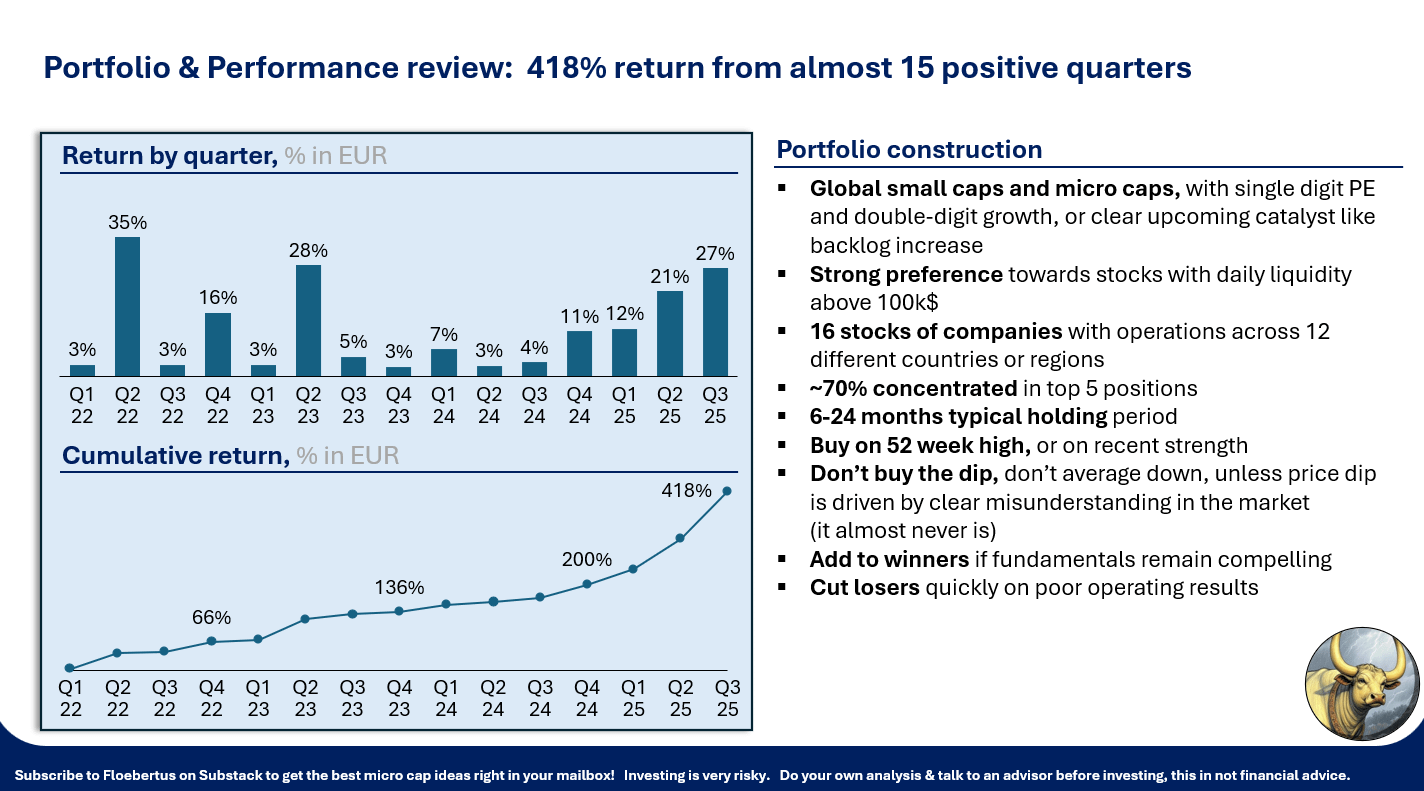

Portfolio update & Performance review

73% YTD, 5x since 2022

Hi everyone,

Welcome to our first portfolio update! We will share the current positions and a few sentences on the idea behind each position.

The ideas of the past years range from Singaporean cycling paths, to Polish make up, to Italian software companies, to gold miners, drone cameras, Baltic dairy production and everything in between. The mix is uncorrelated vs the American or international index, so we don’t compare to S&P500 or MSCI world.

We include mainly stocks with daily volume > 100 kUSD, so sufficient capital can be deployed and friction is limited.

We look for single digit PE stocks with years of growth ahead, slowly getting recognized by the market. We look at stocks globally. We analyze hiring trends, vacancies, product reviews, commodities involved, macro influence, competitors, currency effects, market perception … and pick the best stocks.

The returns so far have been excellent:

Current YTD performance is 73%.

There are 16 positions today (31/08/2025), with operations across 12 countries:

OKP Holdings ($5CF.SI)

Altyngold ($ALTN.L)

Serabi ($SBI.TO)

Bridge Solutions Hub ($BSH.WA)

Soilbuild Construction ($V5Q.SI)

Moneymax ($5WJ.SI)

DBA Group ($DBA.MI)

Canaf Investments (CAF.V)

Matsa Resources (MAT.ASX)

Asiro (7378.T)

Atlas Pearls (ATP.ASX)

Zoomd (ZOMD.V)

Hydreight Technologies (NURS.V)

Silvano Fashion Group (SFG.WA)

NTG Clarity (NCI.V)

NWAI Dom Maklerski (NWAI.WA)

Largest change since July 1st:

Selling most NTG Clarity because of foreseen lower Q2 earnings driven by weakening of USD vs Egyptian pound and higher tax expense

Selling 4Mass after weak Q1 report. The poor growth number looks exceptionally bad when noting that in Q1 2024, revenue was lower because 4Mass implemented an ERP system in the first 2 weeks of Q1 2024, shipping more in Q4 2023.

Selling Simply Solventless because of accounting issues.

Selling Vilkyskiu. The fast rise in European dairy commodity prices has ended, calming down a market where buyers panicked and paid higher margins to essentially commodity producers. We expect continued growth for Vilky but at significantly lower margins.

Buying Soilbuild after great H1 sales, backlog and profits, see our write-up called “writing’s on the wall”

Adding to the existing Altyngold, Serabi, BSH positions. (see below)

Some sentences on why we own these stocks:

OKP. Cheap niche company with a lot of growth coming in. Especially the tender pipeline with larger upcoming contracts is very underrated. The government still needs to build 2 billion in the coming years, so we would not be surprised to see them winning a 0.5-1 billion tender in the coming months. See write up and management interview for more on OKP.

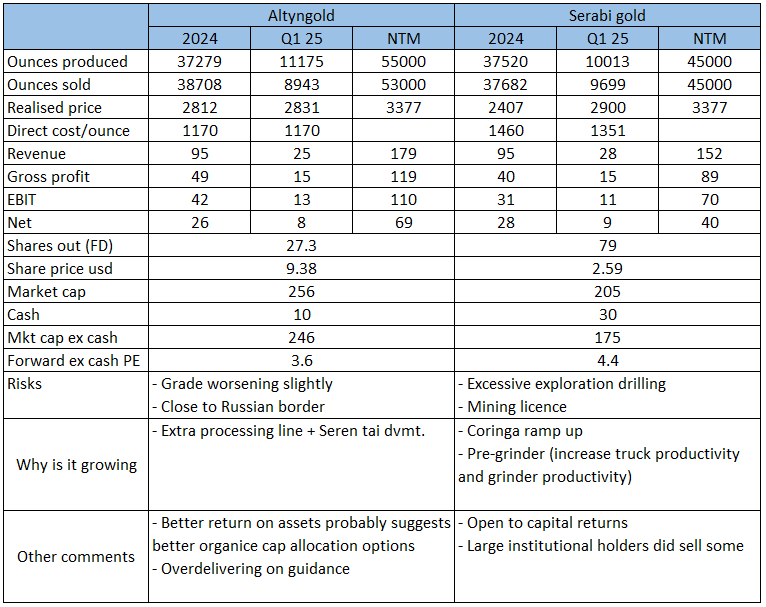

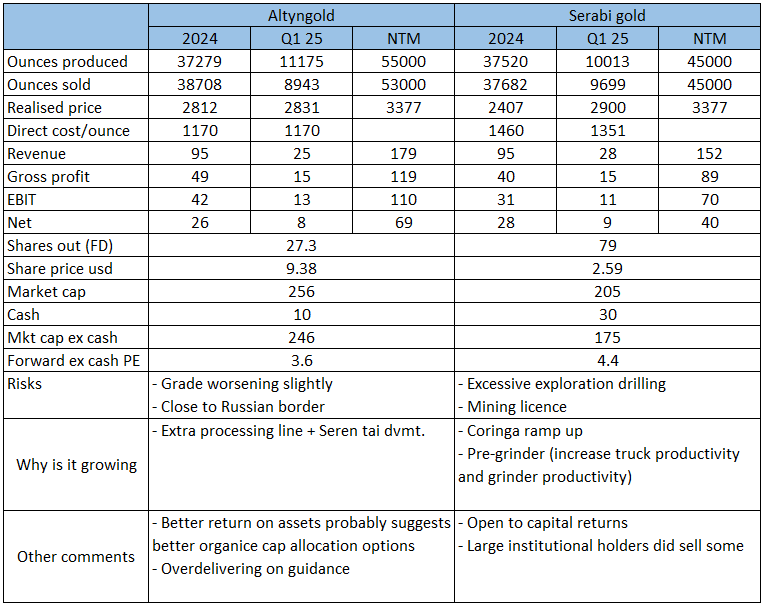

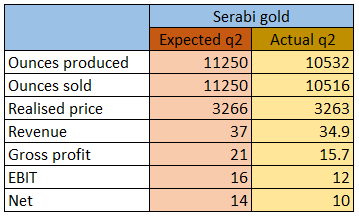

Altyngold & Serabi gold. Two gold miners which saw profitability x10 because of the rise in gold price. Simulation of their next 12 month P&L and resulting ex-cash PE:

Both trade at ~4x NTM earnings based on the current gold price of ~3444 USD. All numbers in USD. Revenue adjusted for current gold spot price, COGS adjusted for USD vs Brazil real and USD vs Kazakh Tenge moves.

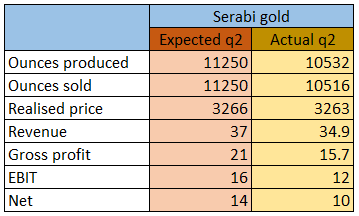

Serabi posted earnings last week which were slightly below our projections because they used some low-grade CMT stockpile material at Coringa during March and April, but the thesis is still strong.

BSH see write up & earnings update. Still very cheap. The position is limited due to limited liquidity in the stock. We own a bit over 1% of BSH.

Soilbuild see write up. They won ~718m in new contracts in the past 12 months, and achieve ~10% net margin. That’s ~72m when those contracts get delivered, putting the stock at ~6x implied earnings using this simple funny money logic.

Moneymax, very cheap pawn broker and jewelry store. Will continue to perform as long as gold does well. (higher gold = higher collateral = higher loan = higher interest income)

DBA Group, cheaper than it looks, growing Italian IT co selling the bad part of their business for a higher valuation than what the overall company trades at. We think the stock might be weak in the next month because they paused aggressive buy backs until the H1 2025 report is out (~Sep 30th)

Canaf. Cheap, hated, consistent grower in South African coal.

Matsa. Sold an option to buy Lake Carey for ~110m AUD and is starting gold pouring in September for a project with expected NPV>100m AUD materializing over the next 18 months, vs dilution corrected mkt cap ~65m AUD. Past tax losses to offset capital gains tax on the Lake Carey asset sale.

Asiro. Fast growing (50%) digital platform for lawyers in Japan trading at ~12x earnings.

Atlas Pearls. Consistent growth, good management, EPS 5ct and cash 5ct and stock price 20ct.

Zoomd. The momentum continues? Very cheap still and very fast growth consistently since the new CEO (with solid blue chip experience) came on a few years ago.

NURS. Uber for Nurses seeing high growth in leading operating metrics. The thesis was described many times by others so won’t bore you with it.

Silvano. Lingerie maker in Belarus sending bras into the Russian market. Trades at cash + 1x earnings because European brokers turned off the buy button. Still available through XTB on the Polish market, but very illiquid.

NTG Clarity. Egyptian software company with several years of high growth. We initially bought this at 0.60 CAD upon initial earnings inflection. The market will give them some hate until the recent strength of the Egyptian pound is priced through and reverses, because it makes earnings look weaker.

NWAI. Polish investment banking firm led by an ex-Citi banker. We think rates go down and they report ~10 mPLN earnings in a year at some point. Market cap 20-30 mPLN, insiders buying at all time high. Too illiquid to make a difference. We look for more illiquid ideas now.

Other thoughts

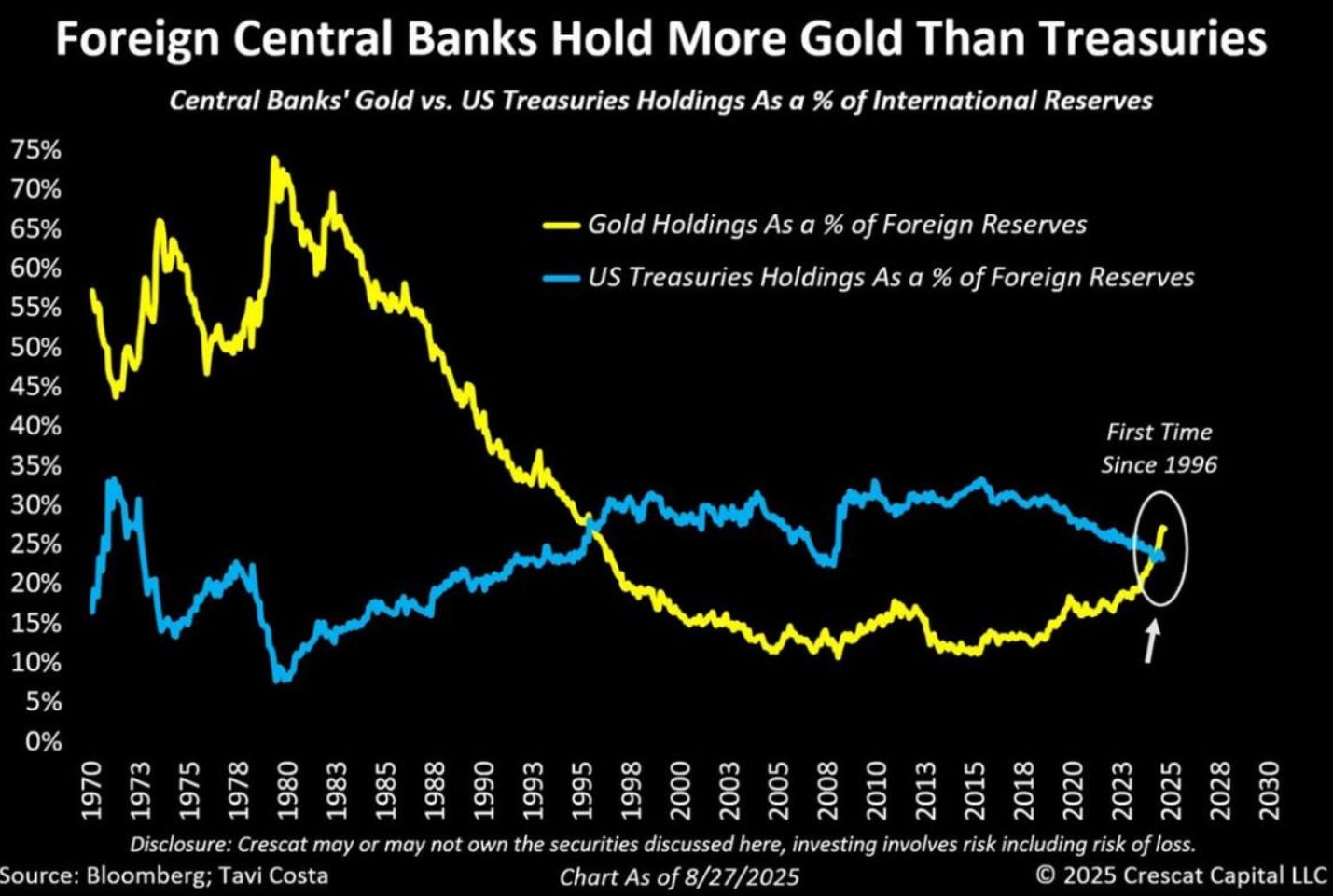

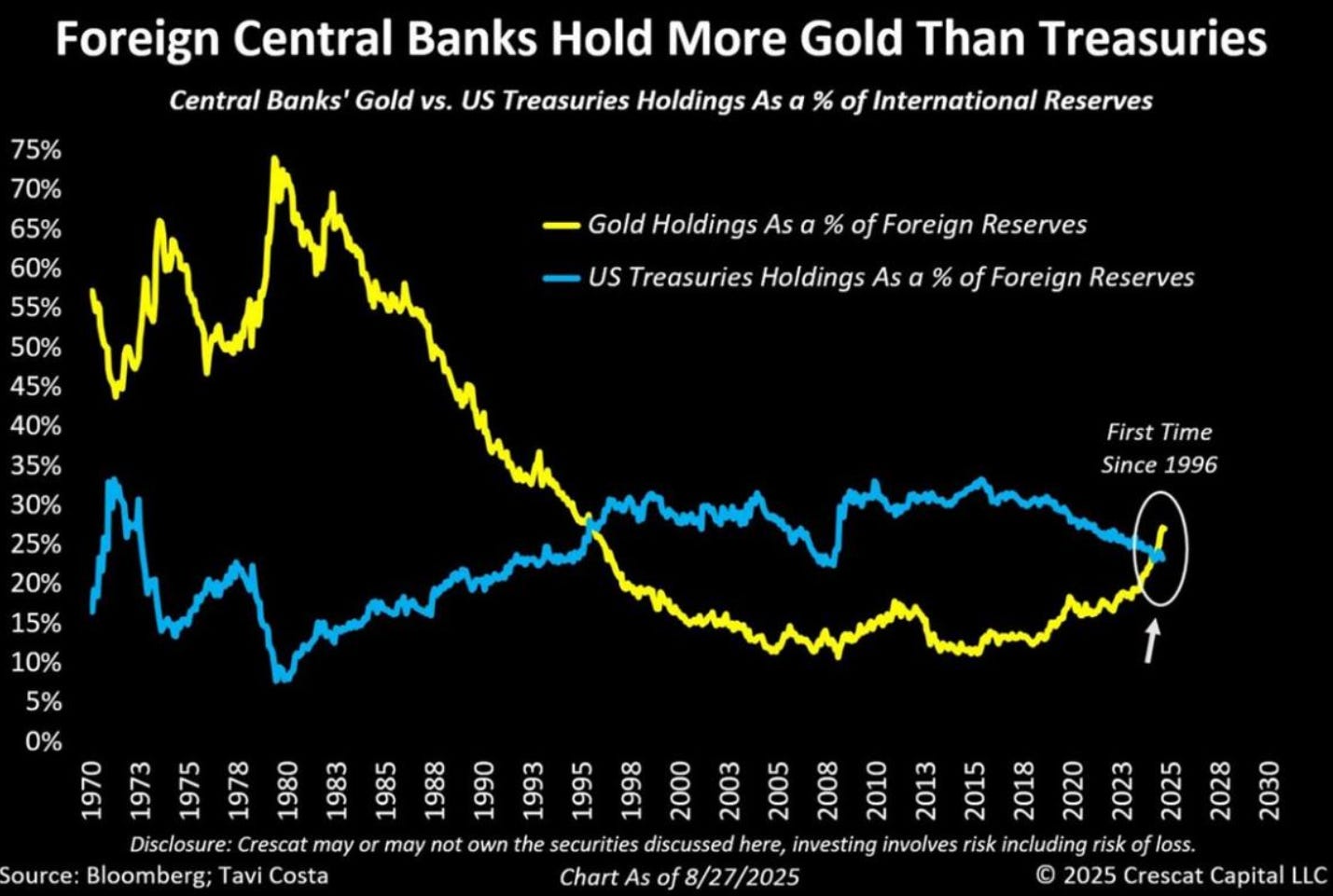

We think gold might continue to do well because since Russia was removed from SWIFT, gold is the most reliable reserve asset for developing market governments:

Couple of stocks we don’t own but will continue to watch closely:

Singapore: Huationg, XMH, Aspial Lifestyle, Nam Cheong, Thakral

Poland: B-Act, Toya, 4Mass, Passus, Yarrl

Spain: Alquiber Quality

Israel: Sofwave

Sweden: I-Tech

Canada: Spectra

Australia: SKS Technologies, Monument Mining

Japan: LTS Inc, Tear Corp., Chleru

The top positions in the portfolio have not moved much over the past 3-4 months. We expect this to continue for the next 3-4 months as we think the current ideas are strong and are playing out very well.

Returns posted above are in Euros, after transaction fees.

We will post a shorter update early October and then do this again at the end of November.

We do not give financial advice, meaning we don’t advise which stocks to buy/sell or which broker to use.

Thank you!

Disclaimer

This publication’s authors are not licensed investment professionals. Nothing produced here should be construed as investment advice.

Thanks Flo for the update!

Question on OKP - are you worried that they're over-earning on gross margins? They're basically at 20 year highs (besides 2011's 39%). The 20-year range is 7% to 39%. I get that the backlog is great and upcoming government tenders will continue to be good, but I wonder how to think about the sustainability of gross margins. Thanks.

I am subscriber for 10 minutes already;)

What do you recommend to buy today? Thank you!