OKP delivers 40% growth in H1 2025

Sales growth, operating leverage and order book growth at single digit pe

Dear subscriber,

OKP Holdings, our construction and cycling path winner in Singapore, reported H1 earnings this week.

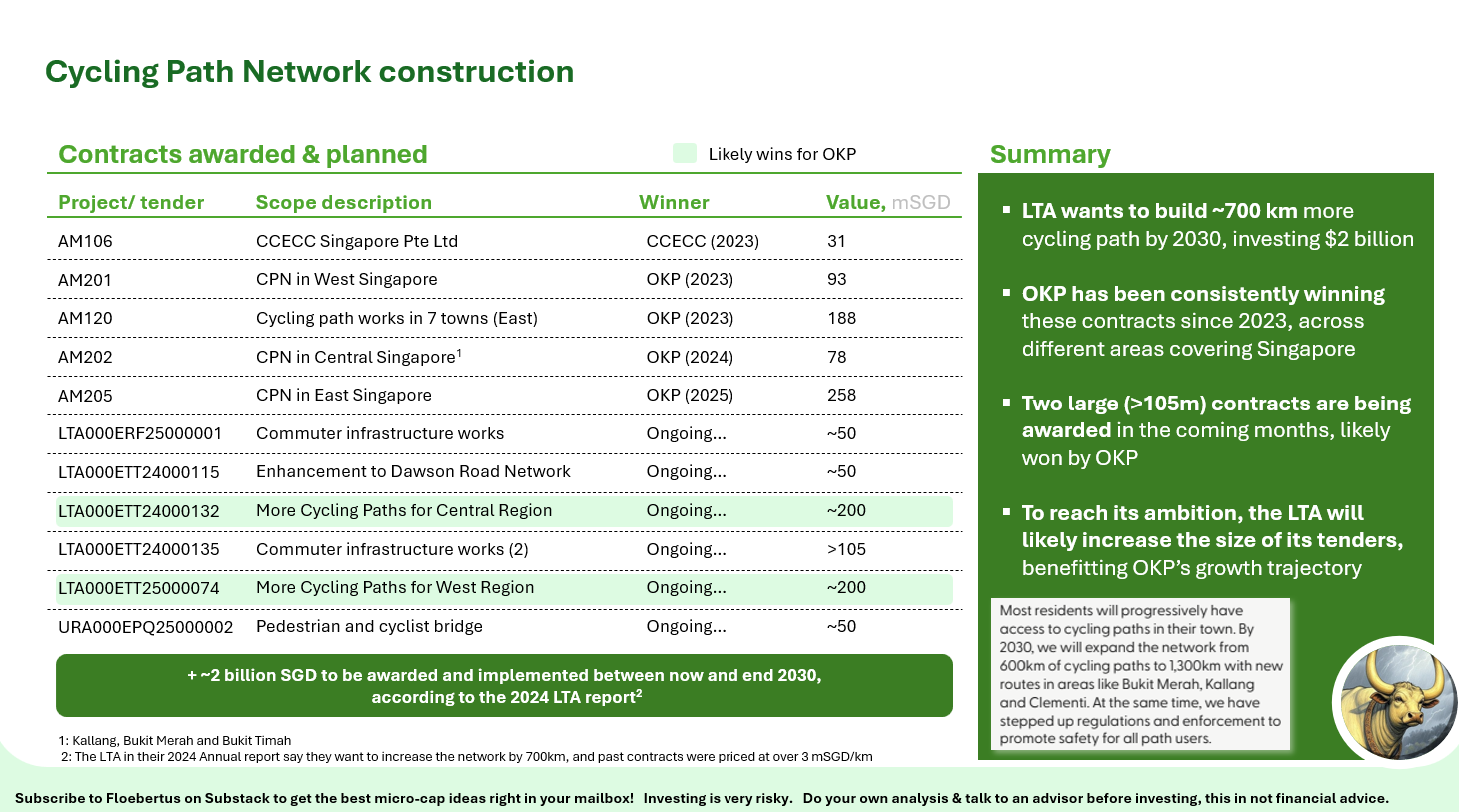

We saw excellent growth in sales and backlog, improved profitability and strong cash flow. At the same time, we saw the Singaporean Land & Transport Authority launch more cycling path tenders. OKP has now won 96% of the SGD dollar value of these contracts since 2023 and is the only Firm currently designing and installing cycling paths in Singapore.

This is an excellent position to be in, because as explained below, demand will grow to ~450 mSGD per year, which is over 3x OKP’s current annual construction segment revenue… and the additional projects will overlap an integrate with the ongoing projects OKP is implementing in the East, West and Central regions of Singapore.

Let’s jump in…

H1 earnings

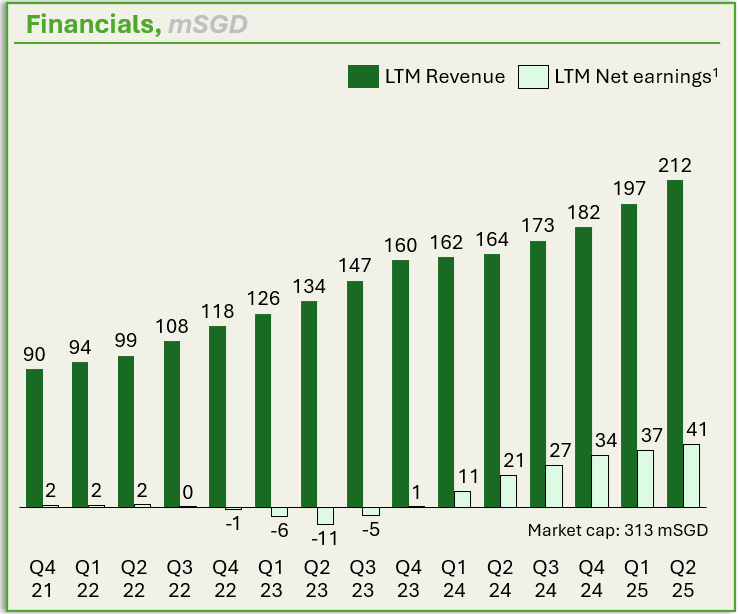

Revenue: 104.3m vs 73.9m (+41%)

Gross profit: 32.1m vs 20.8m (+54%)

Net profit: 19.1m vs 11.9m (+61%)

Management comments

“We are pleased to report a strong financial performance, boosted by higher revenue recognized for our various ongoing and newly awarded construction projects as they progressed to a more active phase in 1H2025. The Group is committed to the efficient and smooth delivery of our projects, underpinned by high standards in our work processes and embracing technology and innovation to sharpen our competitive edge.”

”… the Group remains focused in building a sustainable and resilient business to navigate challenges effectively. In May 2025, the Group announced the award of a S$258.3 million contract from the Land Transport Authority for the construction of new cycling paths for East Region in Singapore across 11 towns. This marks the largest contract win in the Group’s corporate history. As of 30 June 2025, the Group’s order book stood at S$648.3 million, with projects extending till 2031. The Group is actively pursuing civil engineering and infrastructure projects, especially public sector projects, in Singapore to strengthen its order book.”

Our thoughts

The thesis is playing out well here, with OKP delivering strong revenue growth, margins and backlog growth. The results were exactly as could be expected from the ongoing growth of the contract wins and the business. Longer term growth is looking great and the order book suggests it will continue in the coming years.

OKP shared order book of 648m as of June 2025. We expected order book to be at least 755m because:

Dec 31st order book was 601m (Annual report)

They won a 258m contract in May

They reported 104m in revenue for H1

There’s a few different possible reasons for this:

A contracts was canceled/ on hold/ completed at lower cost

Some work may be completed and out of the order book, but not yet recognized as revenue (not validated by the customer yet)

Contract values in Singapore are being adjusted in line with fluctuating material prices (most commodities dipped as SGD rose 8% vs USD in H1)

Full 258m award may not be included yet (may be contracted but not ordered)

Unfortunately this was not mentioned in the H1 report. We think it’s likely that the Land & Transport Authority retired the 2015 Walk2Ride contracts OKP had, and is now embedding them into new cycling path contracts. At the same time, the LTA can adjust contracts when currencies/commodity prices fluctuate, which may have led to a small adjustment in H1 as the Singaporean dollar was quite strong, rising 8% vs the US dollar commonly used in commodity trading and international labor contracts. We will likely get info on this soon as OKP is generally responsive to shareholders questions.

While the LTA awarded this huge 258m contract in H1, it is launching several new interesting tenders - which OKP is primed to win as we see below. Note that according to the 2023-2024 LTA report, they want to build 700 additional kilometers by 2030, and note that the recent contracts have been awarded at prices of

3.2 mSGD/km, to get a feel of how massive the pipeline of oncoming projects is …

OKP has won ~96% of the value of cycling path contracts in the past 2 years, making them the key partner for the LTA, and for the local authorities (traffic, road design, safety, … ) in the different regions and towns.

To implement its targeted network upgrade by 2030, the LTA will tender

~400-500 mSGD per year in the coming 4 years. This is 3x the current construction revenue of OKP, and will come on top of their existing construction and maintenance backlog, setting them up for several years of growth to come

OKP is meanwhile also bidding on larger (>500 mSGD) public construction projects. We think it’s very unlikely for OKP to win this type of projects, as the Singaporean government will not want to interfere with their own fast paced cycling and walking path roll out

We look forward to OKP continuing to win more contracts, while growing their organization to deliver the growth and reap the earnings implied in the past and hopefully future wins

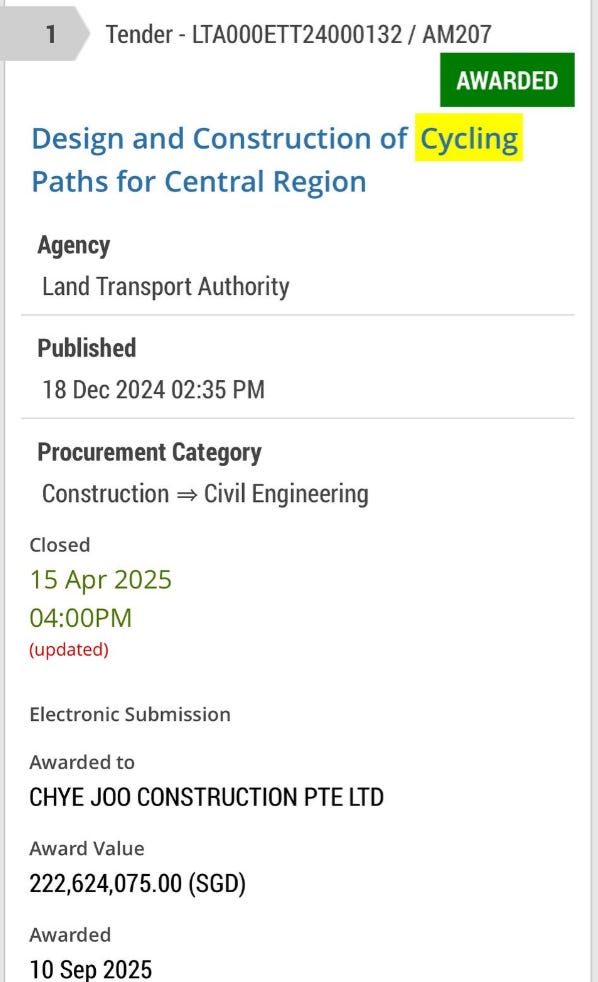

Update on Sep 17th:

Tender AM207 was awarded this week and OKP did not win it, moving their win ratio from 4/5 to 4/6.

We were right on the tender value but not on the winner, which we thought OKP had a 90% chance of winning. This changes the thesis, as they now have (1) lost the tender worth ~1 year of revenue and (2) Have an active Singaporean local competitor for the remaining tenders, which is undercutting their price by 15%, pressuring margins and (3) have their stock up ~130% from the initial write up.

In the next portfolio update, we will therefore have reduced or exited our OKP position.

Lost tenders do not get communicated, so this is not “news” to the market but it can change the long term perspective of the company. The stock is still doing well for the moment, OKP stock being up 5% so far this month.

Anyone looking to reduce or add to their position should therefore consider the balance of positive and negative elements around the stock when deciding their actions. The company has made a lot of progress and growth in the past years, and will likely continue to do well.

Disclaimer

This publication’s authors are not licensed investment professionals. Nothing produced by the Floebertus team should be construed as investment advice. Do your own research.