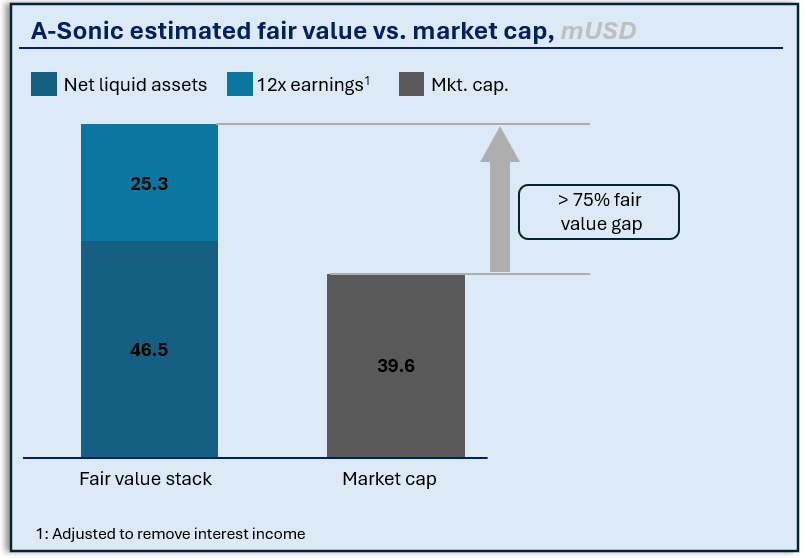

Looking at the balance sheet, A-Sonic is another company with a market cap below net cash and cash equivalents. The current earnings power provides potential upside, especially given the current aggressive buybacks, but the true upside could come from the relationships and customers the company is finding while helping companies adapt to the new US and EU regulations.

Disclosure: I am an investor in A-Sonic but sized it small to leave space for the main course.

Disclaimer: This is not investment advice, please speak to your adviser before investing, and please do your own work analyzing the company.

Note: Both companies covered today have large insider ownership (~40% and ~70%) but those positions are not at all large enough to exposed minority shareholders to delisting or squeeze-outs by majority shareholders.

Thanks all!

Fantastic ! Thank you:-) I just came across both of these while embarking on a personal A-Z of the SGX.

I'm particularly curious what you think about Anchun's LT prospects: is this likely to remain cyclical around the median, or do you see longer-term structural growth trends that could lead the MC to grow much higher over time, even as it fluctuates in the shorter term?

I'm curious about this as a way to play Charles Gave's suggested pivot to "Ricardian" growth (= an age of engineers, not disruptive inventors)

like your $16 Temu “Soft cabbage novelty blanket : true! One question: about the first business are there any risk realted to cancellation of backlog orders?There was some past events as you know refferred to cancellation?Thanks, very interesting cases.