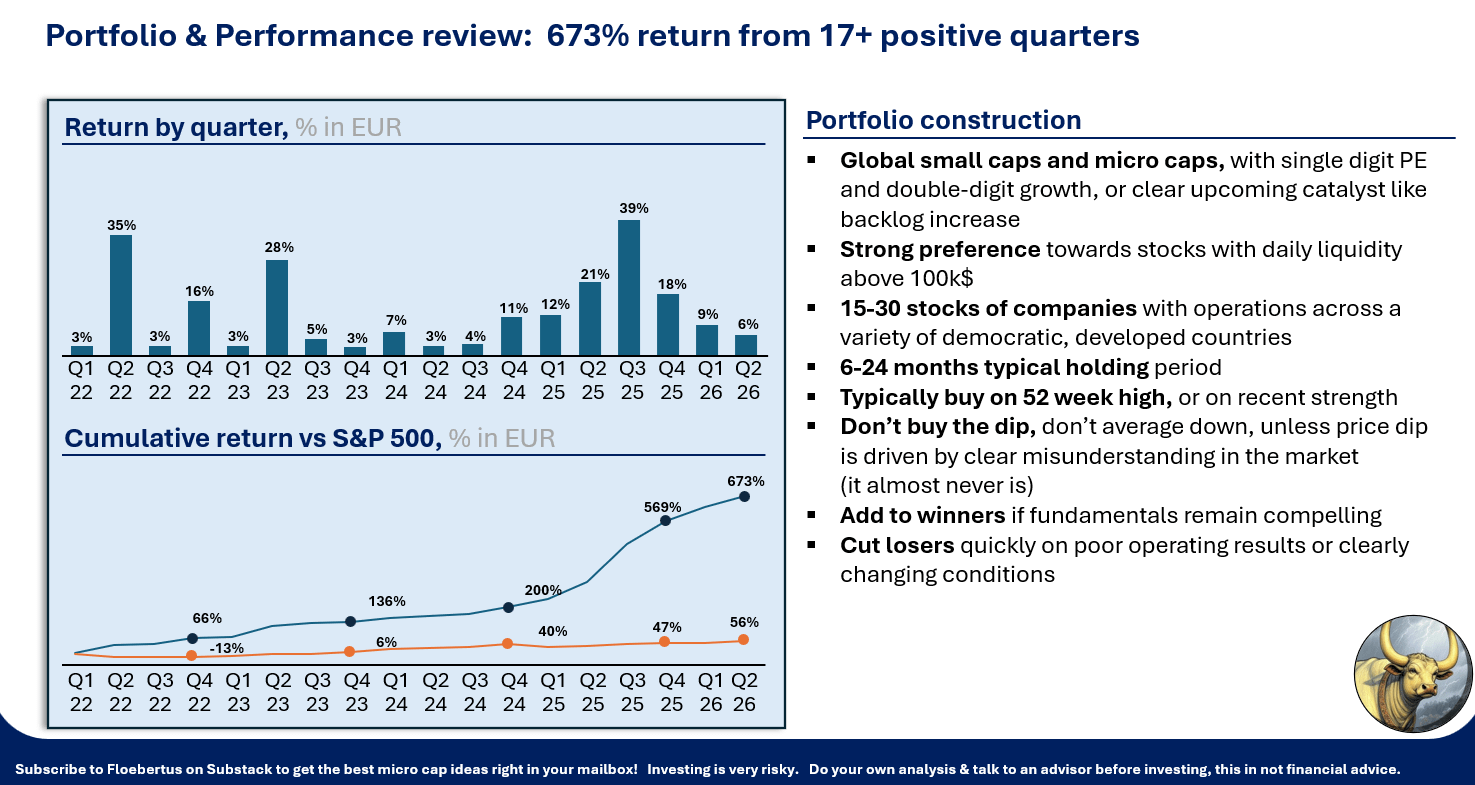

May portfolio update (+673% vs 56% S&P)

16% YTD applying the small cap advantage

It’s a pleasure to provide the May portfolio update! Let’s dive straight in.

Performance

The portfolio returned 16% year to date, compared to 6% for the S&P 500 expressed in EURO. We are working on a potential 18th consecutive positive quarter.

The portfolio is currently not live available to subscribers. I’m afraid that would encourage too much copy-paste trading, exposing you too directly to my mistakes.

Subscribers have done well doing their own analysis of my write-ups though, which actually have performed better so far this year, up 19% on average since pitch.

One new write-up will be out soon on a company which is currently in the portfolio. I have been geek-ing out on it a bit too much and should probably focus on making it a simple and crisp write up rather than a “look at all the work I did on this idea” show.

April 2026 market events

In the last month, the USA and Iran signed a peace treaty. This opens some perspectives for a re-opening of the Strait of Hormuz, although there are still several hurdles to be cleared before that happens.

Meanwhile, markets are making new all time highs. The companies in the S&P500 which have reported Q1 results so far, on average achieved 21% earnings growth, the highest quarterly increase in the last 5 years.

Artificial Intelligence is already driving companies to report higher earnings, not because of what the AI is doing, but because

AI builders (Big tech) save on labor to allow increased AI capex spending

AI users (Banks, Telco’s, IT developers) keep headcount low in anticipation

We’re not in an employment recession though, because the AI build-out itself is funding additional GDP growth, driven by that capex.

This puts in perspective why the S&P500 is doing well, and why it would do even better if the Strait of Hormuz were to be re-opened. In that scenario, we would likely have:

Increased GDP growth because of AI capex

Increased productivity because of automation & low hiring due to AI fears

Disinflation driven by productivity and tariff effect roll off

Fed reducing interest rates

We are talking about markets here though, and so of course, the exact opposite could also happen, with Strait of Hormuz remaining closed, and other trade routes also getting affected, sending oil even higher and creating an inflationary recession much like we had in 2022.

I think Iran and the USA are both so much better off making a deal, that they likely will make one relatively soon.

Changes and Portfolio

In this section:

Full portfolio with % allocation and change vs last month

All portfolio moves and their rationale