Cycling higher

Original OKP Pitch 03/03/2025 (0.49 SGD)

Summary

OKP Holdings is a growing Singaporean infrastructure construction company, with a strong track record in public sector projects such as road construction, airport works, and drainage improvements.

The company has just reported 180m in 2024 revenue, and 33m in 2024 earnings, delivering 18% growth for H2 2024, consistent with the past 5-year double digit growth. We think this growth is likely to continue to accelerate in the coming years, as OKP has a backlog of 600m SGD, up 16% vs last year.

The stock is very cheap at 4.6x earnings, or 1.5x earnings after backing out the cash and the liabilities. There’s no catch in the earnings quality, in fact they had some small write-offs and currency translation headwinds, which in our opinion make the underlying earnings even better than they look.

In the pitch, we will describe the background of the company, their overall success story, their struggles in 2017-2023, their strong performance coming out of that challenging period, the nice prospects of the business, the current valuation and the risks.

What does the company do?

OKP Holdings, named after founder Or Kim Peow, was started in 1966, currently has 800 employees and is engaged in 3 main activities

Construction & Civil Engineering (63% of FY24 revenue)

OKP provides civil engineering and infrastructure construction works, with a focus on public sector projects in Singapore. This includes the construction of expressways, bridges, flyovers, taxiways, airport runways, drainage systems, and commuter infrastructure.Maintenance & Minor Works (34% of FY24 revenue)

OKP provides long-term maintenance services for those same infrastructure elements.Property Investment (3% of FY24 revenue)

OKP owns a portfolio of investment properties in Singapore and Australia on which it generates rental income. This is just a way to keep funds available for the business in case large tenders are won, while also catching some yield.

Or Kim Peow founded the company in 1966 and transferred his role as managing director to his son Or Toh Wat in 2002. The company has grown over the years to become one of Singapore’s recognized infrastructure contractors for both public and private sector projects serving private sector companies like example Exxon Mobile, but more importantly a broad range of public sector companies in Singapore, for example:

- Land Transport Authority (LTA) – Roadworks, cycling paths.

- Public Utilities Board (PUB) – Drainage improvement projects.

- Changi Airport Group (CAG) – Airport runway and taxiway works.

- Housing & Development Board (HDB) – Residential infrastructure

- National Parks Board (NParks) – Landscaping infrastructure.

Public sector work is currently the bulk of their revenues, and the difference between “construction” and “maintenance” in this line of work is relatively thin, so for our analysis we will look at the business mainly as (1) Cycling path construction and (2) Other construction and maintenance.

The Pan-Island Expressway viaduct collapse disaster

In 2017, the company faced a major accident when an expressway they were building collapsed, causing the death of 1 worker (Mr. Zhou Tian) and injuries of 10 others.

In 2019, after lengthy investigations and trials, OKP was fined 1m SGD for workplace safety violations related to this accident. OKP employees were found to have made several mistakes in handling the initial warning signs before the collapse of the bridge.

In 2023 however, OKP won a trial against their design company of the viaduct, “CPG Consultants”, arguing that the bridge was not designed properly and that although OKP could have handled the initial cracks of the bridge better, they followed the advice of the engineering company. CPG was found at fault and paid 44m in damages to OKP in 2023, restoring OKPs reputation and balance sheet.

Since the accident, OKP has updated its safety procedures, to improve design review, training and site inspection, and has talked about this in every annual report and in every investor meeting. OKP was able to continue their business by focusing on relatively small road construction and landscaping projects (20-200 mSGD). Since the trial outcome, OKP has restarted bidding on much larger LTA projects (300-800 mSGD). Although they have been successful in expanding their orderbook, none of the larger LTA projects has gone their way so far. More on this later.

Singapore

Singapore is a country of 6 million inhabitants, with a diversified economy that thrives thanks to an excellent education system, pro-business government and great infrastructure.

The country has a 35% trade surplus, 4% real GDP growth, just under 2% inflation, a balanced fiscal budget, and friendly relationships with China, India, Europe, the US and Japan. One SGD is about 0.75 USD. This currency pair has kept a relatively narrow range since 2010. (+/- 10%)

The economic success of Singapore enables its public infrastructure investments, which are projected to reach about 50 billion SGD in 2025, up ~1% real CAGR for the past 5y.

OKPs Market focus and competition

Within the large ocean of Singapore’s public investments, OKP is focusing mainly on cycling paths and drainage networks, 2 lines of business in which they have been a consistent partner for Singapore’s LTA (Land Transport Authority) and PUB (Public Utilities Board) for the past years.

Cycling networks

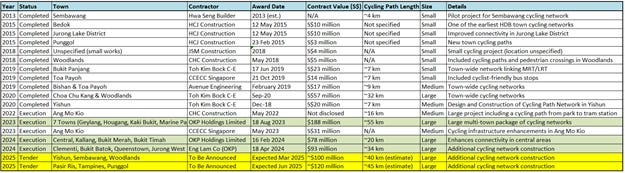

In 2020, the Singaporean government announced intra-town cycling paths as a key priority in Singapore’s mobility master plan. The government wants to invest in cycling networks, to provide a healthy and green way for Singaporeans to transport themselves, while relieving the busy roads on the 30 x 17 mile island. Specifically, the LTA communicated their intention to expand the existing 460 km cycling path infrastructure to 1300 km by 2030.

To accomplish, several new tenders were launched:

Some observations from this overview of cycling infrastructure tenders:

Since the 2020 announcement, the size of the tenders has increased significantly

OKP won 3/4 of the large tenders (incl. subsidiary Eng Lam co)

Average unit price is 2-3 mSGD per km

Of the total expansion of 840 km by 2030, so far 164 km was awarded (676 km to go)

This means that, only in bike lane construction, OKP Holdings is set up well to win a significant part of the upcoming 1.3-2.0 billion SGD in new tenders. In their 2023 FY Q&A, CEO Or Toh Wat explained why OKP is a preferred supplier in these tenders:

“Although cycling path projects may not be technically challenging, they nevertheless require good local ground knowledge and expertise. There are usually few bidders as the skillsets required are different. OKP has the requisite expertise and experience to carry out such projects. The Group may be awarded the contract even though it has not submitted the lowest bid. The Group is in a good position to execute such projects as it has the necessary experience and resources to minimise inconvenience to the public and to deal with the public.”

You may be thinking, how can a cycling path be so expensive or require a skill set? Well these are typically sheltered, to accommodate for the hot and rainy Singaporean climate, or they include large bridges across the well-developed road infrastructure in the country. Also, cycling path improvement or installation requires a multi-phased approach with a lot of interaction with several different levels of government to close and upgrade existing roads. (boring is beautiful, ay?)

Other construction and maintenance work

After the favorable lawsuit outcome in H2 2023, and with the recognition OKP received for improving safety standards in the past years, OKP has restarted bidding on larger construction projects again. So far, their main win was a 96 mSGD roadside maintenance contract, but they have also bid on much larger 300-800 mSGD projects, so far without success.

CEO Or Toh Wat explained how this is linked to the large cash position OKP has:

“It would not be wise for the Group to stop tendering for projects once its order book reaches a certain amount. The Group is tendering for a project that is close to $500 million. It will need to have sufficient buffer cash to execute such projects.”

Competition

For cycling networks, OKP has taken a clear leading position in Singapore. Other large contractors may come in and try to take a part of the pie as it grows, but we think we can expect OKP to continue to win a significant part of this work. We were looking at Toh Kim Bock as a key competitor having done similar work in the past, but they have not bid on the latest large tender. The only competitors in the bid are large generic construction companies, which as Or Toh Wat mentioned have less expertise and appetite to go into the complexities of bike traffic planning.

For road works, the company has many large and small competitors in Singapore’s fragmented construction market. The unpredictability in construction leads market participants to calculate some risk buffer into the price, which typically turns into profit if projects go well. This explains why net margins are at 10-15%, higher than usual in a fragmented market.

Valuation

OKP has net cash of just over 100m and just closed the year with 33m in profits. Cleaning up the income statement, we would argue their earnings power in 2024 was more like 35m, after removing a revaluation of Australian real estate assets, and similar accounting adjustments.

Anyway, these one-off headwinds of about ~2.5m were offset by interest income of ~2.5m, so we can take the 33m earnings power as representative for the business in 2024.

Margins are on the high side, but the continued cycling network wins suggest this will continue at least for a few years, as the CEO confirmed in the most recent Q&A.

We think OKP is worth ~15-20x earnings given their consistent double digit growth, large order book (> 3x sales), clean balance sheet, and prime position to win a significant part of the upcoming 2 billion in cycling path construction until 2030.

After adding the 100m net cash, this leads to a valuation of 1.9 SGD – 2.5 SGD per share, which leaves significant upside from the current 0.49 SGD per share.

Share register and cap allocation

OKP is primarily owned by the OKP family holding 55% of the shares, a Chinese institutional investor “China Sonangol” holding 14%, and 31% free float. The latest change in key holdings was a buy-back of 0.5% of the shares during covid in which insiders did not sell their shares to the company. OKP will pay a total dividend of 2.5 ct in 2025, or 5% dividend yield. The rest of the free cash flow will be used to expand the business and continue to bid on large projects without capital constraints.

Risks

Recovery of the Chinese construction market could cause prices for labor and material might increase significantly which would have at least a short-term negative impact on margins

Competition for OKPs construction projects could increase leading to potentially lower margins. We think this is very unlikely in the short term, and very likely in the long term, to go closer to 10% net margin vs current 15%+ over 3-4 years.

If the 30-year success story of Singapore is interrupted, there would be a major setback in the cycling path part of the business, which we can safely consider “public discretionary spending”. Again here, We think the opposite is more likely to happen, with the continued prosperity of the island nation to lead to more infrastructure investments.

Disclosure

We have shares in OKP since mid-2024 and have made this our largest position after the latest earnings report. We didn’t write this post to do your due diligence, but rather to document ours and to share it with others that may point out gaps to improve our process and avoid mistakes.

OKP 2024 webcast and Q&A

From OKP’s investor relations website:

The Board of Directors of OKP Holdings Limited (the "Company") is pleased to announce that the webcast of the Company's presentation on the financial results for the financial year ended 31 December 2024 is now available. Investors can now access the webcast at https://okp.listedcompany.com/wpsg.html/t/vdo/e/4qfy2024.

In conjunction with the release of the financial results for the financial year ended 31 December 2024, the Company has set up an online question and answer forum with the Management of the Company (the "Online Management Q&A") today. The Management will take questions from investors from now till 4 March 2025 (Tuesday) and will reply on 11 March 2025 (Tuesday).

All investors are welcomed to participate in the Online Management Q&A. Investors can now post questions on the Question Submission Page at https://okp.listedcompany.com/qa.html.

Summary (March 3rd 2025)

OKP Holdings (SGX: 5CF) is a leading Singapore infrastructure contractor with a strong public sector focus and a dominant position in cycling path construction. After recovering from a 2017 project collapse and winning a key legal case in 2023, OKP is now delivering record earnings, with 2024 profits of SGD 33 million, 15%+ margins, and a record SGD 600 million order book. Despite its growth, clean balance sheet (SGD 101 million net cash), and 5% dividend yield, OKP trades at just 4.6x earnings — a deep discount to fair value of SGD 1.90 to 2.50 per share, offering significant upside from today’s SGD 0.49.

Disclosure: We still own OKP as our biggest position

Disclaimer

This publication’s authors are not licensed investment professionals. This is not investment advice. Do your own research.