February 1st portfolio update (+14% YTD)

Positions, changes and rationale

It’s a pleasure to provide the February portfolio update. The year 2026 has started well for investors. As always, we review performance, current positions, and the latest changes.

Performance

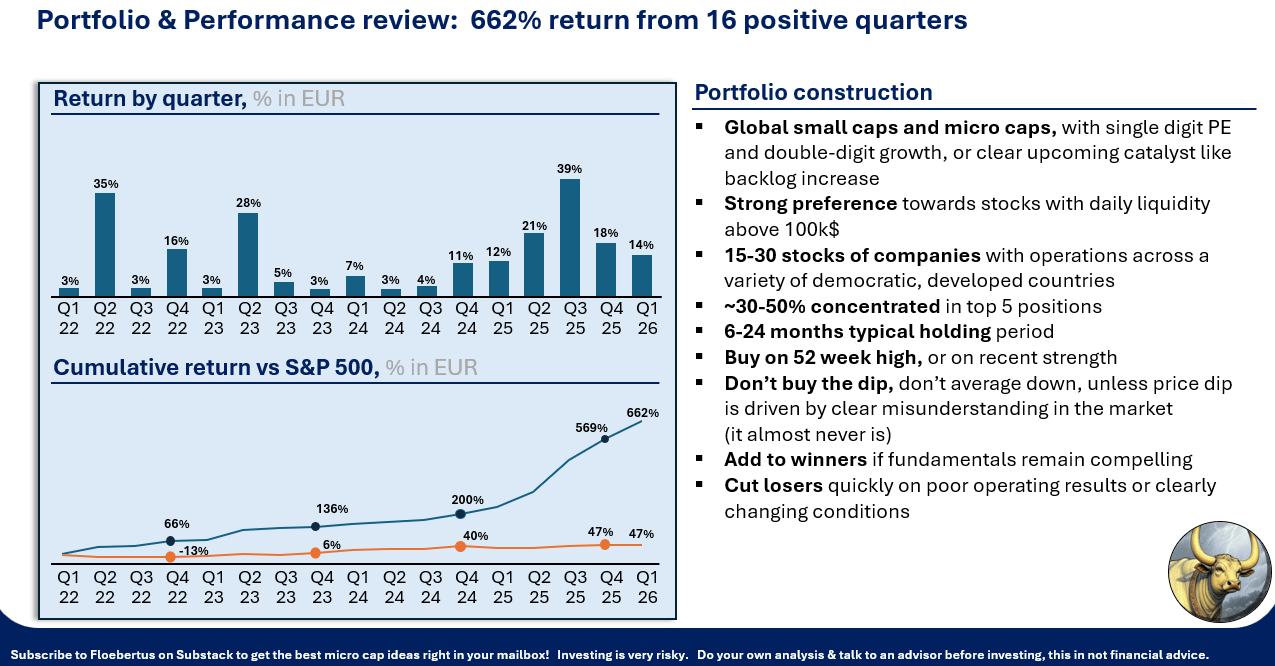

The portfolio was up ~14% for January 2026, for a total gain of 662% since the start of 2022, versus 47% for the S&P 500 Total Return (EUR).

I saw an interesting conversation this week, where Ian Cassel, the founder of MicroCapClub, spoke with Tobias Carlisle and Jake Taylor, two great value investors. The part that interested me most was the discussion around buying the dip vs adding to winners.

Ian explained—referring to The Art of Execution by Lee Freeman-Shor—that the most successful fund managers don’t have a high hit rate. In their stock selection, they are wrong most of the time.

What then makes these elite fund managers successful? Well, they exit quickly and keep adding to their winners as conviction grows and the thesis plays out.

While this is obvious to most micro and small cap investors, the value investors were very surprised. They are used to going through 52-week low lists, buying stocks at their cheapest, providing maximum margin of safety, on the assumption that the underlying value hasn’t changed.

That last assumption is exactly where most micro and small cap investing is different from pure value investing. The large majority of tiny/small companies we are looking at are clearly not as dominant as Nvidia, or Alphabet, or even challenged large cap companies like Duolingo.

Even though we all try to select the strong business model companies from the universe of micro-caps, the above statement means that the prior probability of success (before we filter going through report and filings) in micro-caps is much lower than in large caps.

Small/micro cap investing is like fishing in the dirt, trying to find exceptional companies where they usually aren’t to be found. This is why in small cap investing, it pays to buy new highs, but sell early when conditions deteriorate. Add slowly as things improve, get out pretty fast when something breaks.

Fast here doesn’t mean minutes or even days. Things typically play out over time, so we have time to analyze, understand, and then act. Many investors freeze when things go wrong. They are caught by stress and inaction.

In the excellent book “On Grief and Grieving: Finding the Meaning of Grief Through the Five Stages of Loss”, Dr. Elisabeth Kübler-Ross and David Kessler explain how the first stage of grief is denial and isolation.

Not Fear or Anger. Rather, denial and isolation is the first thing we feel when things go wrong. The mind and body want to find a safe place to start processing things before accepting them.

As Ian explained, and as Lee Freeman-Shor explained, the most successful investors get out quickly when things fundamentally change. They quickly understand and accept reality and move on. Conversely, they add to companies that are improving (even if the market doesn’t recognize the improvement).

I try to apply these principles as well, because I noticed over time they worked. Having said that, while the companies I look for are exceptional, I don’t pretend to be an exception to what Dr. Kubler-Ross wrote in her book on human psychology.

In the Portfolio update below, I will measure if I applied these ideas well over the past couple of months, and how that worked out.

First, let’s look at the current portfolio and what those changes were.

Portfolio

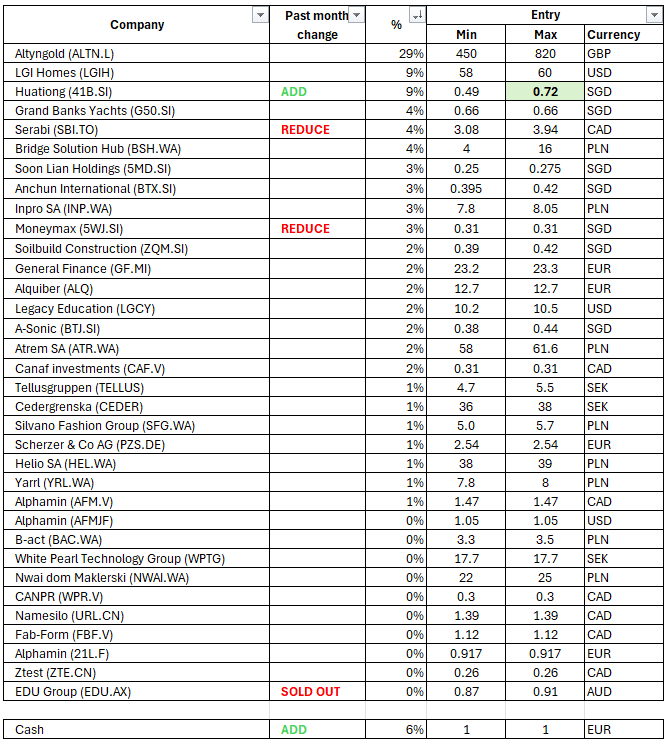

The top 5 positions going into February are:

AltynGold

LGI Homes

Huationg

Grand Banks Yachts

Serabi

Below is the full portfolio and the % allocation of the positions

Changes

All changes were made on Thursday/Friday this week except EDU Group, which was sold a bit earlier, whenever I mentioned about going to sell it in the chat:

Sold EDU Group.

The context of the company is getting more risky, driven by:November 2025 MD117 - A new Direction by the Ministry of Education to further de-prioritize visa applications related to students willing to enter schools which have already exceeded their National Planning student threshold. (majority of students in EDU group impacted, not clear if the MD will be adhered to or if de-prioritization will have impact)

December 2025 Bondi beach attack

January 2026 amendments to the National Code for Providers of Education and Training to Overseas Students, banning commissions for agents finding students interested in changing schools within Australia.

The combination of these events makes it more likely that EDU Group will not be able to enroll the same number of foreign students in the future, putting their business model at risk. The outcome is too hard to predict here, even though I expect 30% growth for EDU in 2026 (trading at 6x 2026 P/E). We will know more when they post T1 or T2 enrollments.

Added to Huationg

Huationg has a growing construction business as mentioned in the post below. As the company has been hiring and did a small capital increase to raise funds for working capital, it is becoming very likely that growth will continue. The company has TTM net margins of 6-7%, which are likely to expand, driven by

(Higher revenues diluting fixed costs over a larger base)

Continued low inflation, protecting margins on long-term contracts

Continued strong public and private sector investments in construction in Singapore, creating a “seller’s market”

Both of the 2 transactions can be seen as an application of the mandate in the slide on top which says “Add to winners if fundamentals remain compelling” and “Cut losers quickly on poor operating results or clearly worsening context”.

It’s not certain, that these decisions will make money in the future. All I know, is this process has been working for a while, and I keep applying it, and tuning it if needed, while doing my best to look at as many great companies as possible.

Reduced Serabi

I have mentioned a couple of times now in the past 6 months, that gold is a trending asset, which means just hold it on the way up.

Gold usually sits in boredom mode. Savvy (grumpy) wiser investors are then telling each other that gold is a pristine asset, and the government is printing too much fiat… They say “the market is too stupid to care” when gold has done nothing for 1-10 years…

Sometimes though, gold goes into sunshine mode. Gold makes new highs, and everything makes sense. The higher it goes, the faster it goes, the stronger the story becomes. Governments, investors, banks are all getting on, and agree that cash is trash.

The time gold stays in this second mode is shorter than the time in the first mode, but still last years, just looking at the past gold bull markets:1976–1980: ~700% gain, during the 70s inflation years (until Volcker)

2001–2011: ~650% gain, after tech-bubble and through GFC stimulus

Dec 2023–Present: ~133% gain, driven by declining appeal of US Treasuries and Euro/Dollar reserves due to low real interest rates and low trust in Western governments.

It’s interesting to note that the previous 2 bull markets ended when interest rates changed upwards. Investors then replaced gold by (government) bonds.

Gold ended January like it ended December. Significantly higher, but very volatile. Whether the current rally will last as long as those in the 70s or 00s is impossible to predict. What we do know, is that the sentiment of the past few weeks is probably too optimistic, and that typically in the past, bull markets last significantly longer than the 2 years we have just seen and don’t typically end in years when governments around the world cut interest rates. A good scenario for gold to decline would be if oil doubled in the next 3-4 months and the fed started raising rates to cool down the economy to avoid inflation.

Putting all the facts together, gold miners, at their very low valuations, still look very interesting (Many trade at 2-6x earnings with 10-20 years of reserves). The risk level of the situation has changed slightly from ~Q2 last year though, as there’s clearly more optimism and volatility in gold, posing a risk to the ongoing trend.

This is why, just like in December, I have cut back a bit more on 2 gold positions (Serabi gold and Moneymax). Serabi in particular, not only is exposed to gold price risk, but also carries some risk from their ongoing expansion of the Coringa mine (both licensing and resource risks).

I think investors are likely well rewarded for those risks (Serabi trading at < 3x 2026 earnings at 4900$ gold). However, as gold was down 12% to $4600 at some point on Friday, putting more risk to the gold trend, I decided to take some profits on Serabi, from a risk management point of view.

Expect some volatility. As the waves go up and down, so do the birds sitting on the water. The strongest will fly up, while the weaker might go under. The trick is not to avoid the waves but to find the strongest birds.Reduced MoneyMax

Everything is currently going well at Moneymax. Gold and silver are doing well, drawing people to their pawn shops to bring in items in exchange for credit. Existing pawned items can even be used to finance more credit, bringing in more interest income for the company. New pawnshops immediately provide high returns on investment as customers flood into the doors… The company will very likely post great operating results for H2 2025 in February.

There’s a big difference in how pawn shops vs mining companies are linked to precious metal prices. While miners benefit from high commodity prices, pawn shops like Moneymax benefit from rising commodity prices. While I don’t have a high conviction opinion on whether gold prices stay high, I do hope it’s fair to say that they will not continue rising steeply forever.

This means a moderation of pawn shop results is likely, whenever the pace at which commodity prices rocket higher cools down (as of H2 2026 ?). This will lead to a normalization of growth and margins for Moneymax. (while miners will continue to print cash)

Both of the 2 transactions cannot really be seen as an application of the mandate in the slide on top which says “Add to winners if fundamentals remain compelling” and “Cut losers quickly on poor operating results or clearly worsening context”. Gold is up 12% YTD even after yesterday’s drop.

These 2 transactions are therefore mostly “portfolio risk management” changes. These typically cost money but (in theory) provide consistency and downside protection.

Adding to existing positions vs. taking new positions

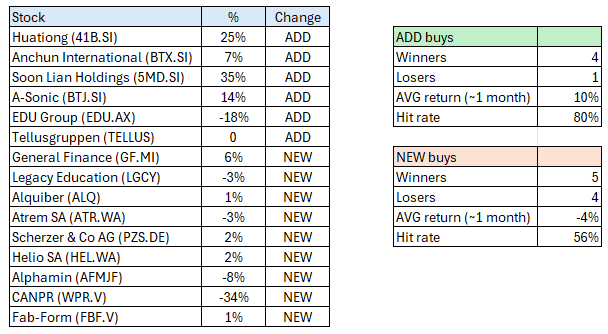

Looking at the ADDs to the positions in December and early January, we see why adding to small well performing companies is powerful.

A nice 80% of the additions worked (Average 10%)

Only 56% of new buys worked (Average -4%)

I’m not showing this to over-analyze my own trades, but rather because I think this is very common. Adding to stocks because we know very well and we know are doing great, often works out.

Main dish?

One attentive reader pointed out that after the “Appetizers” post of January 1st, no main dish has arrived yet. We will need to be a bit patient here though. While finding great microcaps is amazing, our focus has to be on searching them.

Carefully searching, understanding more and more companies in the world. Then suddenly finding an insight worthy to put the hammer down. That’s the focus.

The goal is firstly to “search well”, rather than “trying to find” a new stock idea. When we try to find, we are always successful, but we accept mediocre ideas. When we try to search, we have no measure for success, but the best ideas will somehow find us anyway. That’s how it works for me anyway.

Conclusion (or lack thereof)

If you like any of the ideas or stocks above, this post will not bring a clear conclusion. Make sure to read about the company, get to know them, or discuss them with your financial advisor. Feel free to give the CEO a call.

My goal is to share what I’m doing in a transparent way, trying to optimize my process of building a portfolio of winning companies. It’s been great sharing this to understand it better myself, while getting feedback from readers.

It does come with a sort of “lack of conclusion” though, because well (1) I can’t tell you what to do because fortunately that’s not my responsibility and (2) I can’t even really tell you what I’m going to do, because then I probably would have already done it and (3) There’s really no indication that what I will do in the future will work out or have any benefits.

Thank you

Disclaimer: This is not investment advice, please speak to your adviser before investing, and please do your own work analyzing the company.

I am new here so have a couple of questions. Do you have any write-up of your trading process? Such as selection criteria and entry and exit criteria. In addition you mentioned letting the winning stock run. But what are your criteria for exiting a stock that has appreciated a lot? Thanks!

Great post floe. Your writing has improved tremendously