June portfolio update (+666% vs 66% S&P)

It’s a pleasure to provide the June portfolio update! Let’s dive straight in.

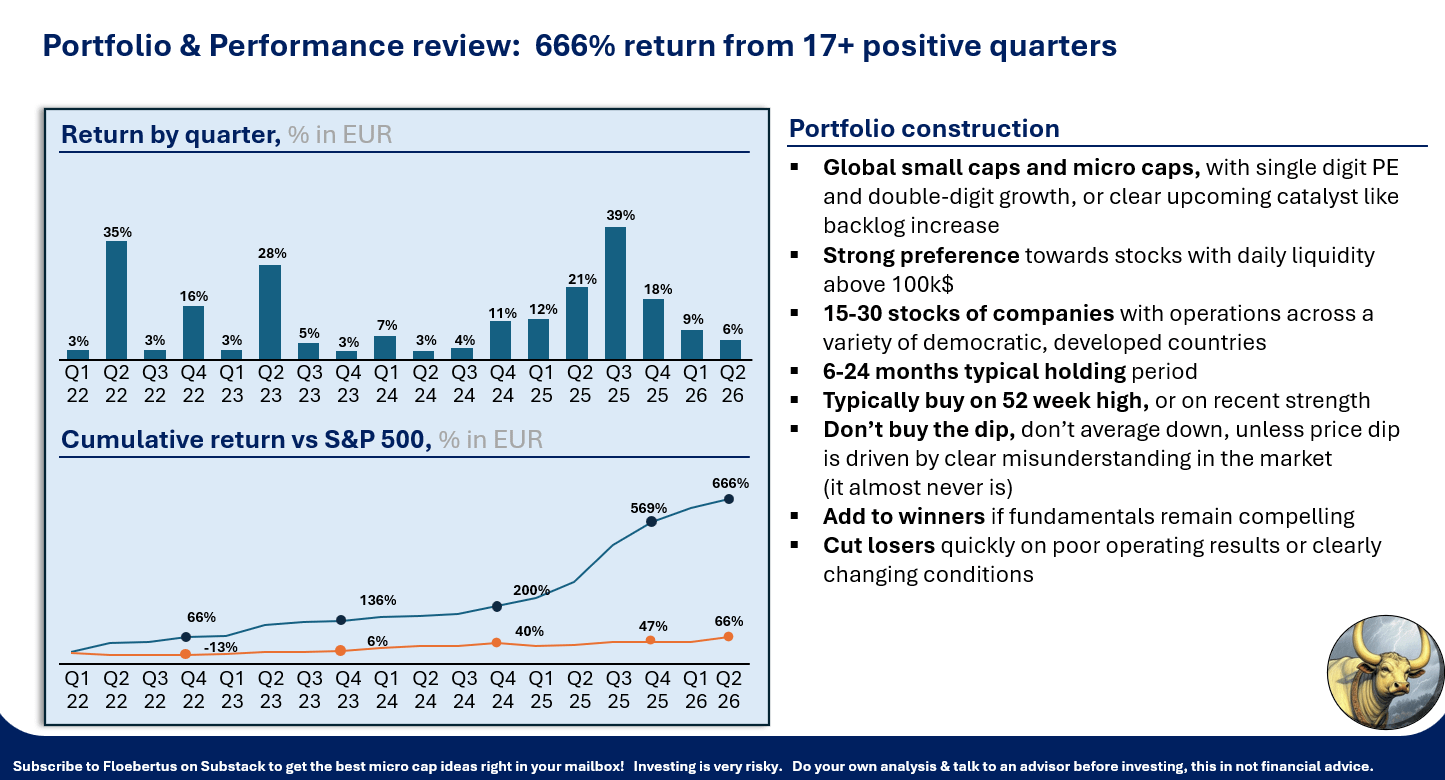

Performance

The portfolio returned 15% year to date, compared to 12% for the S&P 500 expressed in EURO. Closing in on a potential 18th consecutive positive quarter.

The portfolio is currently not live available to subscribers as that would encourage too much copy-paste trading, exposing you too directly to my mistakes.

Subscribers have done well doing their own analysis of my write-ups though, which actually have performed better so far this year, up 19% on average since pitch.

It may take a minute before the next stock idea is out. I have been looking at a couple of interesting companies but didn’t find them good enough.

This morning DBA Group reported. They look pretty interesting with ~5m net income + 2m goodwill amortization, trading at ~7x owners earnings while guiding continued ~5% growth and typically outdoing guidance ~5%. Their growth mainly comes from acquisitions though, and bolting on ~5mEUR acquisitions onto a 130mEUR company every couple of months is not the best possible long term strategy. So I did not revisit them although they look interesting.

Looking across my pitches a bit longer term, I have made 15 of them since the beginning of last year.

When I wrote them, I felt highest conviction on OKP, Soilbuild, Lincotrade, Alquiber, Huationg and Generalfinance, and I had a bit more doubts on LGI Homes and Grand Banks Yachts.

This conviction level, with some statistical ups and downs, did translate into better results for the high conviction companies. When I wrote up LGIH and Grand Banks Yachts, I was starting up the Substack and hoping it was going to work out well… I was trying to put enough ideas out.

I think both were and are good ideas, but the others are clearly better. Going forward, my focus will continue to be finding many great ideas, and posting write ups on only the most excellent companies regardless of my post frequency.

May 2026 market events

In the past month, the S&P500 was up 6%. I saw a fund manager explain his 2025 underperformance by saying something like “the S&P500 is exceedingly driven by a small number of irrational large cap stocks… ”

Let me disagree here. I think the large cap market is quite rational and while valuations are getting stretched, I think they should be.

The reasons valuations are high, are those we reviewed last month:

Increased GDP growth because of AI capex

Increased productivity because of automation & low hiring due to AI fears

Disinflation driven by productivity and tariff effect roll off

Fed reducing interest rates (after 1-2 interim hikes in 2026)

I think that while the bond market is correctly starting to price 1-2 rate hikes in 2026, equity investors can already look beyond 2026 and see rate cuts coming in 2027-2028, which will further drive up corporate profits and valuations.

In any case, it’s ok to underperform, but take it as a learning opportunity. Don’t fight the market.

Portfolio

Below is the portfolio as of May 29th: