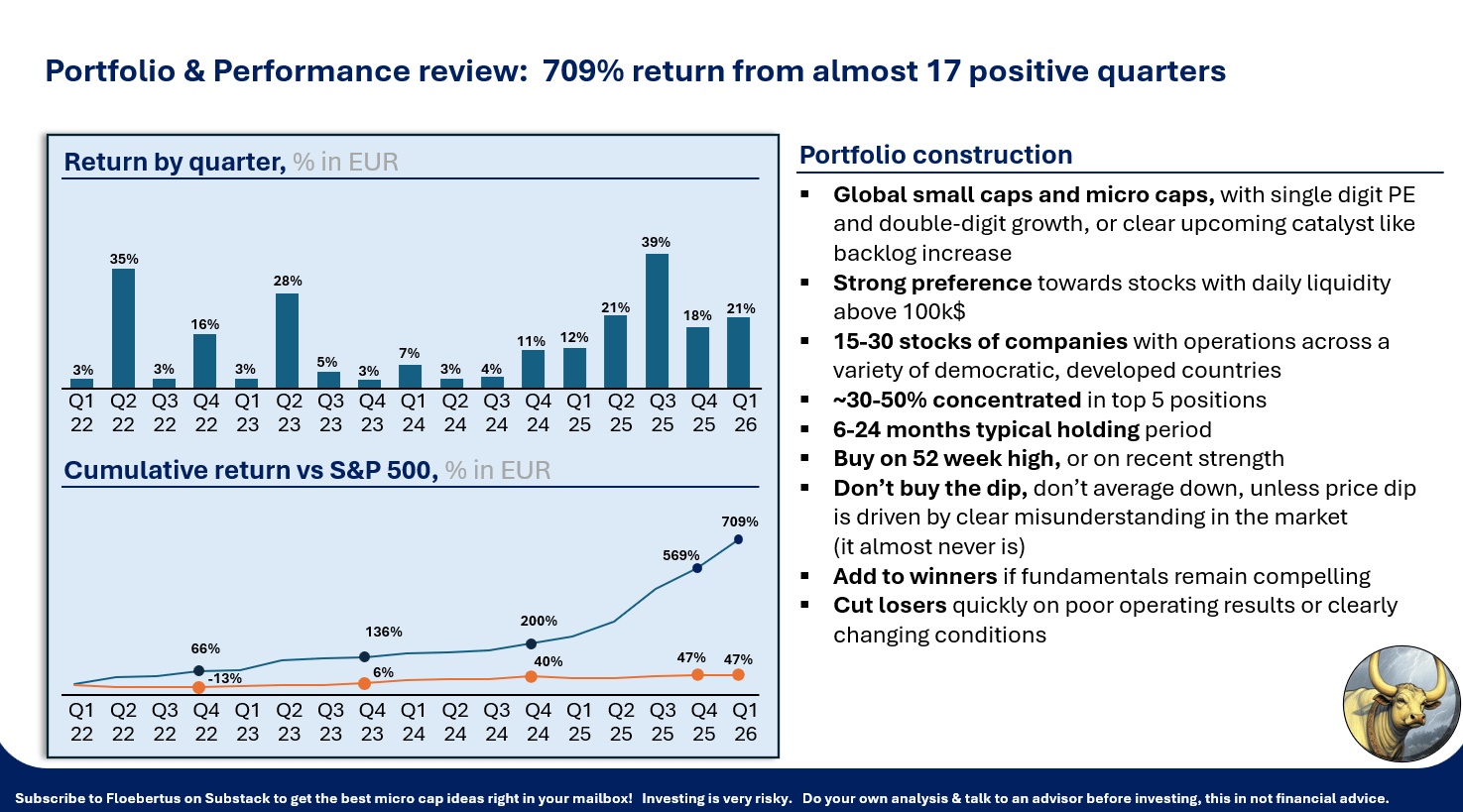

March portfolio update (709% vs S&P500 47%)

Positions, changes and rationale

It’s a pleasure to provide the February portfolio update! The month was full of interesting earnings reports. Let’s dive straight in.

Performance

The portfolio returned 21% year to date, compared to ~ 0% for the S&P 500. We look ready for a 17th consecutive positive quarter.

The portfolio is currently not live available to subscribers. I’m afraid that would encourage too much copy-paste trading, exposing you too directly to my mistakes.

Subscribers have done well doing their own analysis of my write-ups though, which have performed similarly well:

February 2026 market events (old man rant)

In Feb 2026, the market realized SaaS business models were prone to AI disruption, triggered by comments from Anthropic CEO Dario Amodei:

“An AI tsunami is coming”

His words provided context for the exceptional performance of Anthropic’s latest Claude Opus 4.6 model, including Cowork and Code.

As an investor, it’s fine to agree or disagree with Dario. Take a good look at the world, and form an opinion. While doing so in 2026, I think it’s helpful to check out, and be surprised by Claude Opus 4.6, while forming an opinion. I have used it to update my positions table below, right in Excel, based on screenshots of my latest positions. It updated positions, currencies and latest prices. Surprising and handy.

I think the market is still underestimating AI. I wrote a screener for Polish stocks in early 2024 using GPT-3.5, over a year before the market started selling off FactSet, the financial data provider… It took me 4 hours.

The AI disruption in SaaS is similar to the disruption telecom providers and cable TV providers faced when the internet came along… It won’t kill companies like a fox in the night, leaving nothing behind. Rather, it will clip away their pricing power piece by piece until there’s nothing left… Criticism of AI’s limitations will evaporate, just like our complaints about dial-up internet connections did…

I have seen this movie before and I would suggest: Don’t fight the market on this…

Electric light was commercialized less than 150 years ago. Don’t try to be a genius by underestimating technological progress!

Changes and Portfolio

In this section:

A review of the 6 new positions

All portfolio moves and their rationale

Full portfolio with % allocation and change vs last month

New positions:

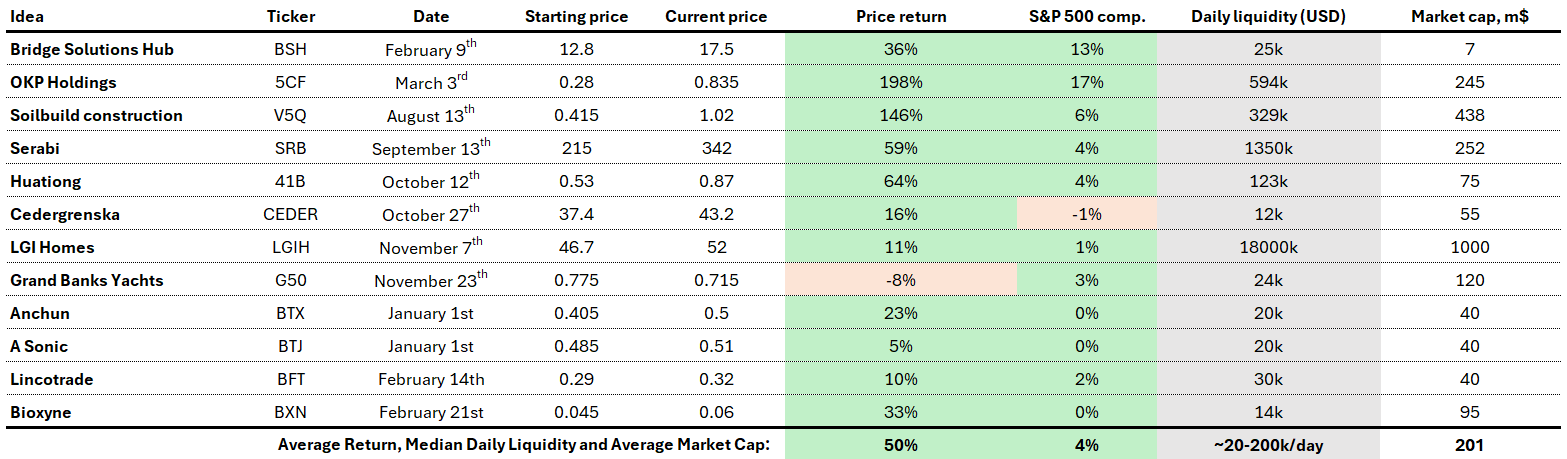

1. Lincotrade (BFT.SI)

I love these kind of Singaporean construction companies which report growth, profitability and backlog visibility all at the same time. I try to know and follow many of them, to increase the odds of being able to swing at a perfect earnings report like the H1 2026 Lincotrade reported.

Driven by data center demand, Lincotrade reported revenue up 58%, net income up

> 400%. Order book doubled in 12 months. Looking a bit deeper, we notice a new factory coming in March 2026, and insiders still owning ~80% of the company trading at ~5x run rate earnings plus cash.

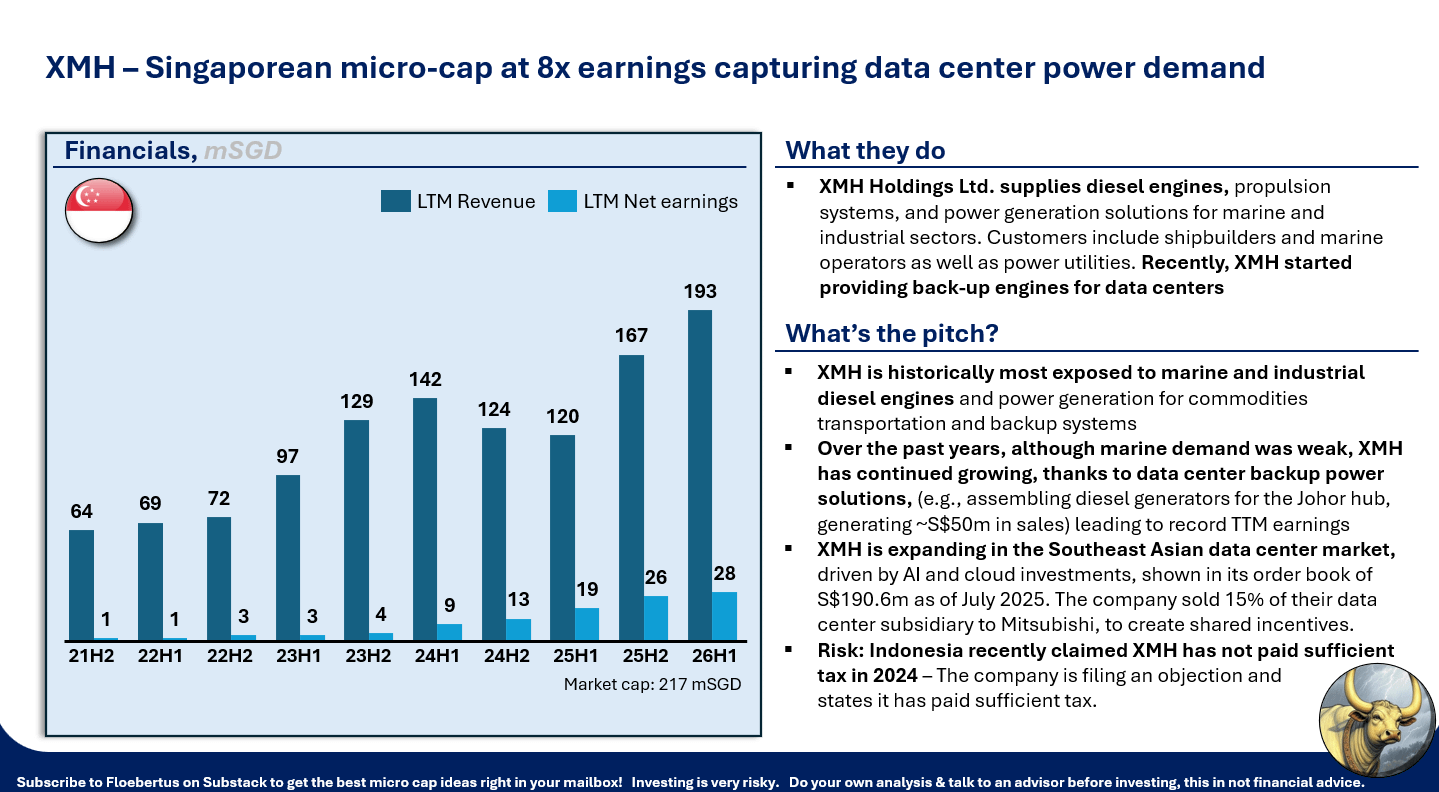

2. XMH Holdings (BQF.SI)

This is a Singaporean power solution provider, mainly to marine and data center sectors. When you build a ship, or a data center, and you need a propulsion engine, or a backup power generator, then XMH will engineer this for you. They select and integrate a commercial engine, gearbox, shaft, bearings and other parts. They have custom solutions and (semi-)standardized solutions. The company is founder led has been growing for years, but trades at only ~8x P/E.

XMH’s solutions were recently recognized by Mitsubishi for their exceptional assemblies. Mitsubishi not only selected XMH as a preferred partner, but also bought up 15% XMH’s data center subsidiary, providing the company with working capital for growth. A nice win-win.

An unclear backlog, and Indonesian tax issues, caused me to hold off on buying shares in XMH for about a year (price rising from 0.90 to 1.70 SGD).

It looked good, but there was no way to build confidence. No way to suggest that the data center projects were not a one-off… Or two-off…

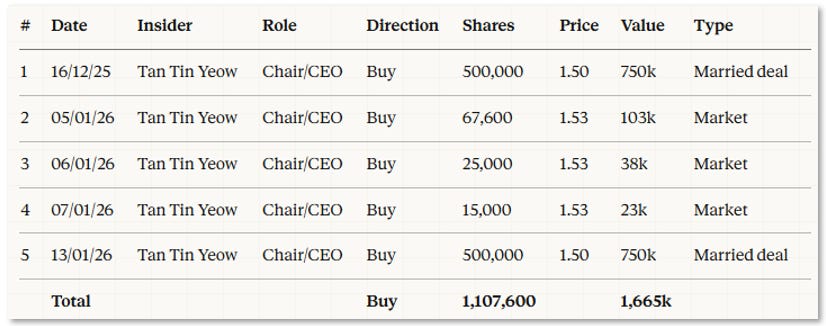

That was until 2 large insider buys… This was the missing piece for me:

Looks watertight? It never is. I have seen the weirdest reasons why CEOs buy shares. Avoid delisting, avoid lawsuits, avoid bad perception… I have a good impression of this one though. Founder, good fundamentals, big buys.

Time will tell… (Married deal = large block agreed between large owners)

3. Bioxyne (BXN)

Medical cannabis producer growing over 100% and trading at 7-8x 2026 earnings.

I wrote this article on the company last week, just before the company raised guidance.

The write-up already suggested that they would meet guidance on revenue, but beat guidance on EBITDA. The company posted their Q2 cash flow statement in January, making it clear that

(1) Inventory was rising …

(2) Capex investments were being made …

(3) Some suppliers were being pre-paid …

(4) Cash was rising …

Put these things together and it was clear EBITDA/ net income would be great.

I will be reaching out to the company for some more perspective, answering some of the open questions in the article. They sounded very optimistic in the H1 call, but didn’t really provide hard data on their international expansion.