Poland's most interesting stocks

Update for Q3 earnings

Poland is a great place for hunting micro-caps. Today, we will not go in large depth on individual companies, but we will overlook this hunting ground for potential multi-bagger candidates, taking 5 steps:

Narrow down for what we are looking for quantitatively

Remove several groups of stocks for Qualitative reasons

Add back amazing growth stocks even if P/E or ROE doesn’t fit yet

Show the 16 most interesting Polish stocks for the moment

Review the most interesting 10 in a preliminary 1 page pitch

Poland is a great place for investing, because it has an amazing economy, a low cost of being public (resulting in a high amount of companies) and valuations are low as international investors are only just finding their way to the country.

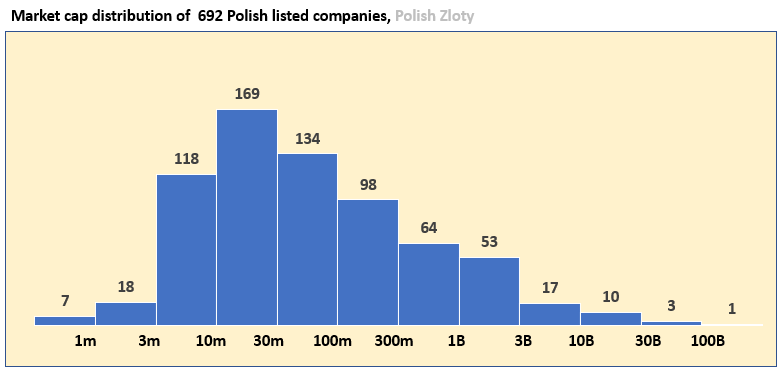

There’s over 700 listed companies in Poland. We include 692 in our population, having removed some “blacklisted” companies like CDA and Gamivo.

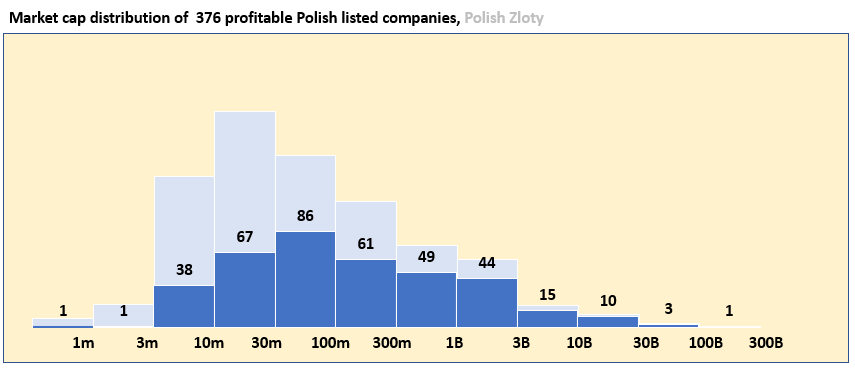

We are going to be a bit greedy because that just works well in this market. In the sense that we want an amazing growth stock at an unreasonably low valuation. Start by removing unprofitable companies.

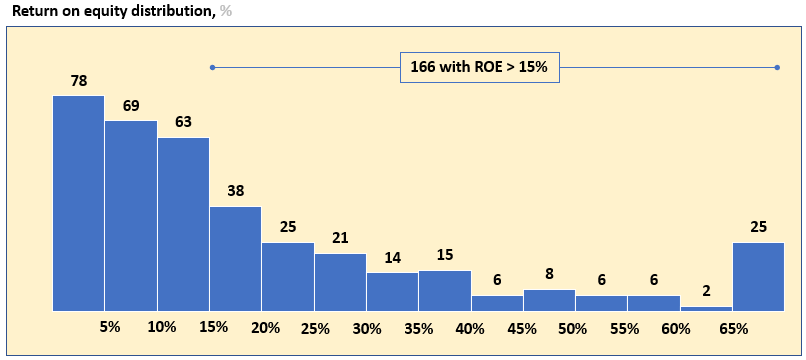

That light blue part above. That’s like the Polish Russel 2000. Not saying it’s garbage… Not saying it’s not… To further side step low quality companies, we only include those with ROE > 15%, showing some quality.

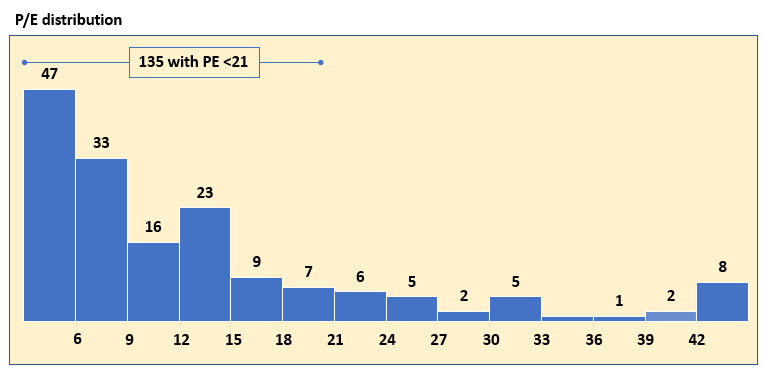

We didn’t come all the way to Poland to pay for these high quality companies though, so we include only stocks with P/E < 21

As we will see soon, many of these cheap high quality companies will be small and micro caps. Not many people are looking at them, and that’s our opportunity. The best scenario occurs when they are also growing fast. So they are already undervalued, but their growth makes them visible to more consumers and investors. We then get paid for the earnings yield, the growth, and the increased visibility showing up in multiple expansion.

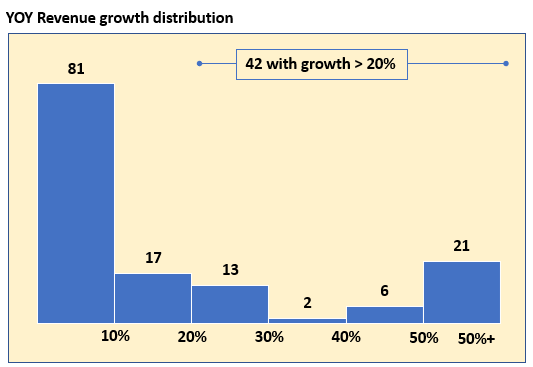

We are left with 42 companies that screen well. You know what’s the problem with companies that screen well? Most are still terrible businesses. This is why we exclude most of them, because they are too unpredictable (gaming, solar, energy retail, … ), too cyclical (steel, coal, paper, …) or too hard (biotech).

Finally, we add back some companies that may not have great P/E or ROE yet, but are showing such nice growth that they are hard to ignore. Today those were Inpro, Marvipol, Vindexus, Helio, Yarrl and Torpol.

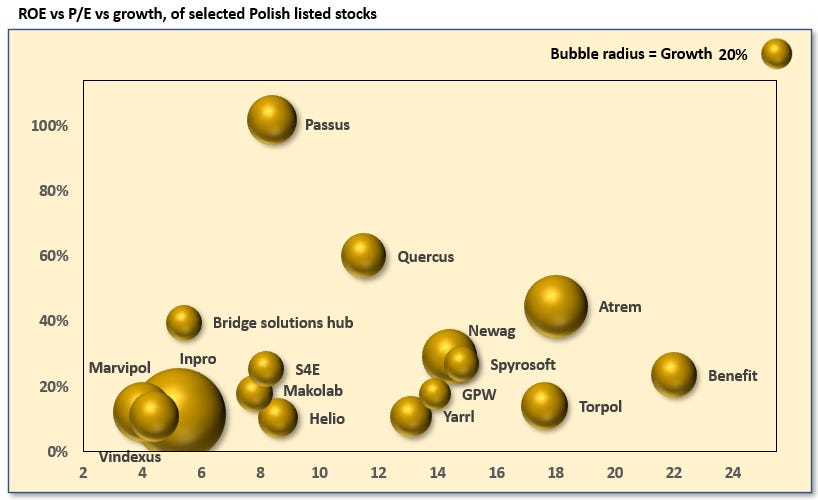

We end up with 16 wonderful companies at wonderful prices.

Below are our 10 favorites from reading the Q3 reports, in no particular order.

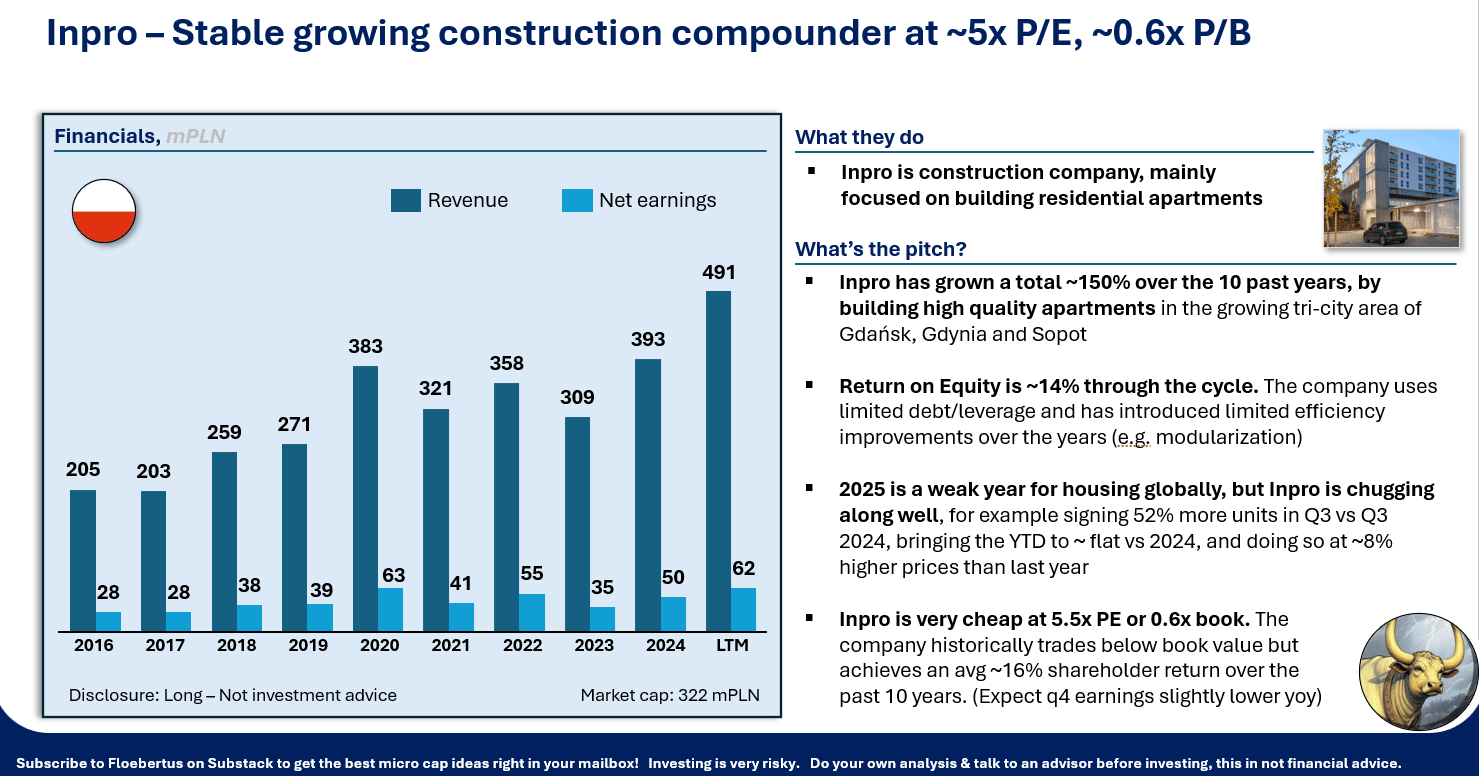

First is Inpro, a growing residential construction company at a very low price.

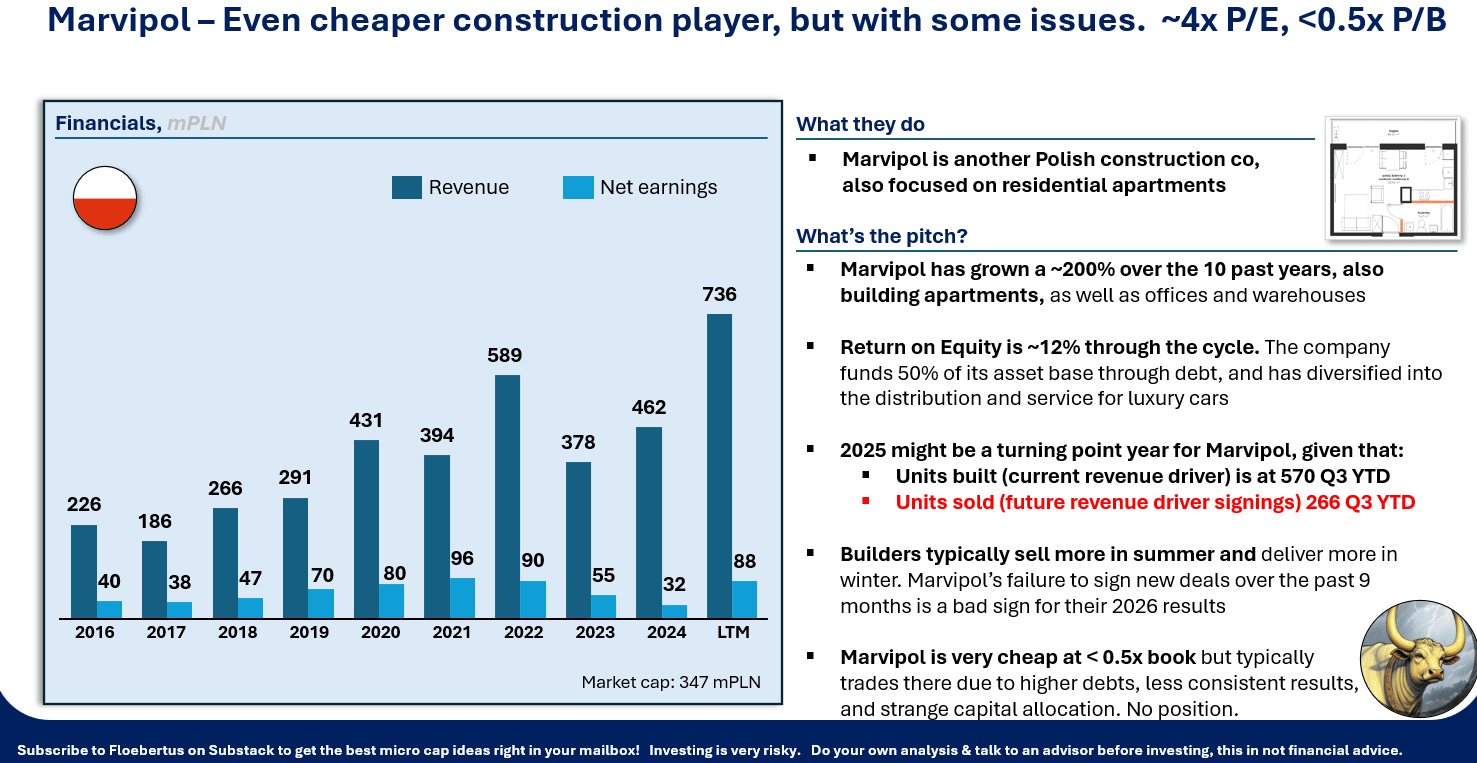

Marvipol is a very similar company, even cheaper but doing significantly less well in terms of signing new sales for next year. We think next year they will come behind Inpro in sales and profits.

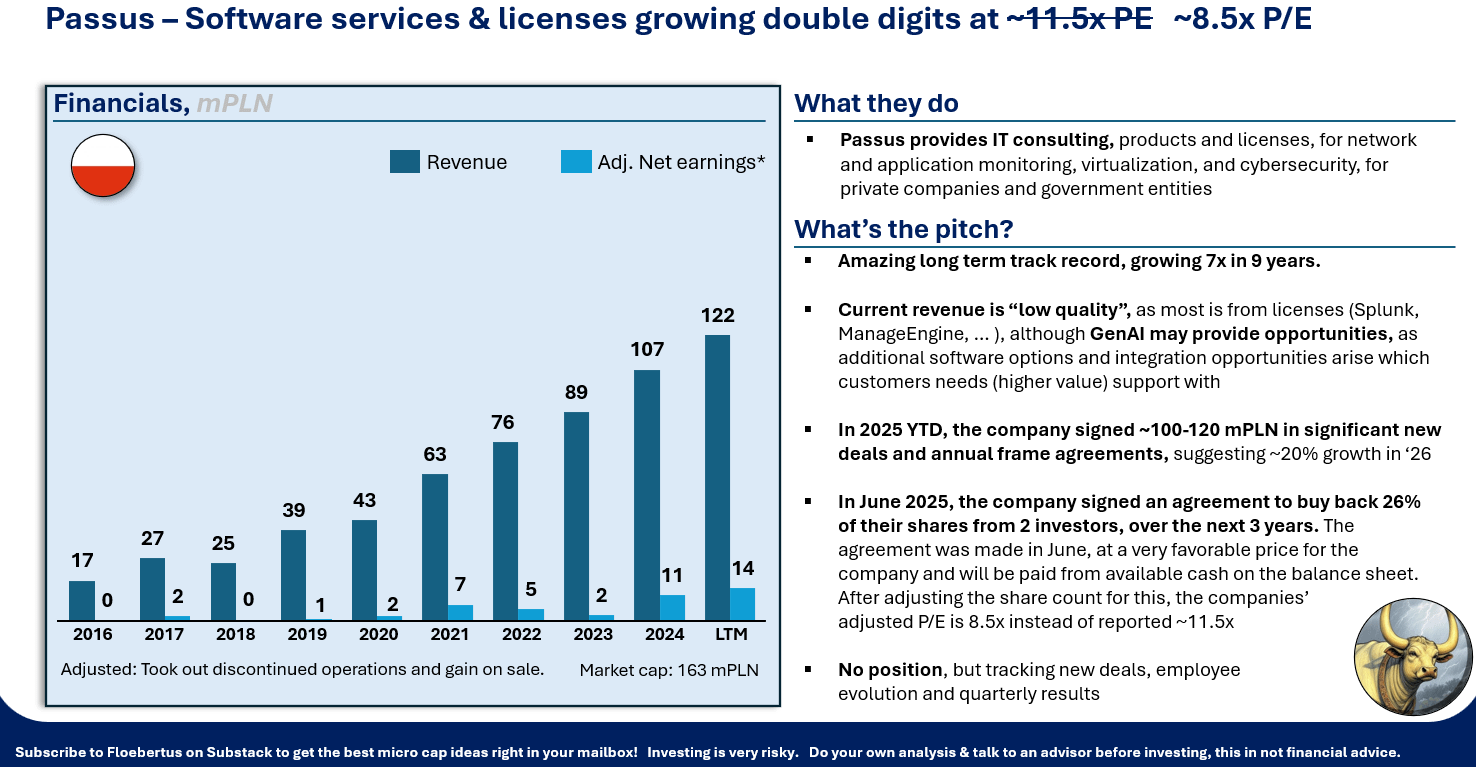

Next we have Passus. The company signed a contract to buy 26% of its shares in the coming 2 years, buying from early family office investors. Since locking in the price in June, the stock is up over 60%. Taking into account the buyback, the stock trades at ~8.5x implied market cap.

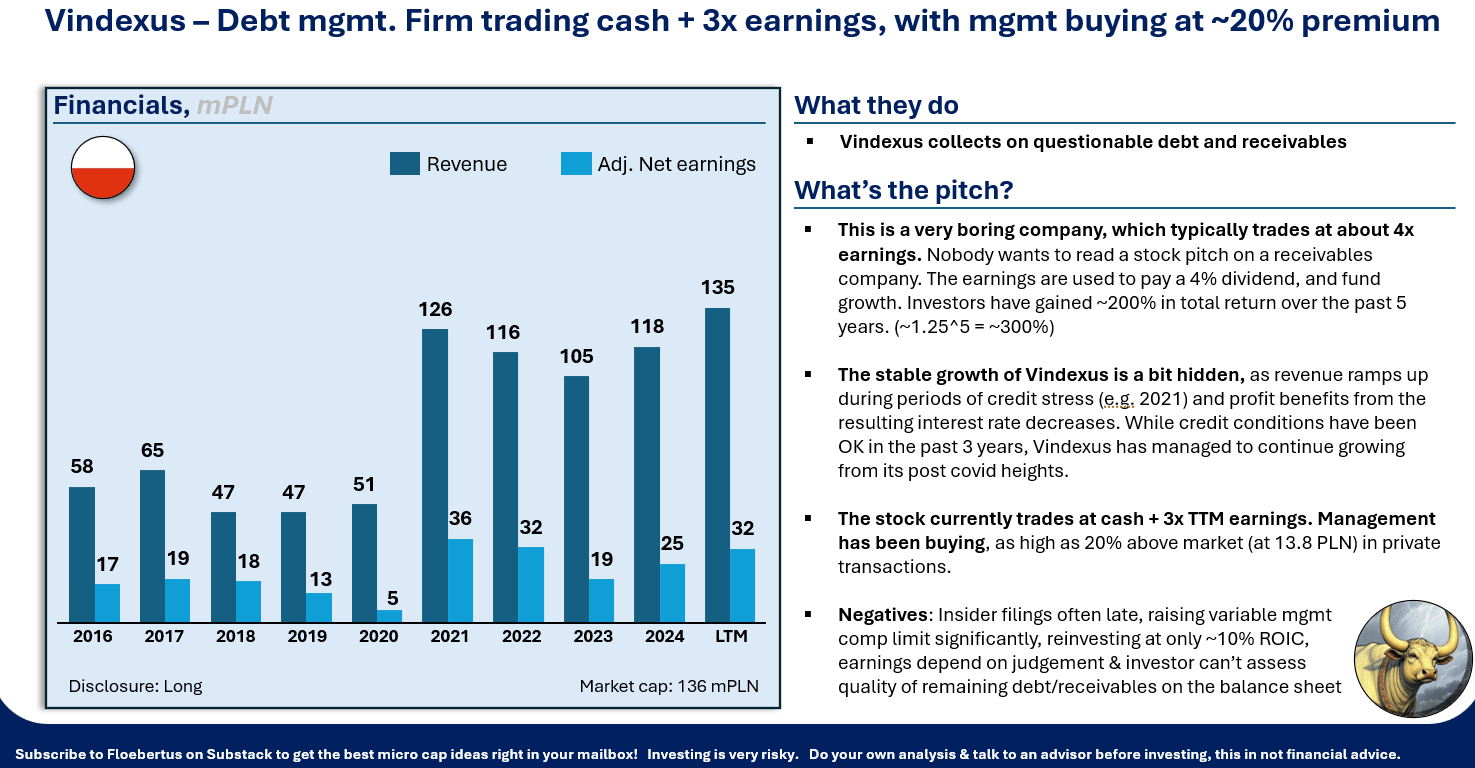

Vindexus is one of the cheapest companies in Poland today, at cash +3x earnings. Insiders are doing block trades at a 20% premium…

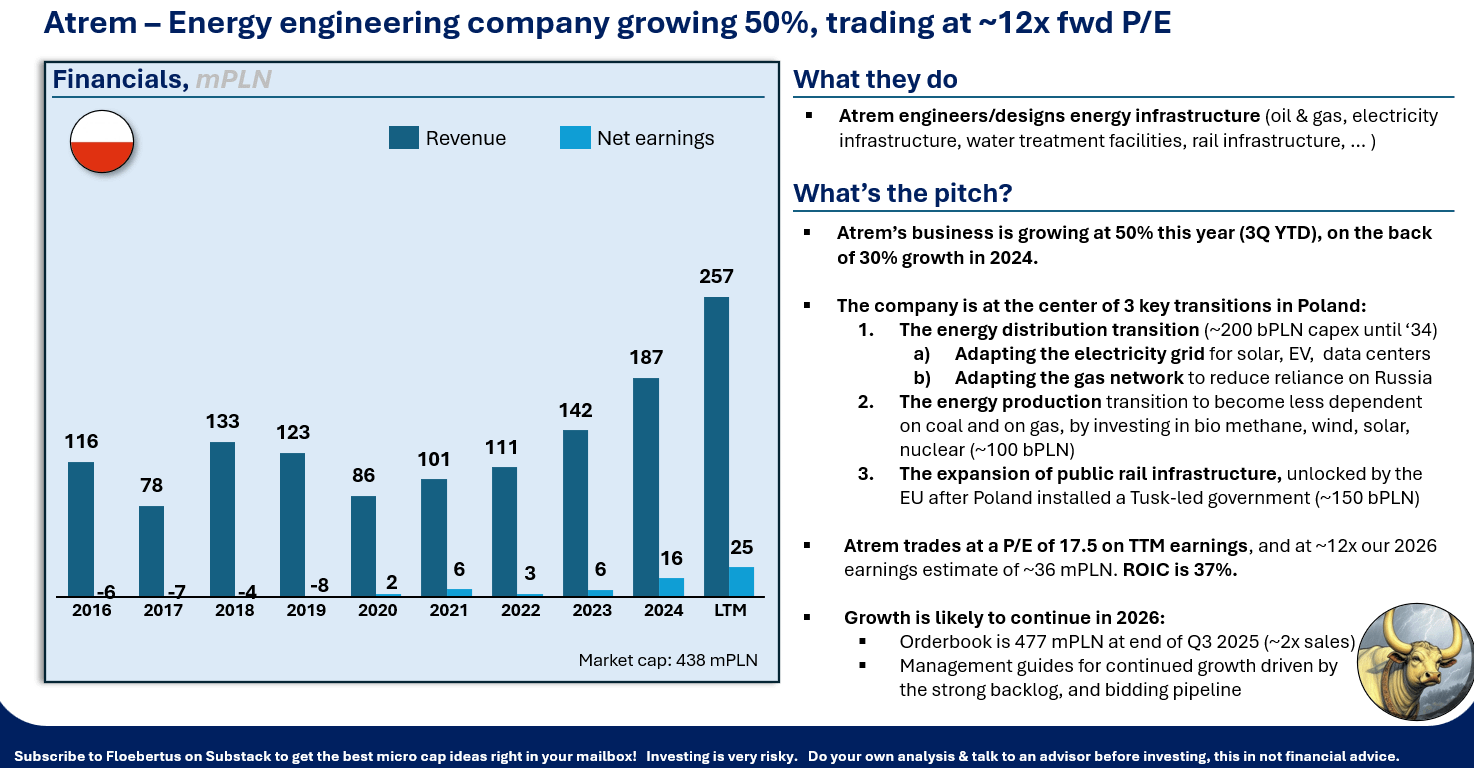

Atrem is a high quality grower playing into several growth trends

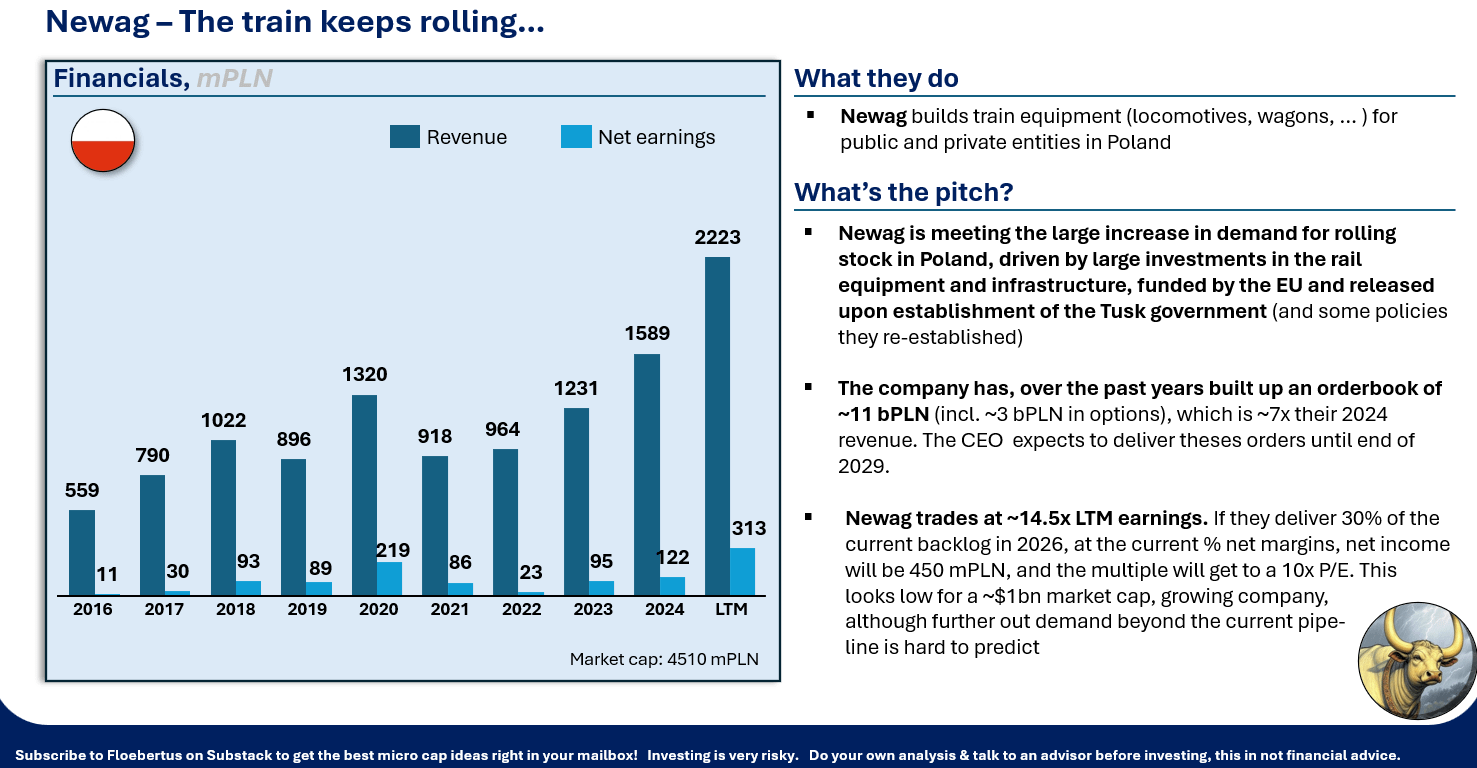

Newag is a train builder with revenue visibility for the next 5-6 years.

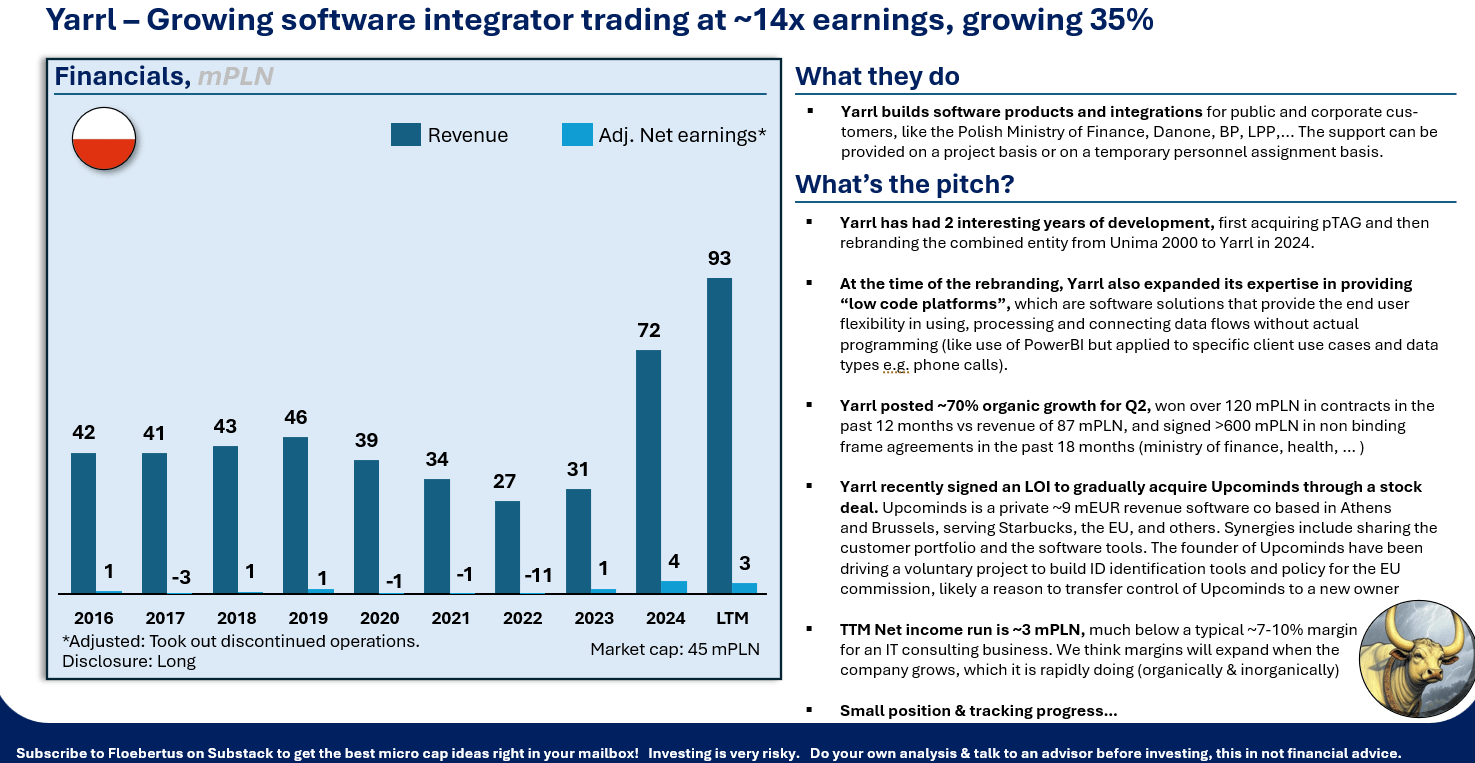

Yarrl is a Polish software co. This could be the next Spyrosoft, a company we found in 2022 growing 50% trading at 12x earnings. Yarrl needs to work on margin expansion though. It will happen but might take some quarters/years

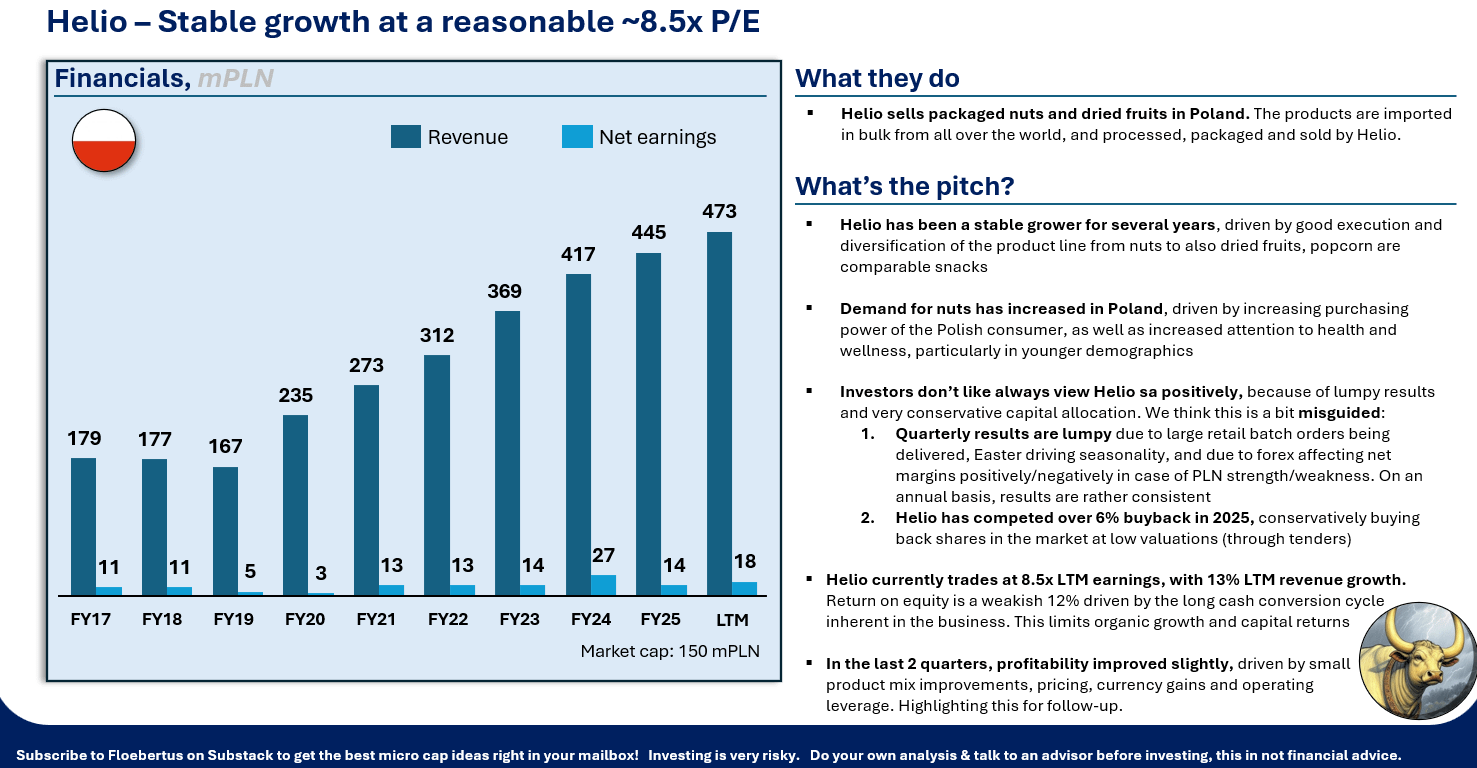

Helio is one of the two growing Polish packaged nuts and dried fruits companies. This one initially didn’t make the ROE cut, but delivers growth so consistently that we included it. It reminds us a bit of Tarczyński, another Polish consumer brand which quickly doubled a few years ago after catching some operating leverage, resulting into higher net income, driving P/E down and ROE up.

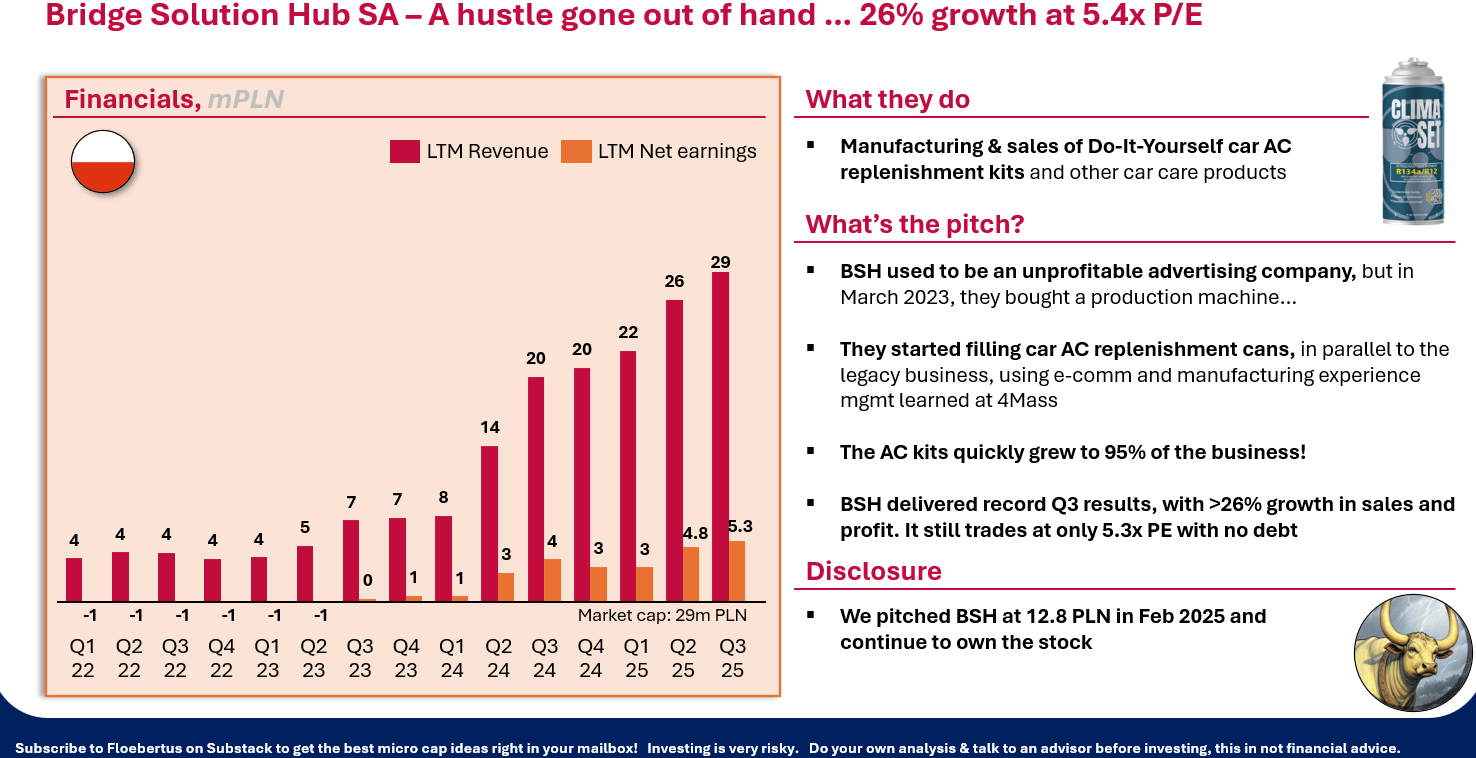

Bridge Solutions Hub is next up. The company keeps executing and growing.

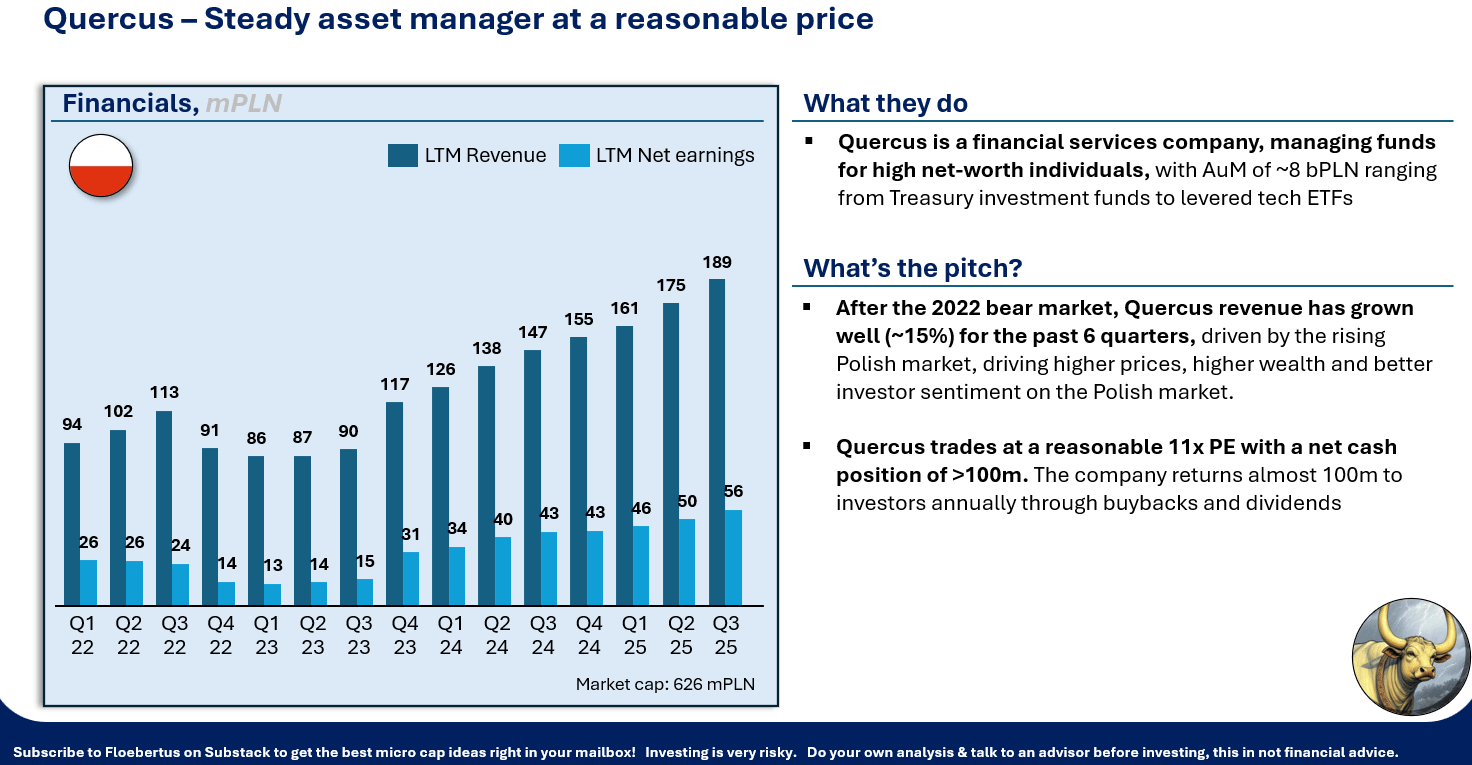

Finally we have Quercus. The current P/E of this funds manager is probably too low, although time will tell how much the E goes down in a bear market.

We like to study Polish companies and we like your thoughts on them as well. Let us know which one you like.

Disclosure: We own BSH, Inpro, Vindexus and Yarrl, as well as other under the radar names in Poland that didn’t make the list for Q3.

We like all of the above companies and will do some more work on them (employee evolution, cash flow conversion, business moat, employee reviews, e-commerce stats, … ) before likely buying a new position in one of them, or increasing an existing position.

Disclaimer: This is not investment advice. Before investing, validate the data within the companies audited reports, and speak to an advisor.

Thank you

Would you mind sharing what software or platform do you use for the screening?