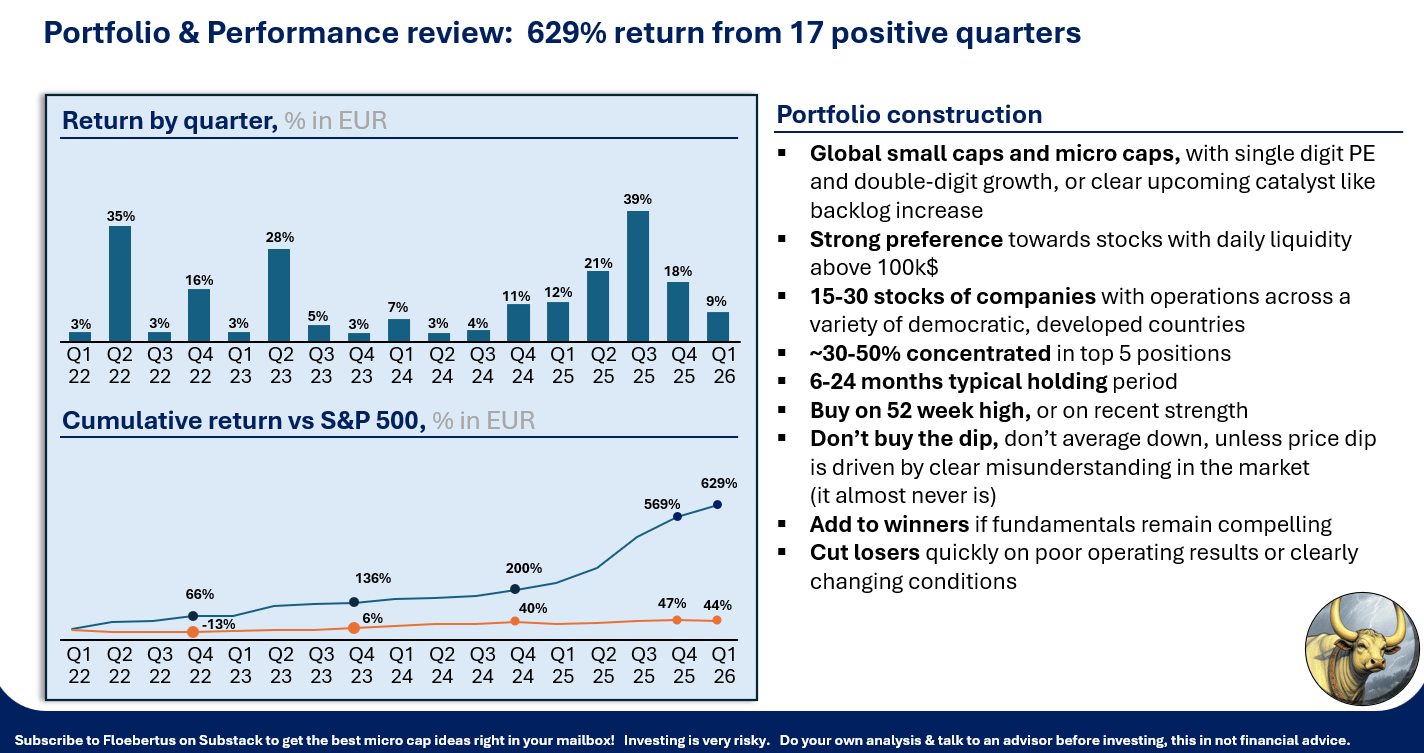

April portfolio update (+629% vs 44% S&P)

A 17th consecutive profitable quarter

It’s a pleasure to provide the April portfolio update! Let’s dive straight in.

Performance

The portfolio returned 9% year to date, compared to ~ -2% for the S&P 500 expressed in EURO. We made a 17th consecutive positive quarter.

The portfolio is currently not live available to subscribers. I’m afraid that would encourage too much copy-paste trading, exposing you too directly to my mistakes.

Subscribers have done well doing their own analysis of my write-ups though, which actually have performed better in this quarter:

Two new write-ups will be out soon, one tomorrow on a stable, consistent EPS grower hiding behind a temporary accounting overhang. A second one later this month on a larger, more liquid company which trades at a single digit multiple but has more than 10x’ed its business in the past 6 years and guides continued 30% earnings growth.

March 2026 market events

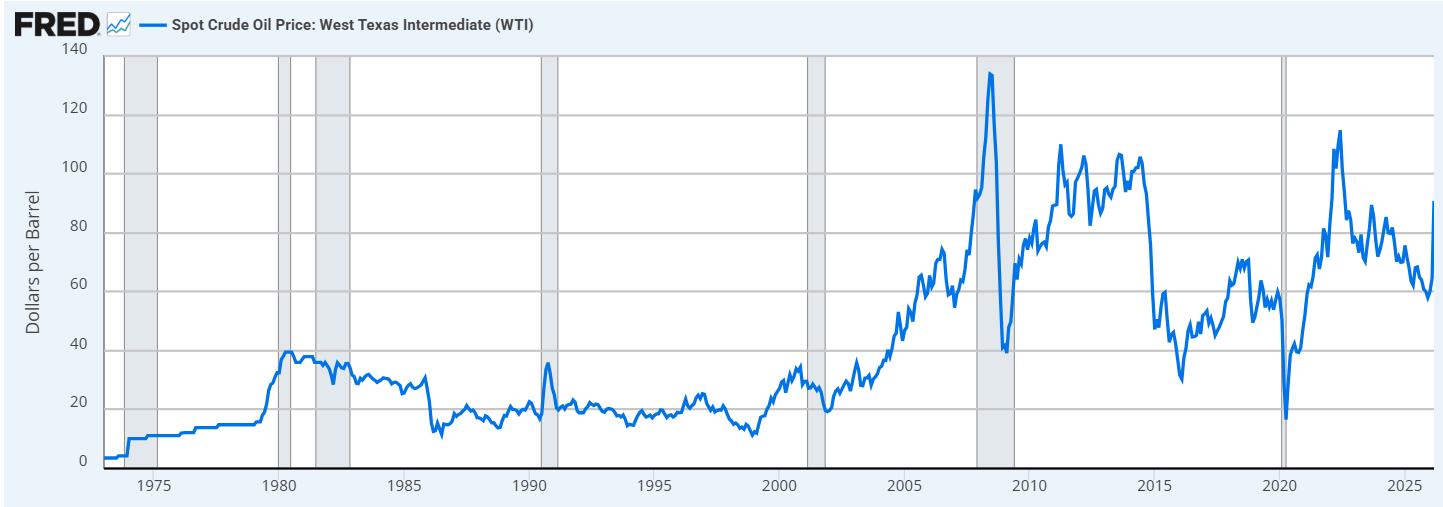

In the last month, the USA invaded Iran, the Strait of Hormuz closed, and short term oil prices rose about 50%.

Historically, when oil rises, there’s a very high probability of an immanent recession. As oil rises, the cost of living increases. This drives up inflation expectations, eroding trust in currencies.

Central banks then have to increase the cost of borrowing. Higher oil and higher rates drive down inflation-adjusted spending, which economists call a recession.

The 2022 recession is not indicated in the chart, but it did occur, in the sense that the economy did decline in real terms, and the stock market declined about 20%.

These events have hit the portfolio particularly hard, because of the large exposure to gold as well as construction. It’s good to still come out with a 9% gain for the quarter, and having adjusted the portfolio a little bit to limit the downside.

I think the war in Iran will end in April, but would also like to avoid losing a lot of money if that’s not the case. Let’s look at the current positions, latest changes, and rationale.

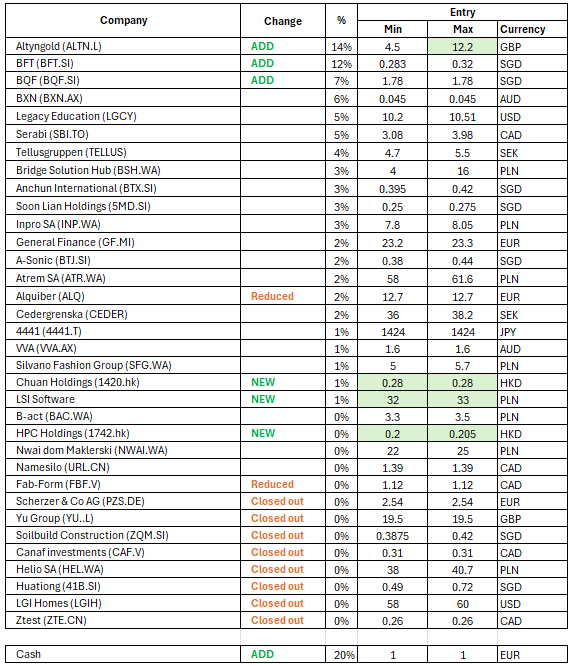

Changes and Portfolio

In this section:

All portfolio moves and their rationale

Full portfolio with % allocation and change vs last month

New positions:

LSI Software

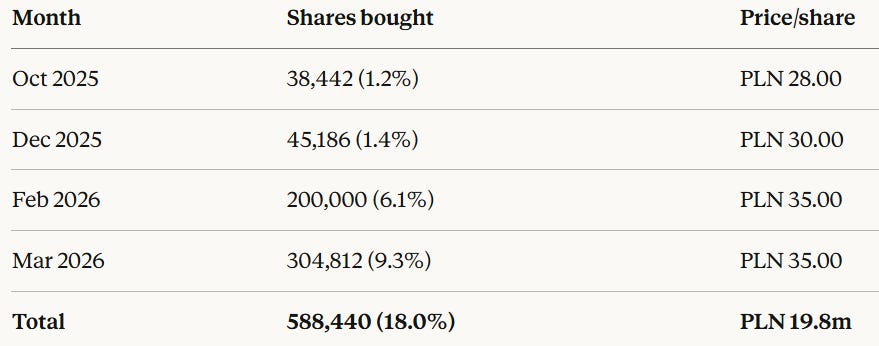

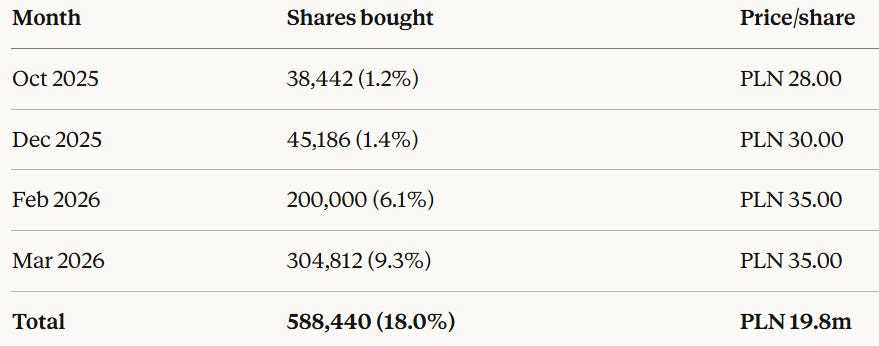

Small software and robotics company. The founders are still running the company and have grown it from ~6 mPLN revenue in 2016, to 81 mPLN right now. AI is a tailwind for LSI, as it enables customers to do more with robots. Sales is growing at ~20%, and LSI trades at ~12x earnings. Large investor “Franasik Funds” wants to delist the company, but CEO Mr. Siewiera has not been providing his votes to make that happen. As a consensus, they are buying back stock (~20% in the last 6 months)

LSI Software share buy-backs I have been buying the 32-33 PLN dips here, as I expect them to continue to raise their offer price, and ultimately buy out the company at 40-45 PLN. This is a stupidly illiquid stock though, and I have resolved to focus on > 40 kUSD stocks from now on too limit distractions.

Chuan Holdings and HPC Holdings

Both of these are highly undervalued Hong Kong listed construction companies, active in Singapore.

Chuan trades at ~3x earnings of which 2x backed by cash.

HPC trades at ~5x earnings, and below cash.

Both are not accessible to international investors, and return very limited cash to shareholders, making it likely that they will remain significantly undervalued. I use this as a tracking position, to expand on if either one of these 2 “problems” changes and turns into a catalyst.

Additions:

Altyngold

I bought a bit more Altyngold this month, as it traded at an implied 2026 P/E multiple of 2.5-3x, even after correcting for higher oil, higher Kazakhstan taxes, and lower gold. Looks like many investors who made money on Altyngold in 2025, where not prepared to risk those gains, became forced/scared sellers on the way down.

Lincotrade

I bought a bit more Lincotrade. The thesis is available below. Good to see them doing buybacks here, as well as board members buying shares.

Reductions:

Reductions to protect against the effects of higher oil:

Huationg. The companies oil expenses are the same size as their net income, putting any forward earnings estimates at risk. I initially was a buyer of Huationg this month, but when the Gulf nations started attacking each other, I realized the Iran conflict could last for a very long time.

Reductions to protect against the effects of interest rates staying higher:

LGIH. The company already did write downs against some of their assets in Q4, and likely had to do that again in Q1. Higher mortgage rates mean lower demand, lower prices, higher write-offs, higher refinancing needs to restore leverage, and higher funding costs on that refinancing… I like this company for its balance sheet, but sustained higher oil costs could have a devastating effect on that balance sheet.

As suggested last month, I have sold or reduced many smaller positions, in order to add to the larger positions I like most. (ZTE, Scherzer, Yu, Canaf, Fab-Form, … )

Changes going forward

I would like to study a bit more liquid companies going forward, let’s say above at least 50-100k USD. While these often are still undervalued and underfollowed, they would allow us to put in bigger investments and reap bigger profits when they do well.

Altyngold, OKP, Huationg, Soilbuild and Serabi have all been great examples of this, trading decent 500-1000k/day liquidity but still providing a good source of alpha.

Focusing on more liquid companies will make it much easier to share trades on a going basis, providing more value to subscribers, and getting used to making profits on deeper ideas (like OKP, Altyngold) rather than quick but small gains (like the LSI Software setup, which is interesting but way too small).

I have to force this on myself a bit, changing my ways of working leaving behind the ~10kUSD/day companies, as the portfolio has grown a lot in the last years, and I can’t “just in put more time” anymore to compensate…

I might still share some illiquid names but not invest in them myself. For example,

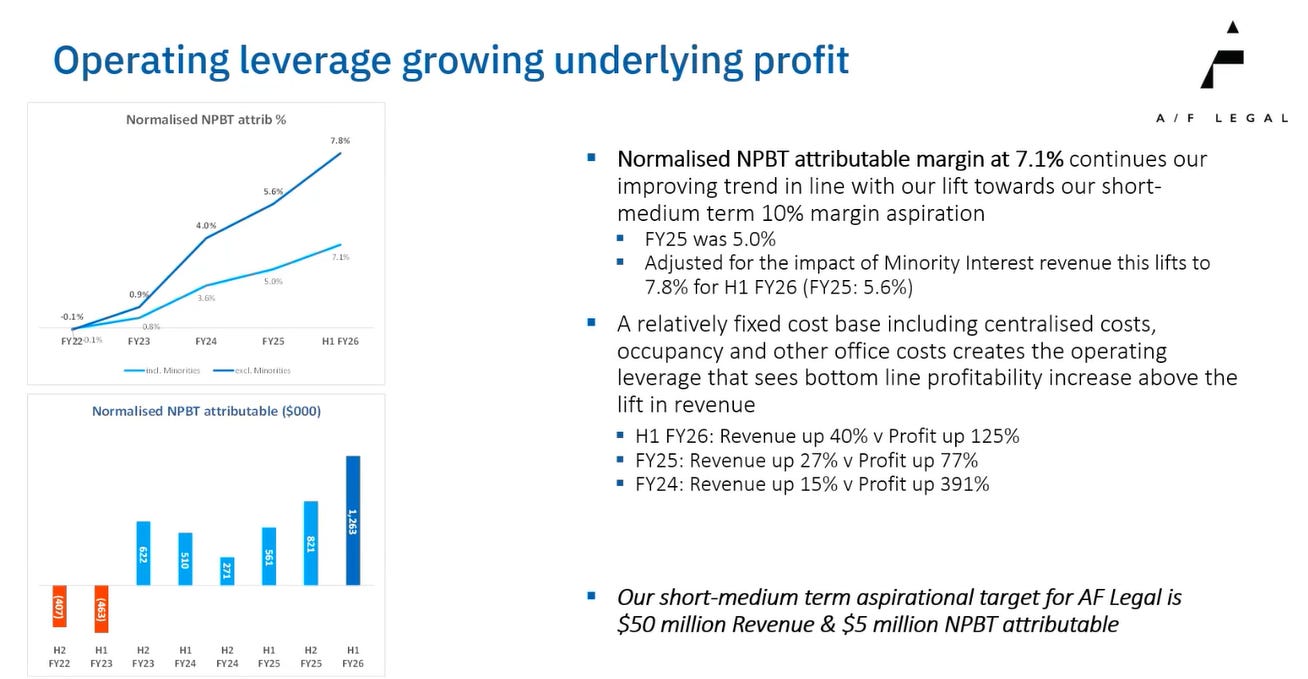

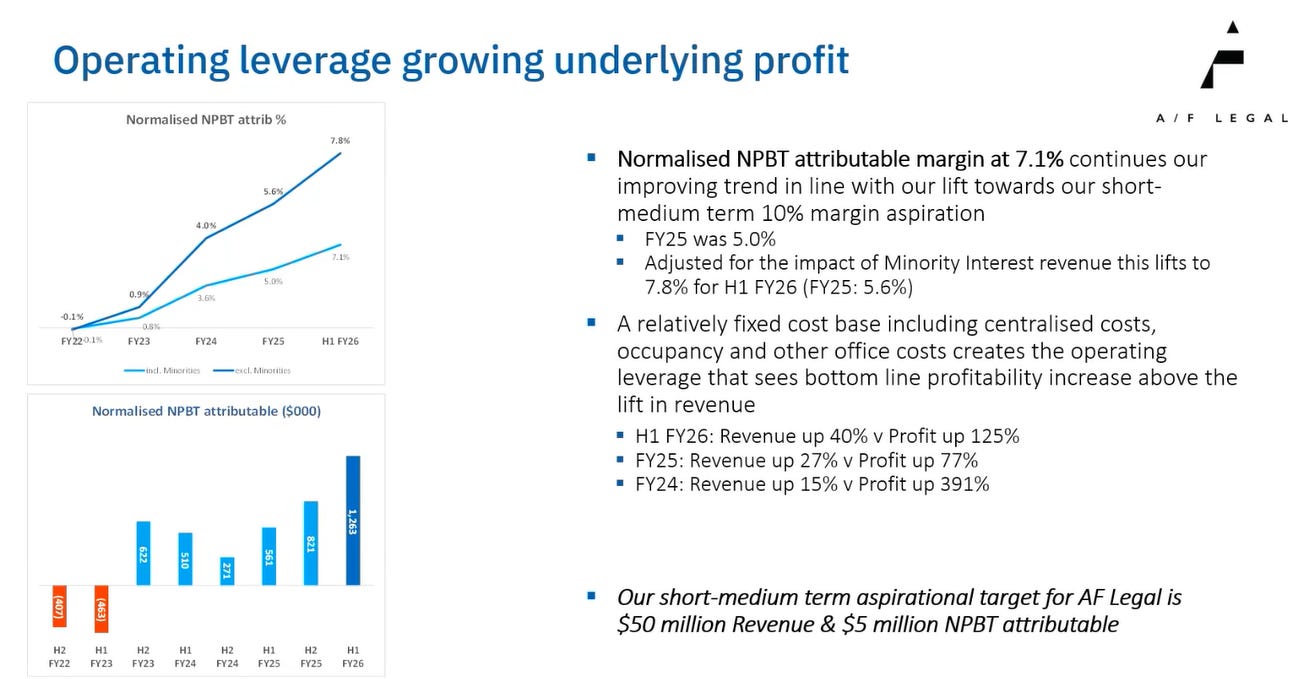

AF Legal on the ASX, trades ~5 kUSD per day, grows ~20%, has grown underlying profits since ~2018 but hidden by restructuring expenses. Guides for short-mid term profit before tax of 5 mAUD, on a 15m market cap…

AFL H1FY26 call, slide 9: vimeo.com/1169785210

That looks like an interesting setup to me, and the theory says that most interesting setups are very illiquid companies like this… So I will keep sharing them with you.

In the past years though, I have done just as well in more reasonably liquid stocks, so I will focus more on those to drive a more sustainable performance and share-able investing journey.

Discussion and Discord

Don’t copy paste and don’t always agree with me, but do check out the ideas I put out. Feel free to reach out when you notice a mistake or have a question. If you’re not on the Discord yet, just DM me on Substack for an invitation link. If someone contacts you on Discord to sell a product, that’s not me. When in doubt, ask me on Substack.

Disclaimer

This is not investment advice, please speak to your adviser before investing, and please do your own work analyzing the company.

Amazing as usual. Thank you for the update floe