Fighting gold with gold !

New write-up on Serabi Gold plc

Ticker: SRB.L Price: GBp 215

Basic/ FD shares: 75m / 78m Market Cap: GBP 163m (USD 213m)

Net cash/debt: +25m (30m-5m) The company reports in USD

Overview

Serabi gold is a profitable unhedged gold producer operating the Coringa and Palito mines in Brazil.

The company is executing on increasing gold production from 33k ounces in 2023, 37k ounces in 2024, to ~45k ounces in 2025, and further to 60k ounces in 2026 and ~100k ounces in 2028.

This ongoing increase is fully funded by operating cash flows. Capital is used efficiently by using ore sorters at both Coringa and Palito, increasing the ore quality by removing dirt and rock, before feeding the ore into the existing processing plant at Palito.

At the current gold price of ~$3,528/oz, Serabi’s forward 12-month revenue is estimated at $180m, with $98m gross profit and $68m net profit. At the current $213m market cap, with $25m in cash, the company is trading at a 2.75x forward PE.

CEO Mike Hodgson says: “We’re going to generate a lot of cash this year. I don’t think our current shareholder base would like us to sit with that amount of money, so we are looking at all kinds of mechanisms available for shareholder returns. Some prefer buybacks and some prefer dividends“

Deeper company overview

Serabi runs underground gold mines in the state of Pará in Brazil and has a team of ~850 employees. The company was founded in 2004 and is led by CEO Michael Hodgson who joined in 2007. Serabi has balanced production income and exploration costs over the years, and is now stepping up both, supported by a higher gold price and the start-up of Coringa mine which it acquired in 2017. Both assets are 100% owned without external royalty obligations.

Palito

The Palito Complex comprises of the Palito and São Chico narrow vein underground gold mines. This Complex has been in production since 2012 and yields around 40,000 ounces annually. Serabi has continued developing and exploring both mines over the year, keeping proven and estimated reserves constant.

Ore mined at Palito is crushed, x-ray sorted and processed into gold and copper-gold concentrate using the process below. Total current capacity is 650tpd, or up to ~60k ounces of gold output. This output is the total current capacity of the company, as input material includes sorted ore from Coringa.

Coringa

Coringa is Located 200 km south of Palito and was acquired from Anfield Gold Corp (now part of Equinox Gold) for $22 million in 2017. The asset is comparable to Palito, but before Serabi started mining it in late 2023, only artisanal surface level mining had taken place.

Serabi likes the asset because although measured grades are slightly lower than those measured at Palito, they come in wider veins than those at Palito. The rock can also be optically sorted to ~10 g/ton ore, thanks to clear color differences between useful ore and surrounding dirt and rock. The optical ore sorter at Coringa was commissioned for production in October 2024.

The Coringa asset is more sensitive than Palito, because it’s much closer to Indigenous lands. The mine is only 30 km away from Baú, which locates an indigenous settlement with ~200-300 people. The broader area to the East is home to several other contacted and non-contacted villages.

The local people have suffered from the effects of small illegal gold miners for years, causing mercury poisoning and violence with several indigenous being killed. In fact in 2017, before Serabi bought the asset, the government ruled that no further licenses would be awarded until Coringa’s potential impact on the indigenous communities was better understood. This ruling was repeated in 2021.

Serabi has worked hard over the years to be a positive influence in the region and build good relationships with locals. The company provides local infrastructure improvements, healthcare, reforestation and clean ups of artisanal or illegal mines. Management has meetings with local indigenous and non-indigenous on a daily or weekly basis.

The relationships Serabi has built over the years, led to approval of Coringa’s trial mining license in January 2024. The license allows Serabi to mine, sort and truck out 50.000 tons from Coringa to Palito, supporting their 2026 production goal of 60k ounces. Serabi is working with SEMAS to obtain a full permanent mining license, which requires more extensive environmental impact studies.

Serabi has relocated part of its team from Palito to Coringa in late 2024 and early 2025. The company plans to further ramp up the ore sorter at Coringa and feed it mined ore rather than historically stockpiled material. This will improve ore quality shipped from Coringa to Palito and enables H2 gold output of 24-25k ounces at Palito.

Other assets

Serabi holds additional assets in the region that are less significant, notably the Matilda prospect, which generated revenue through an exploration alliance with Vale from May 2023 until its termination in April 2024.

Financials & Valuation

The company projects ~55 000 ounces of next 12 month gold production. Working conservatively with 51k ounces, at a realized price of $3528/oz, forward revenue is $180m. (We use ~98-99% of current gold spot which seems to be what Serabi realizes historically)

Serabi had COGS per oz production of 1572$ in H1 2025. At forward 51koz this leads to 80m COGS or 100m Gross Profit for the next 12 months. The Brazilian Real has appreciated ~2% over the past months. Incorporating this currency headwind, we estimate ~98m Gross Profit for the next 12 months.

SG&A was $7.5m for H1. We estimate NTM SG&A to be $18m, for EBIT of $80m. The company will pay ~0 interest in the coming year and is taxed at 15%, leading to $68m NTM net earnings.

Taking out the 25m net cash from the 213m market cap, Serabi trades at 2.75x forward earnings.

Given the growth prospects of the business, we think fair value is ~7.5x forward earnings, or ~540 mUSD = 6.9 USD/share = 5 GBP or 9.6 CAD per share.

This valuation is 2.3x today’s share price.

Capital allocation

Serabi will likely use ~10-15m for exploration capex and capacity increase upgrades. We think these investments are very sensible as they enable Serabi’s planned expansion to ~100k ounces by 2028, using a hub and spoke model, where pre-sorted ore is shipped from developing mines, to the Palito processing plant.

The relatively small need for investments enables Serabi to return capital to shareholders, which it intends to start later this year, through dividends or buybacks.

Ownership

Serabi is owned by Starboard Asset Management (20%), as well as a range of small institutional investors and retail investors. Insiders own less than 1%.

Serabi historically was owned in size by Fratelli investments Ltd and Greenstone Resources, who sold most of their stake to Starboard and other institutional investors.

Fratelli sold most of their shares in April 2025 and is still actively reducing its position. The company entered their investment in 2012-2014 and provided Chairman Nicolas Banados. Mister Banados left Fratelli (Megeve) in June 2021 and left Serabi in January 2023, removing the historical connection between Fratelli and Serabi.

Risks

There are 4 main important risks:

1. Ore quality. Mining is risky as results vary significantly driven by ore quality. Initial results from Coringa have been good, but possible deterioration in quality is a significant risk.

2. Coringa license. The Coringa mine is currently running on a preliminary license valid until January 2027. If the license is not converted into a permanent production license, the company may lose the benefits from its main asset. It may be a bit controversial, but we think this risk is extremely limited. Serabi provides value for local communities and is a better steward of the Coringa mine than the prior owner was, which resulted in the approval of Coringa’s preliminary license in early 2024. It’s very uncommon for a mine to obtain this preliminary license but not receive a permanent operating license.

An example of a project in the Para state having their permanent license denied, was the Volta Grande project. They had their license denied in 2017 due to insufficient analysis. In January 2025, a judge ruled the state authority SEMAS capable of providing said license, rather than depending on federal environmental authorities. This paves the way for Volta Grande to get a permanent license, removing a rare exception.

Also in 2025, federal funding for indigenous communities in Brazil was cut by 20%. We think this is increasing the importance of the role of both states and professional (legal) miners towards improving the safety and development of their local communities.

3. Capital allocation. Miners traditionally burn cash on crazy adventures. We think for Serabi this risk is limited by the size of the profits and the CEO’s explicit focus on organic growth and capital efficiency.

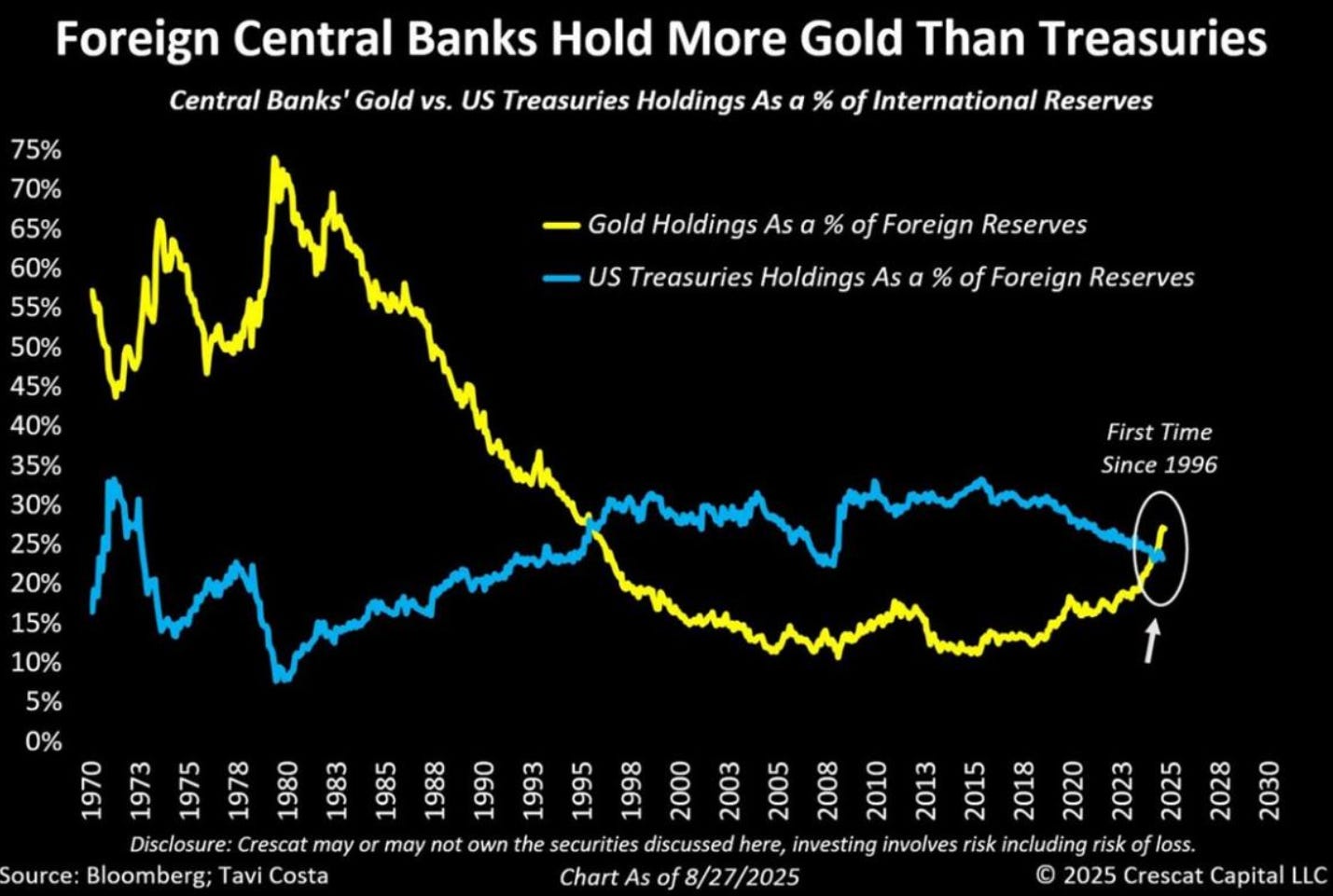

4. Gold price. For $100/oz change in gold price, Serabi’s net income shifts ~$5m up or down. Gold has rallied significantly in the past years, driven by interest from developing market governments after Russia was removed from SWIFT. These countries might continue to prefer shiny rock money over mutable orange man money or digital rocket money.

Why the opportunity exists

Price lag. As gold rises, the profit margins of gold miners explode upward, and their growth projects become exponentially more economic. Temporary multiple compression is caused by existing investors rebalancing out of sky-rocketing mining stocks.

License risk. We think the market is overestimating the risk of Serabi’s permanent license for Coringa being denied.

Historically bad sentiment towards miners slowly turning as mining has become much more economical.

Optically not that cheap. The current gold price is not visible in Serabi’s P&L yet, making the company harder to find and optically less cheap.

Mean reversion thinking. Investors seem to think gold prices will revert back to where they were. We appreciate this from an owner’s point of view when planning capex projects, but we think equity investors should work with the current spot/futures price, because gold has never been mean-reverting.

Further reference

Crux investor interview with Mike Hodgson:

Summary

Serabi is a profitable growing miner trading at 2.8x forward earnings which we think will double as the higher gold price runs through the income statement. Investors should investigate the risks

Disclaimer: Not investment advice. Talk to an advisor before investing.