December portfolio update (+102% YTD)

Positions, changes and rationale

It’s a pleasure to provide the December portfolio update. As always, we review performance, current positions, and the latest changes. This month, not much has changed, so most of the post is dedicated to broadly sharing perspective on the opportunity in the top 2 positions in the portfolio.

Performance

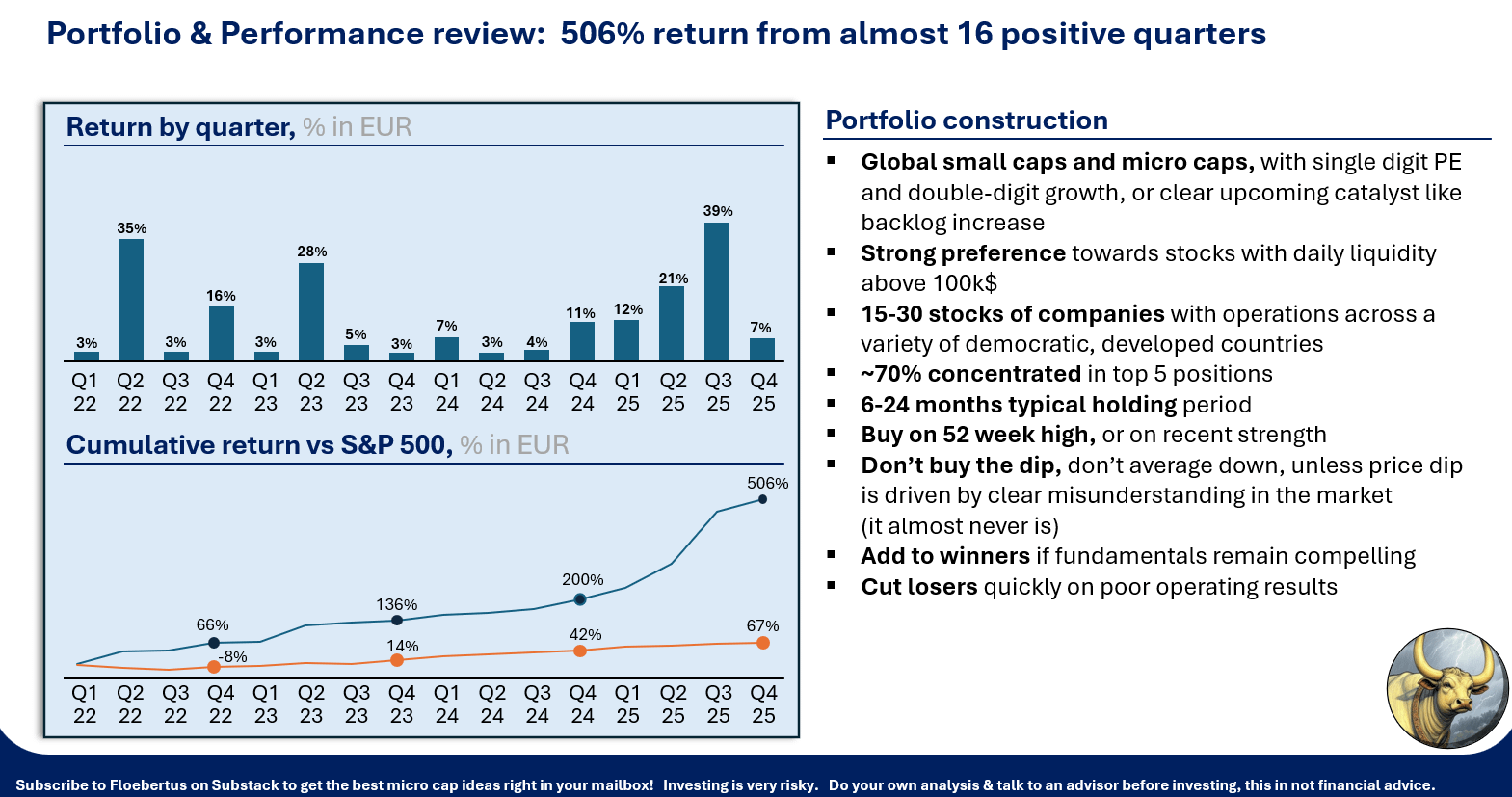

In November, the portfolio was up ~3% again for the month, for a total of over 102% YTD, or 506% since Jan 1st, 2022 vs. 67% for the S&P500. (measured in Euros)

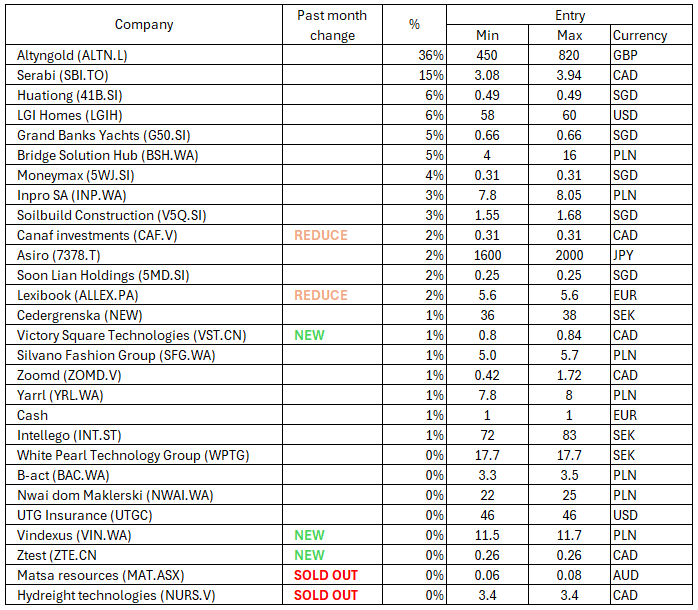

It’s odd to have 16 consecutive positive quarters, but it doesn’t matter. What’s important is to achieve continued longer term returns, without worrying if they come continuously, or if a bit is taken back sometimes. The top 5 positions going into December are:

AltynGold

Serabi

Huationg

LGI Homes

Grand Banks Yachts

Below is the full portfolio and the % allocation of the positions

Not a lot has changed

The thesis laid out in the write-ups on Serabi, Huationg, LGI Homes, Grand Banks Yachts, Bridge Solutions Hub, and Soilbuild is playing out. It has been great seeing them perform well over time. We continue to like and hold them and have not found comparable opportunities in the past month.

Before going through the small changes in the portfolio, let’s reflect on the opportunity in small cap mining stocks today.

Why most smart investors hate small mining stocks

Small mining stocks have performed poorly for almost 20 years, before waking up in 2024. Most investors rightly hate them because

(1) They often create more shares diluting the interests of current owners

(2) They use funds to execute risky capex projects with low returns

(3) When they do a big discovery, they often get taken out by a larger miner

So, generally we should not like miners. The current gold rally provides a good reason to make a temporary exception though, in exceptional times…

What happens to a miner’s P&L when gold doubles?

In late 2023, gold broke through its high of ~$2100 and started a run higher, driven by the loose policies of developed countries. Loose in terms of fiscal policy, monetary policy and in terms of credibility. Russia was moved off the SWIFT system (and its USD & EUR reserves within Euroclear are currently being taken from them). This drives global central banks and investors away from US Treasuries and USD reserves, to gold.

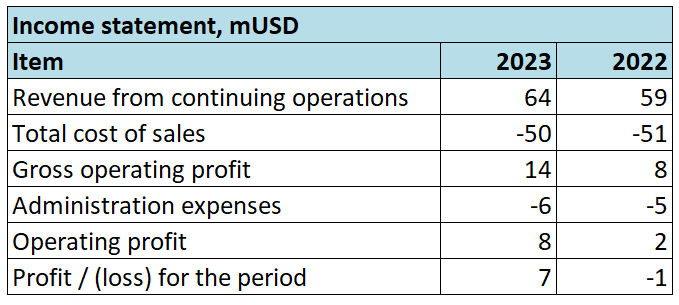

The run in gold has completely changed the economics of these miners, and has created a stock market distortion. Look at Serabi Gold’s 2023 income statement for example, as a baseline:

Nothing extra-ordinary. The market priced Serabi at a $51m market cap, or a ~7x P/E multiple when the 2023 report was published in April 2024.

Let’s do an experiment here. When gold increases 2x, then …

Revenue doubles from $64m to $128m

All operating expenses remain the same

Operating profit increases from $8m to $72m …

Debt and Interest expense quickly disappear …

Net income rises more than ~9x …

Does the stock just 9x then?

Theoretically, we could expect the stock price of the company to 9x over night. In reality though, this is not what happens:

Existing share-holders see their position 2x, 3x, 4x … and start selling to keep their portfolio in balance. Being up 2x on the initial investments in both of our top positions, we are trying to stay out of this “forced seller” camp, looking at the current valuations…

New buyers step in, attracted by lower forward valuations

(and lower convexity of outcomes)

To give the stock its 9x run in this experiment, new buyers have to be found. Not a lot of investors are pragmatic towards gold though. They either like it, or they don’t. This makes it hard to find these “new buyers”. A long and troublesome search for additional owners is started, and the miner(s) meanwhile trade at low valuations.

The mining stocks meanwhile trend slowly higher, not because their “momentum” reinforces itself, but because rebalancing and profit taking by the original investor base, creates an inertia that delays the share price reaction in response to the dramatically improved fundamentals.

Stuck a low valuations forever?

We could wonder if the lack of new owners means that small gold miners will trade at low valuations forever. Fortunately, the answer is “NO”.

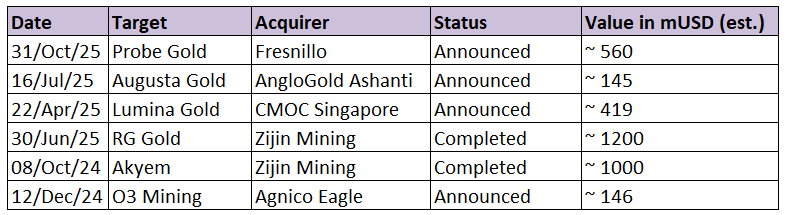

At these prices, every single day, massive cash flows are being generated in the mining sector. The large miners return this cash to shareholders and invest in organic growth, but also acquire smaller peers.

This takes out smaller miners and puts cash in the hands of their owners, who re-deploy that cash into other small mining stocks, helping them re-rate higher

We so far not seen that many acquisitions yet in the sector, although they are ramping up:

Meanwhile, although the process is slow, especially for small companies, new mining investors are attracted by the lower valuations and increasing stock prices, providing a second driver for valuations to normalize.

In theory, markets are efficient. In practice, fund flows take time, and create large temporary market inefficiencies, which pragmatic investors, can benefit from.

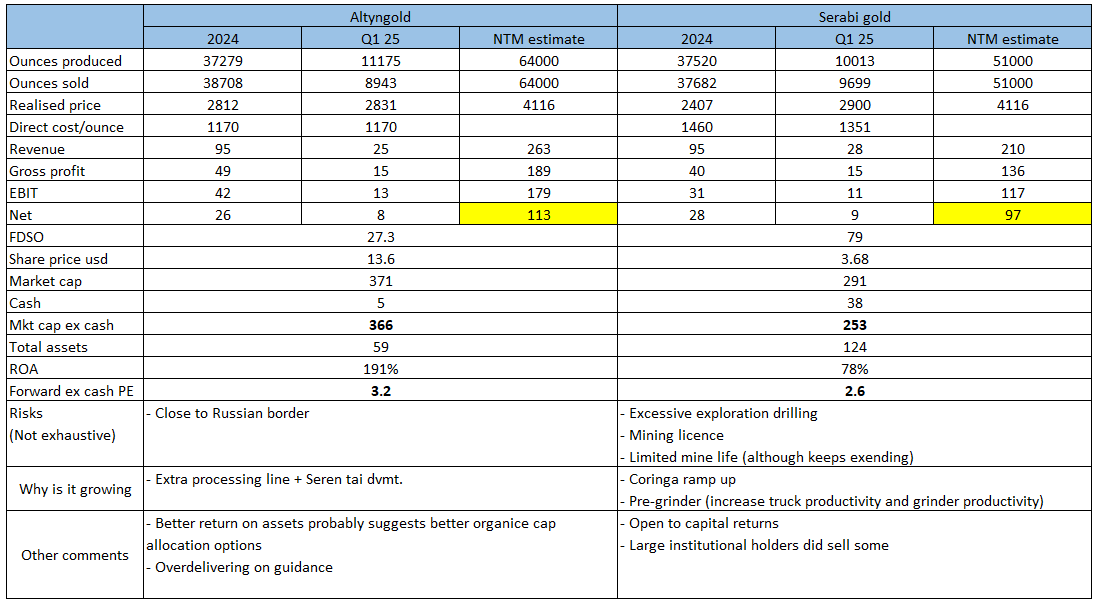

Serabi and AltynGold

The narrative above applies to both Serabi and AltynGold, with some extra spice on top. Both companies are not only benefitting from the higher gold price, but are also ramping up production. Below are their forward ex-cash P/E ratio’s.

We see that these growing companies both trade at ~3x forward net income, with ~100% Return On Assets. We are early in the process described above, and the market still has work to do to price in the strong rally in gold.

3x earnings?

At 3x earnings, SBI.TO earns its entire market cap in 156 weeks. The stock trades at 514 cents CAD today, so it earns ~3 cents CAD per week, organically… without multiple expansion. Management is looking into buybacks and dividends to return part of this cash to shareholders, while deploying part of it to grow the company at these attractive ROA %s.

Changes to the portfolio

Exits

During November, we have exited the following positions as discussed in the chat:

Matsa resources - Balance sheet thesis played out, and sold at ~60% gain

Hydreight - We found a cheaper way to own this through VST which holds twice the amount of NURS shares for every CAD invested, compared to owning NURS directly.

Since the start of December, we have exited 2 very small positions:

Victory Square Technologies - There are several reasons for this exit, which can be summarized by saying we were not comfortable owning it. Main reasons:

The main service Hydreight ( inside VST) provides is to remove regulatory hurdles for medical operators. This does not mix well with having a director run a Discord account focused on Investor Relations, as” The Alchemist”

Hydreight claims to have 3000 Nurses at $3000 license fee per year. This implies $9mUSD x 1.4 CAD/USD /4 = 3.15 mCAD per quarter. The reported revenue from this activity was less than 1mCAD though.

The main growth driver for Hydreight now is pharmacy sales, which has missed managements gross margin guidance in Q3 (reaching only ~10% GM), putting a big question mark on future net profit growth

Insiders are not buying, likely because of 1-2-3 above

This caused us to exit NURS/VST at a ~35% gain. The company is interesting but we should find lower risk high performing stocks.

Zoomd Technologies - We have exited Zoomd because based on the Q3 call, 2 of their main 4 customers are reducing spend. We thought the result was less concerning then the outlook. Zoomd has exceptional management, but if they can’t say “the momentum continues” with regard to the P&L, then it’s likely that the next quarters will also be down in revenue and profits. We keep ad tech businesses on a very tight leash and are happy with the run in Zoomd.

New positions - nothing exciting this month

Vindexus. Entered 0.1% position in November, and already exited it after the company significantly increased CEO compensation to unreasonable levels.

ZTest Electronics. Opened a 0.1% starter position after Trevor Treweeke joined the board. We will watch for insider buying, buybacks and/or business improvement before adding more. ZTest has ~800k CAD net income run rate. We could see them implement quick wins to get this to 1m CAD relatively quickly, which is interesting at a ~3.5 mCAD EV.

Other changes

Slightly reduced Lexibook. Their H2 report indicated difficulties around tariffs, license costs and US competition making the company less attractive in the short term, although still clearly undervalued.

Slightly reduced Canaf. The stock is very cheap, but its limited growth make it potentially less attractive to other stocks that can be found in the future. Its limited liquidity though, make it hard or impossible to quickly act when such a more attractive stock is found. Scaling down that position a bit is a way to enable quickly deploying cash when such a new stock arrives.

Disclaimer

This publication should not be construed as investment advice. Investing involves serious risks, including risk of capital. Do your own research before investing, and size your positions appropriately, in line with your own conviction and your own knowledge of the companies involved.

Looks like Serabi did x12 since 2023, though?

What’s your thesis for the ZTest Electronics? For me it looks really interesting right now. The part with Trevor Treweeke is really nice but the business itself looks really good