November portfolio update

Overview of October changes & their rationale

In this monthly update, we will

Update you on the current portfolio

Share the latest changes and rationale for each

Give the Top 3 stock in the portfolio we like most today

This is not meant to be an analysis but rather a quick info sharing.

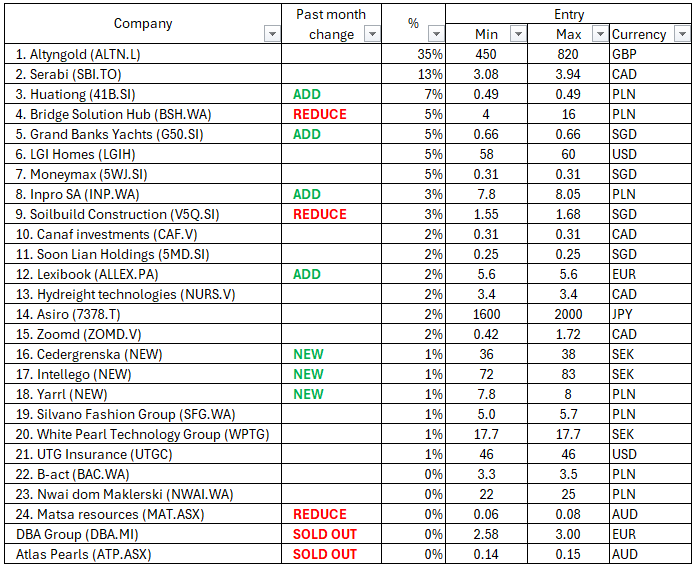

Portfolio:

The portfolio was up just over 3% in October, mainly driven by Altyngold closing Oct at 930 vs closing Sep at 840. (The % weights reported in the last update were those of ~ Oct 1st 09:30, at which point Altyn was already up 10% for the day. This meant that the reported weight was 35%, while it was only 32% at Oct 1st 00.00 am. So we now make sure to take the snapshot at 00.00 am to avoid confusion)

Also, in the previous update some 0.4% positions were shown as 1% positions. We now just show them as 0% to keep it simple. To make things more clear, we highlighted the changes above.

Changes:

Added to Huationg

A very cheap growing Singaporean builder.

The write up on this company can be found here:Reduced a little bit of BSH, to add to Inpro

BSH and Inpro are both small growing Polish companies trading at ~6x P/E with great prospects. We wanted to give Inpro a slightly bigger weight and reduced some BSH. We think BSH looks great but we own a lot of it compared to its liquidity, so we can allow taking some out to put into Inpro. Maybe we will do more of this, but we don’t imagine selling it below 20 PLN for the moment.Added to Grand Banks Yachts

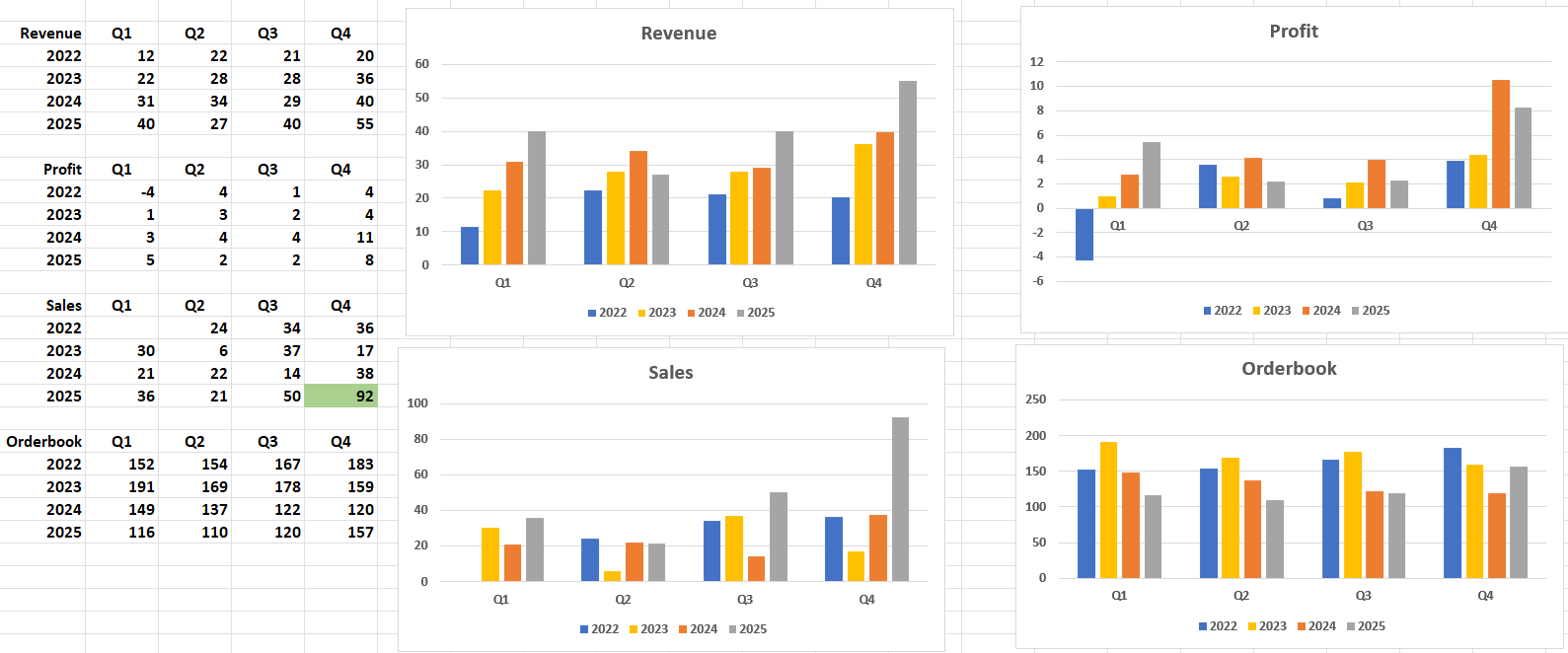

The company delivered a great Q4, and the comments in their Annual meeting suggest a very strong 25/26 fiscal year. The sales strategy with more US local presence seems to be working very well, leading to record sales bookings. They did not report sales bookings, but we could of course calculate it as { end Q4 orderbook) - (end Q4 orderbook) - Revenue}. What appears then is record sales bookings of S$92m, almost twice as high as sales in any other quarter in the companies history. TTM net income is 18 vs market cap minus cash of ~$105m today. The cash position is a bit debatable because some customers pay up front, but then also some boats are already partially completed and the revenue is not booked yet so that is not a visible asset… Potential philosophical discussion there but anyway we look at it, the company continues to grow double digits and trades at 6-7x market cap ex cash. Below is how we like to look a these companies. Note that with Grand banks, the market buys/sells the stock based on net earnings, but the true leading indicator is sales bookings. This would become a top 3 position if they get another quarter of sales bookings > S$60m. Worth mentioning much of the latest sales bookings are likely maintenance bookings which have lower margins, so the improvement in new sales is not as large as it looks. Anyway great progress specially compared to other yacht builders like Catana for example.

Bought some more Lexibook

Very cheap French toy manufacturer (~ 40m mkt cap, 7m TTM net income) with ~5 years of growth behind it. They make things like a 100 Euro “laptop” for your 7 year old, which runs some safe games and educational exercises.

Their continued geographical expansion across Europe and the USA, combined with lower container freight rates, should drive additional growth in revenues and margins.

Bought Cedergrenska

We think this is mostly a very well run company which will do well over the long term, improving every day and navigating the changing regulatory landscape in Sweden, a country that thrives thanks to its great education.

Bought Intellego

We don’t really think they would do buybacks and CEO purchases if the company was fake. We like their dosimeters and can understand why Henkel likes them too. This is too risky for a bigger position though, and too crowded as well.Bought Yarrl

Yarrl is a growing Polish IT company. We like their execution, we like that headcount on Linkedin is up 30% year over year. We like that together with Euvic, they recently signed a ~200m PLN frame agreement with the Polish ministry of finance (vs 55m market cap). We don’t strongly like/dislike their acquisition plans or intentions. Good for a starter position.

Reduced Matsa

We reduced this to invest in Huationg and Grand Banks and reduce gold exposure. We like Matsa from a balance sheet point of view, but their press releases seem quite promotional, and they have 100 different upcoming ideas which they can burn cash on, and then they also raised cash which seemed unnecessary. They will likely continue do well, but We wanted to free up some cash and reduce gold exposure, and this was certainly our least favorite gold stock.Sold DBA because their organic growth was a bit too low in our opinion. They will do well long term though. One thing with DBA is they amortize 1-2m in goodwill every year, which the market seems to never give them credit for. They end up spending this on small acquisitions which helps them grow faster. They then also amortize the goodwill on the new acquisitions, creating a bit of an extra hidden engine for returns… We don’t think this will get “unhidden” so there’s some lack of a catalyst here, but long term we think it will contribute to 10%+ annual returns for DBA. Looking at that setup, we preferred to sell it and allocate to the Singaporean companies and to Cedergrenska.

Sold Atlas Pearls.

The latest pearl auction in Kobe was pretty bad in terms of quality Atlas could bring, as well as price per quality point paid by the market. It’s still very cheap at 4-5x forward earnings, but its not as ridiculous as before.

Top 3 stocks today

Altyngold/ Serabi

Huationg

Grand banks yachts or Lexibook

(or the builders LGIH and Inpro but those are much longer term and maybe with a bit less conviction as we don’t usually invest based on balance sheet)

We hope you enjoyed this update, and really hope that before buying/selling any stocks, you do your own work on them and discuss the actions with your advisor. The goal of course is to share the journey, thought process and potential ideas, rather than to provide a copy paste portfolio. It’s probably helpful still to share monthly updates so everyone can use recent information to follow the story and consider new ideas. Let us know if you have any questions/feedback! Next write-up will likely be about one of the two housing stocks mentioned above.

Disclaimer

This publication’s authors are not licensed investment professionals. Nothing produced by the Floebertus team should be construed as investment advice. Investing involves serious risks, including risk of capital, as well as health risks. Do your own research before investing, and size your positions appropriately, in line with your own conviction and your own knowledge.

If Hydreight delivers on its monthly sales targets by December at VSDHOne, the stock should be a five or six-bagger very quickly. Why is its position so small?

Great update thank you