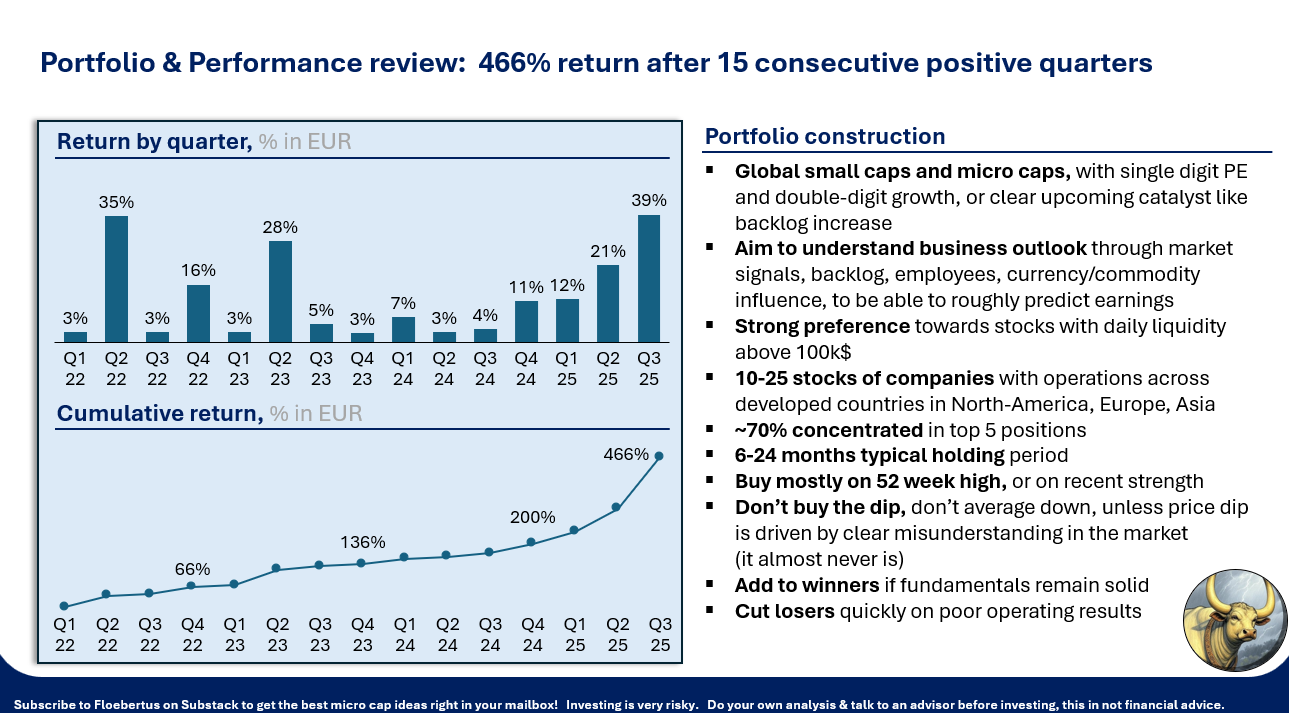

Portfolio & Performance review (Q3)

+89% YTD and ~5.5x since 2022

In this first quarterly update, we will:

Update you on the performance since Jan 1st, 2022

Review the performance of the 2025 write-ups

Share the current positions and % allocation for each stock in the portfolio

Describe the main Q3 changes and rationale + lessons from mistakes/winners

Close with a quick summary of why we own each stock in the portfolio

In late 2021, we started really digging into small and micro-caps. We would find small companies like Spyrosoft which no-one had ever heard about, trading at 12x earnings with 50% growth. We realized there were stocks nobody noticed and nobody cared about. You only had to search hard enough to find them, and understand them well enough to build conviction.

Since then, we look for single-digit P/E stocks with years of growth ahead, slowly getting recognized by the market. We look at stocks globally. We analyze hiring trends, vacancies, product reviews, commodities involved, macro influence, competitors, currency effects, market perception … and pick the best stocks. As the portfolio grows, we include mainly stocks with daily volume > 100 kUSD, so sufficient capital can be deployed and friction is limited.

Performance update

The returns so far have been excellent:

The 4 pitches written in 2025 are up 79% on average, in 4 months on average, with a 100% hit rate. Below is an overview of the companies written up, and their stock performance since each write-up.

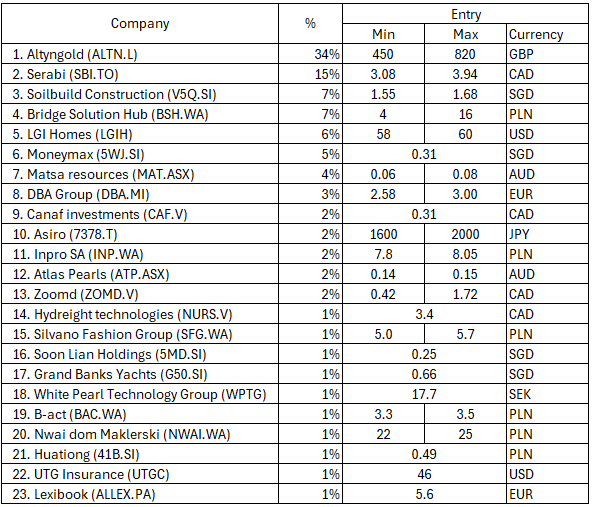

There are 23 positions today (01/10/2025), with operations across 14 countries:

Altyngold (ALTN.L)

Serabi (SBI.TO)

Soilbuild Construction (V5Q.SI)

Bridge Solutions Hub (BSH.WA)

LGI Homes (LGIH)

Moneymax (5WJ.SI)

Matsa Resources (MAT.ASX)

DBA Group (DBA.MI)

Canaf Investments (CAF.V)

Asiro (7378.T)

Inpro SA (INP.WA)

Atlas Pearls (ATP.ASX)

Zoomd (ZOMD.V)

Hydreight Technologies (NURS.V)

Silvano Fashion Group (SFG.WA)

Soon Lian Holdings (5MD.SI)

Grand Banks Yachts (G50.SI)

White Pearl Technology Group (WPTG)

B-Act (BAC.WA)

NWAI Dom Maklerski (NWAI.WA)

Huationg (41B.SI)

UTG Insurance (UTGC)

Lexibook (ALLEX.PA)

Changes

Largest change since Sep. 1st:

Sold OKP after the company lost a cycling path tender against a local competitor underbidding them by ~15%. The tender outcome meant a significant adjustment to our growth and margins expectations for OKP. It basically moved from a high margin, high growth niche company to a commodity provider in our view, leading us to exit the position. No one is looking at these tenders and Singaporean construction likely continues to do well, driven by large investments like the new Terminal in Changi Airport, so OKP will likely continue to do well, but we’re out of the position.

Adding to the existing Altyngold and Serabi positions. While their stock prices went up, the stocks also became cheaper as gold rallied and the mining operations performed well. (see below)

Buying LGIH and Inpro, 2 housing stocks that trade at 65% of book value

Selling the remaining NTG Clarity because of foreseen lower Q3 earnings driven by weakening of USD vs Egyptian pound and higher tax expense

Adding a little bit to Asiro after the large drop on weaker earnings

Buying several small positions we’re still reading about (Soon Lian, Grand Banks Yachts, White Pearl Technology Group, B-Act, Huationg, UTG, Lexibook)

Rationale of the key positions

Some sentences on why we own these stocks:

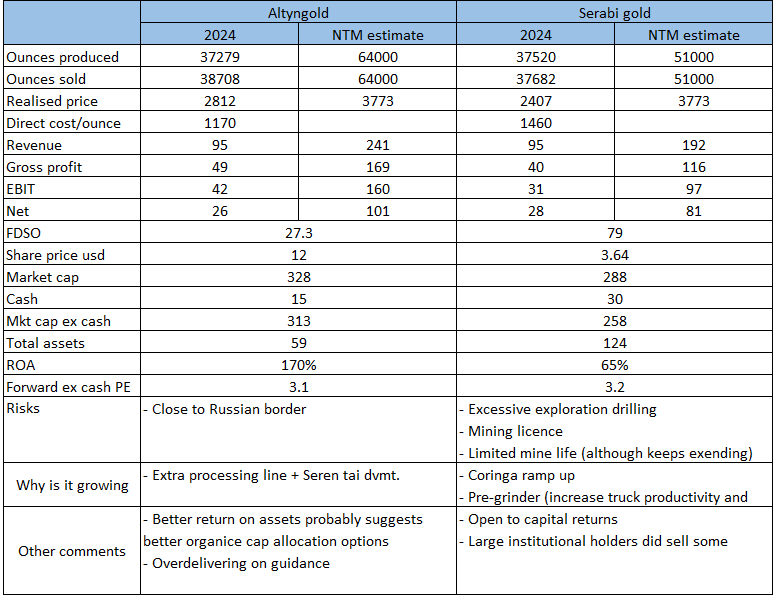

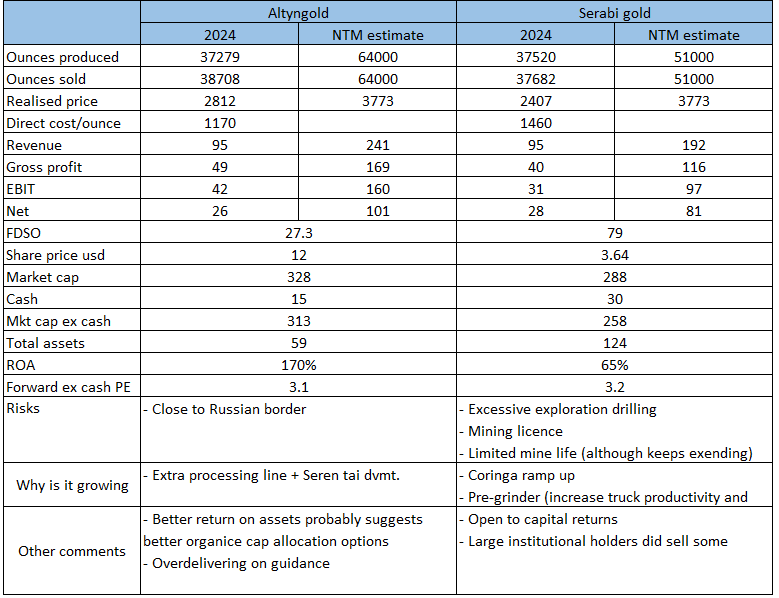

Altyngold & Serabi gold. Two gold miners which saw profitability x10 within a few years, because of the rise in gold price. The market is still adapting to this new reality. Simulation of their next 12 month P&L & ex-cash PE:

Both trade at ~3x NTM earnings based on the current gold price of ~$3850. All numbers in USD. Revenue adjusted for current gold spot price, COGS adjusted for USD vs Brazil real and USD vs Kazakh Tenge moves. Fixed cost increased by 20% because as the companies do well, management will spend a bit more money…

During September, we did a deeper dive and write-up on Serabi and decided to add to the position, because (1) the thesis actually improved as gold prices kept going up and (2) we better understood the licensing risk, the insider sells and life-of-mine risks, giving us the conviction to average up. We will not repeat the thesis but think the hub & spoke model will enable Serabi to expand production in a capital-light way over the coming years, making the stock attractive at a forward PE of ~3x.

Soilbuild was written up in August and has been quite a rocket before and after the write-up. We initially found the stock at 0.95 SGD, at the end of a long day going through ~600 microcaps. We remember walking down the street for a snack thinking: “Their recent contract wins and updated backlog actually imply large revenue growth for this quarter, and for the years to come. How is it possible the stock is not much higher?” After a few more weeks reading about it, it had run to ~1.57 SGD when we finally took our position after stronger than expected earnings. The company still looks incredibly strong just looking at the new project wins they realized in each of the past 8 half-year periods, although the price has run up significantly.

BSH see write-up & earnings update. Still very cheap. The position is limited due to limited liquidity in the stock. We own a bit over 1% of BSH. It’s easy to see that Q3 will be strong as well and will put the stock at 4-5x PE with strong growth.

LGI Homes. US home builder at or near the bottom of the housing cycle, trading at 0.65x book value. This is not our typical investment, because we usually buy growth companies with an attractive income statement. LGIH used to be such a company in the 2021-2022 housing boom, when it was posting 30-40% growth at 7-8x earnings. We sold it there at ~166 USD, because housing is cyclical, and rates had to increase because of inflation… Knowing this, LGIH at 166 USD was priced at ~2x book value, with a commodity-type business putting out unsustainably high growth and earnings figures. Today, LGIH is priced at ~0.66x book, with housing stocks putting out unsustainably low growth and earnings. We think at some point, interest rates will go down, housing affordability will improve and the home builders will return to growth and better valuations. Until that time, we’re happy owning an American home inside a business, at a strong discount not even to its selling price, but to its book value, the cost to build it. This might take a while to turn though.

Moneymax, very cheap pawn broker and jewelry store. Will continue to perform as long as gold does well. (higher gold = higher collateral = higher loan = higher interest income)

Matsa. This Australian gold miner has (1) AngloGold Ashanti looking at buying Lake Carey for ~110m AUD and (2) Gold production from the Devon Pit which started in September 2025, with expected NPV>100m AUD over the next 18 months, and (3) Past tax losses to offset taxes on the production profits and Lake Carey asset sales. After the recent run-up, this still sits at only a 110-120 mAUD market cap (increased for options near/in the money).

DBA Group, cheaper than it looks, growing Italian IT company selling the bad part of their business for a higher multiple than what the overall company trades at. As described in our write-up, they amortize goodwill at 10%, making actual earnings look ~1.5-2m lower than they actually are.

Canaf. Cheap, hated, consistent grower in South African coal. Their Enterprise Value is about 10m CAD, and they put out 0.5-0.7 mCAD in net income every quarter, stacking cash. Discussions on dividends and buybacks are ongoing but unclear for now.

Asiro. Fast-growing (40%) digital platform for lawyers in Japan trading at ~9x 2025 earnings.

Inpro. Same thesis as LGIH although Inpro seems to always trade at ~0.6x book, even while it continues growing and continues putting out solid earnings. This is the less liquid Polish way to play the same housing thesis.

Atlas Pearls. Consistent growth, good management, EPS 5ct and cash 5ct and stock price 20ct.

Zoomd. The momentum continues? Very cheap still and very fast growth consistently since the new CEO (with solid blue-chip experience) came on a few years ago.

NURS. Uber for Nurses seeing high growth in leading operating metrics. The thesis was described many times by others so won’t bore you with it. See their interviews on YouTube.

Silvano. Lingerie maker in Belarus sending bras into the Russian market. Trades at cash + 1x earnings because European brokers turned off the buy button. Still available through XTB on the Polish market, but very illiquid.

16-23: Newer < 1% starter positions in stocks we think are very interesting, but need one more good result to prove themselves, or need further research to understand them. We will likely write a post about one of these but it’s not clear which one. Many others will likely get sold because we didn’t end up liking them enough. The thesis for all of these is mostly the same. Growing fast, cheap valuations, reasons to believe the growth will continue. We’re trying to better understand these growth drivers to decide where to allocate more capital.

Usually what happens is at some point we find a stock we like so much, that we just start comparing it to all the smaller 1% positions, and end up selling them off to add more to our favorite stock. We currently like our top positions a lot, but can’t add more to them because of liquidity, or conviction, or exposure to 1 commodity. This causes the tail of small positions to become a bit longer until the next fat pitch arrives.

Watchlist

Stocks we don’t own but will continue to watch closely:

Singapore: XMH, Thakral, Lincotrade

Poland: Toya, 4Mass, Passus, Yarrl, Rainbow Tours

Spain: Alquiber Quality

France: Robot SA, Catering International & Services

Israel: Sofwave, Libra Insurance

Sweden: I-Tech

Canada: Spectra, Cannara, NTG Clarity

Australia: SKS Technologies

Japan: AsiaQuest

New Zealand: Seeka Ltd, Third Age Health Services Limited

The world already has much more pie charts than needed. On popular request though, below are the allocations and entry prices for the stocks in the portfolio ending Q3:

Mistakes

This was a great Q3, although at some point our 7% allocation to Simply Solventless got cut in half. Incidentally, their auditor did not agree to their accounting policies anymore. We think the problems or required adjustments were quite significant, and we sold it on the ~60% drop the next day, at about 0.20 CAD.

We had been buying this at 0.16-0.68 CAD and took a ~4% portfolio loss on it. We sold the company because we do think (1) management might not be 100% trustworthy, (2) their restated financials are just not as good as they were before the restatements (3) their buy and build approach is broken given the broken credibility (4) Cannabis is a very tough commodity market with few and small moats

The lesson was that a consumer goods company just can’t have >1y COGS in inventory. It just doesn’t make sense to have such a long production and sales cycle, when producing agricultural products, even after factoring in the specific accounting standards applicable to such products. A year in inventory should raise red flags even when inventory includes the growing plants.

Integrating this into our process, we noticed that Inpro and LGIH both have large housing inventories as well (~2x revenue in land, building supplies and finished homes). This is an issue for both companies, but we think it’s more of a temporary, cyclical issue, while with SSC it might be more of a red flag as their products have a limited shelf life.

Summarizing, we further raised the standard of our work this quarter, and regardless of the large inventory numbers in the home building sector, we sleep well knowing we own 1 American home on the balance sheet of LGIH, and 1 Polish apartment on that of Inpro, both priced at a very large discount to replacement value.

Be careful, bull market genius

This was another wonderful quarter. We started writing “returns of x positive quarters in small cap investing” a few years ago, and x just keeps incrementing, now to 15.

Please note that while this did happen and all 15 quarters had positive returns, you should read that as a bit of a joke, because concentrated investing as we do, comes with volatility, and no one should expect having positive results over any short-term period, whether it’s days, weeks, months, quarters or years. We’re all getting fat and happy in 2025 and this is exactly when the market likes to punish investors that stop putting in the work to find and understand the best companies and stocks out there.

Thank you!

Disclaimer

This publication’s authors are not licensed investment professionals. Nothing produced by the Floebertus team should be construed as investment advice. Do your own research and speak to your advisor before taking a position.

That’s a strong conviction in gold!