Review of the 8 write-ups in 2025 (+44% avg)

Dear reader,

Whether you’re a hedge fund manager, a Twitter degenerate, a factory worker on night shift, or my wife… Thank you for reading this!

I did a write-up on a company a few years ago, to get into MicroCapClub. I did it to challenge myself. Writing was difficult for me, but my favorite thing has always been to try to push my own boundaries. By doing it, I found an amazing group of smart people, and I learned how writing can deepen your own understanding and order your mind.

In 2025, writing has become more of a habit, and I put out 8 pitches, covering the companies I like or liked most. Some subscribers have asked for an overview, so they can easily find the write-up that meets their preferences in terms of market cap, liquidity, sector or country. Happy to provide the overview here, as well as current positioning, and a brief summary of each idea.

Overview

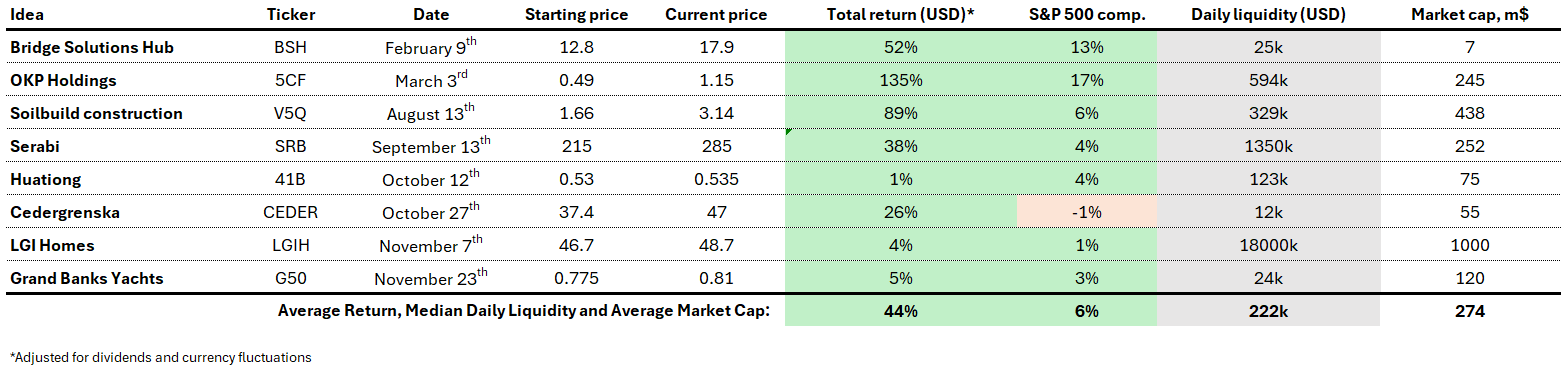

Before we dive in, below is the overview of the 8 ideas covered this year:

The average return was 44% vs 6% for the S&P 500, creating a remarkably large gap in only ~3 months on average since writing. This is not unique. It’s our microcap advantage and the result of working through all the reports to find the diamonds in the rough. The median liquidity is ~222k USD providing several pitches which even our wealthiest subscribers can act on.

I still own all the companies above except OKP Holdings. The goal of this post is to provide an updated point of view on each of them. You can find the links to each of the write-ups at the bottom of this post. At least 7 of them should have no paywall.

Bridge Solutions Hub

I originally bought BSH a couple of years ago after they reported their first quarter of growth and profitability. They bought an asset in April ‘23 and launched a new A/C repair product with it, being profitable in Q3 and achieving triple-digit growth. That’s a crazy achievement from April to Q3!

With some months over the winter to professionalize things and get into more sales and distribution channels, it was clear they would report much stronger growth and profits in 2024.

Buying the stock was horrible. At that time you had to make a Polish XTB account as IBKR didn’t have it yet. I bought 5 kEUR of the stock making it rise from 4 to 5 PLN, and patiently tried to get more but didn’t get much.

In 2024 and 2025, BSH delivered double-digit growth and their profits grew from 0.4 mPLN in 2023 to 5.4 mPLN in the past 12 months. Strong earnings often gave an opportunity to add at 5-6 P/E multiples.

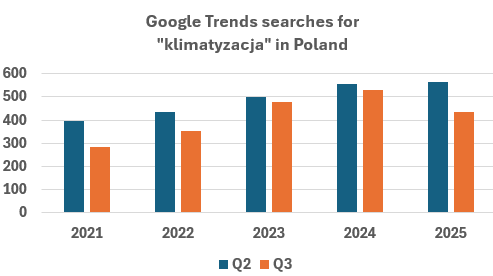

I still own BSH and have increased my position to ~1% of the company. Earnings for Q3 came in at 26% revenue and profit growth, putting the stock at an ~5.5x P/E. I had expected a weaker Q3 as the summer in Poland was a bit less warm than usual, leading people to search for “air-conditioning” 18% less in Q3:

The write-up came at a strange time in February, when insiders sold the stock down from 19 PLN to 12 PLN to cash out. My perception at that time was that these were people close to the original founders of BSH. They started BSH as an outdoor advertising company, before it got disrupted to become the product-driven company it is now. They didn’t have a relationship with the business anymore, and wanted to get out in February to do something else with their money, rather than wait until August 15th for the Q2 earnings report. They made ~10x on their initial investment and wanted out. That odd insider sale created the opportunity at ~13 PLN. Today at ~18 PLN though, BSH is still very cheap at 5x earnings with 26% growth.

The question for the year ahead is whether they keep the growth trend, or retailers try to copy them with private label brands, getting into a position to negotiate discounts from BSH, eating into their margins. Looking online, the top two products I would buy today to replenish the car air-conditioning are both from BSH, so the competitive position still looks good. It will be interesting to see if growth inflects higher than 26% again, when we get a warm Q2 or Q3 next year.

OKP Holdings

So we just talked about Polish people looking for the word “air-conditioning” in Polish on Google… Am I Polish? No, but I did make some Polish friends over the past years.

It’s kind of crazy to move top-down all the way from screening through the universe of 100,000 stocks, narrowing down to one stock, just to then dig so deep into Google searches, product reviews, employer reviews, and other bottom up work to become the biggest/smartest geek on the stock out there. I love that aspect of MicroCap investing.

Taking that up a notch, earlier this year, I built a Python script that scans through the 200 most recently awarded Singaporean tenders every 5 minutes all the time, and sends me an email when a tender larger than 20 mSGD gets awarded.

I built this after discovering OKP, which was a Singaporean construction company coming out of years of struggles after a lethal work accident and the resulting lawsuits.

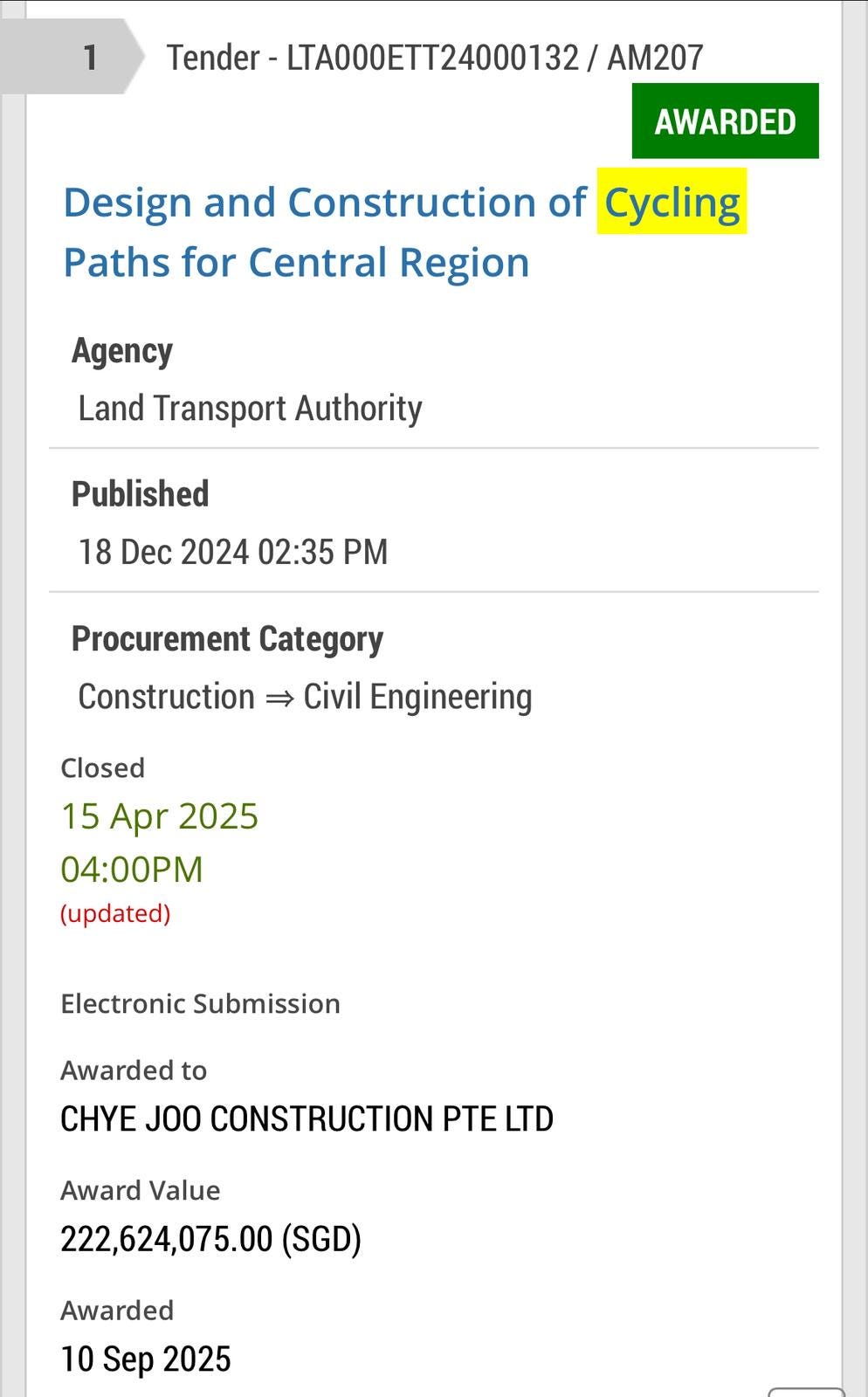

The company won 3/4 government tenders for cycling paths, something the Singaporean government is extremely serious about. They want to build thousands of kilometers of new cycling paths across Singapore. They even got Dutch engineers to come to Singapore to give their opinion on the design and planning aspects of the project, which is a key priority for the Singaporean Land & Transport Authority.

Not only did these contract wins give OKP a nice backlog and 20% growth, the company also had its entire market cap in cash, and was bidding on projects that would 3x their revenue overnight…

I talked to their CFO and Executive Director in the summer, who told me they don’t use bikes themselves, because they drive to 5-12 of their work sites every day to track productivity and safety. They even implemented a tracking app that shows the CEO how much concrete each of the crews pours every hour, on his phone. This is an exceptional management team, very engaged, passionate and very kind.

Meeting them made it a bit saddening to sell the stock a few months later, when the thesis broke. They lost their big ambitious tenders, making the future of the company less clear, and causing me to exit the stock. OKP with their management team will do great, but I had to get out.

I sold OKP at a ~135% gain, when the below Tender was Awarded to Chye Joo, and was communicated on the Gebiz website on about September 15th. The stock didn’t move and has not done much since, just because of how cheap it is and how no one cares about lost tenders.

Soilbuild Construction

If it hadn’t been for the great interview with OKP’s management, I might have invested more or earlier in Soilbuild. Before I finally bought this and wrote about it, it was already up 60-70% in 1-2 months, after winning a large private sector tender.

It’s interesting that Singaporean companies, when they win a large tender, they announce the win, but they also announce their resulting net order book at the time of the win. This gives you future revenue visibility, but also current quarter revenue visibility, as the new order book figure implies the amount of booked revenue (going out of the order book).

Anyway, when Soilbuild had that big win, just the day after, I looked through 800 companies, and I thought well, that’s such a massive win, and the net order book implies ~50% growth in the current half year already, and this trades at single-digit P/E. That’s kind of crazy.

My head was fried from screening through so many companies though, so I decided I was going to read all their filings in the next week, to understand what was wrong with them, or what I was missing. The stock then went up ~50% in a couple of days. I did still do the work on them but was struggling to buy the pop…

They reported H1 earnings mid-August, with revenue up almost 2x and profits about 4x. Looking at the report after hours, I knew I was going to stay up all night buying the stock in Singapore, and making a write-up about it.

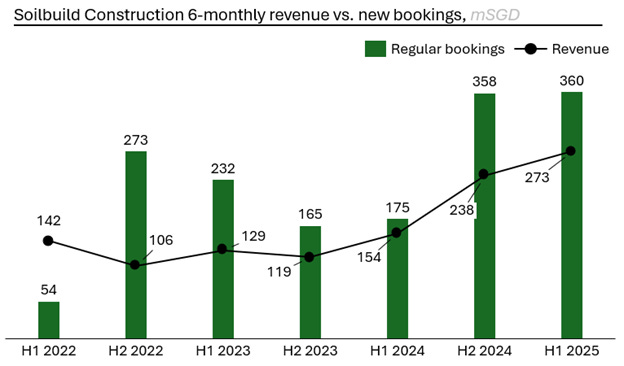

From there it doubled in about 2 months, and then gave back a bit. I have sold a bit around 3.40 SGD but keep part of the position. There are a lot of cheap growing construction companies in Singapore, but I think Soilbuild Construction is doing best in terms of digitalization and sales, driving their order book up massively. Notice how high new sales bookings are compared to revenue booked:

This chart even excludes their largest one-off contract win earlier this year.

Serabi Gold

In May this year, I had a surgery that didn’t really work well initially. It’s fine now but I basically couldn’t eat anything except plain vanilla ice cream for about 8 weeks. I still have 16 liters of that if anyone wants them, as I can’t enjoy that anymore. Anyway, at some point during this time, I had 2 days where I was feeling pretty good, probably because I had just mixed a full Neapolitan pizza converting it into a 100% drinkable liquid fuel. I got out of bed and the first thing I wanted to do was to screen through companies and find something new.

I then found AltynGold and Serabi Gold. Two companies that had been popping up on the screen for months, but I didn’t really look at, because I always hated mining stocks. When I was 16, I put my savings into junior mining stocks, which seemed to have dilutive rights offerings every Monday afternoon. They declined 90%, causing my first car to be a 12-year old Ford rather than a 5-year old Audi…These days, things have changed a bit for mining stocks though, at least temporarily.

What is special about Altyn and Serabi, is that the market just could not (and cannot) keep up with the progress they were making. I already wrote about this in the December portfolio update, but these companies are doubling production, while the gold price has also doubled… This is leading to 3-4x higher revenue on a 30-40% higher cost base, resulting in 10-15x higher net profit…

Nobody wants to see their gold mining allocation go up 15x, so people have been selling these into the market, creating a drag on the price and the multiple, and frankly giving late joiners like me a free ride.

In August, Ian Cassel wrote up one of these stocks, and I read the pitch and thought, “ok he is seeing what I am seeing, but I like my 2 gold stocks better, even after the run-up they have had…”

So I wrote up Serabi gold at that point. Serabi is a risky stock with a very large potential upside, interesting even for those who are not bullish on gold. Both AltynGold and Serabi continue to be my top positions, and I have added a bit more to both since the write-up.

As these stocks keep rallying, I’m trying to not rebalance out of them at the current 2-3x forward P/E multiples they trade at, but this is becoming more and more difficult as they become such a large part of the portfolio. A problem everyone in mining stocks is facing, which is exactly why the opportunity exists.

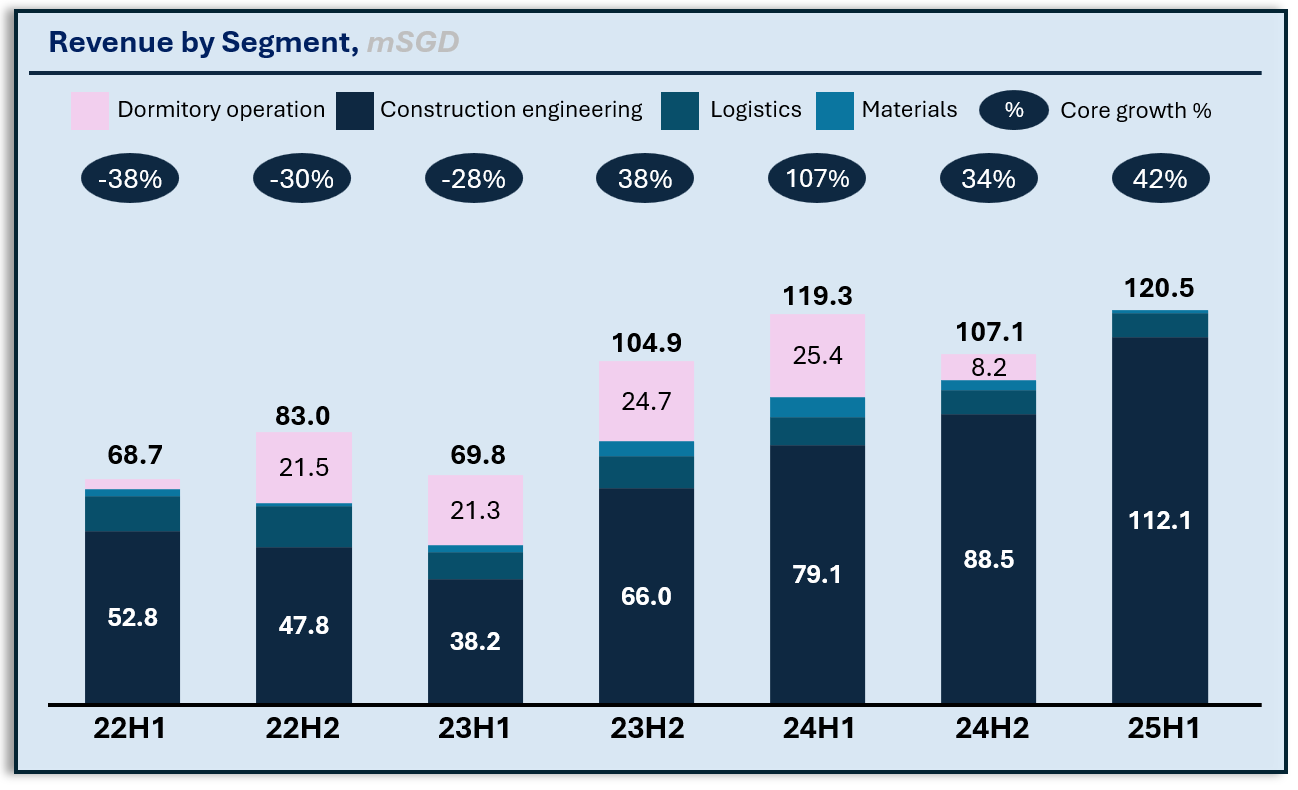

Huationg Global

When I wrote about OKP, someone asked me why I didn’t own Huationg, because they were even cheaper. I agreed but explained the attractive OKP tender pipeline. I also noticed that Huationg was going to lose revenue from their highly profitable dormitory management contract, which was responsible for the majority of their profits.

I was hoping for this contract loss to show up as a revenue drop in the H1 2025 results, and to buy Huationg on the dip for their strong construction business.

The construction business however, did so well in H1, that it completely compensated for the lost dormitory revenue.

I bought Huationg in August and described in the write-up how the ~40% growth in the core construction business, is hidden behind the disappearing dormitory business:

Still today, Huationg is very cheap with more cash than its market cap (half offset by contract liabilities, but still), having a backlog above 500 mSGD. Just compare that to the current revenues shown above, and note that they have their next 2-3 years of great results already contracted.

Huationg is a less shiny business than Soilbuild or even OKP. They do ground excavation type work, and some tactical engineering work, rather than the end to end design of large buildings or the management of infrastructure projects interfacing with 6 levels of government…

But Huationg is delivering very strong results and is very cheap. The stock is taking some rest here after the 3x in the past year, but it still has a lot of work lined up for it, so I still own it.

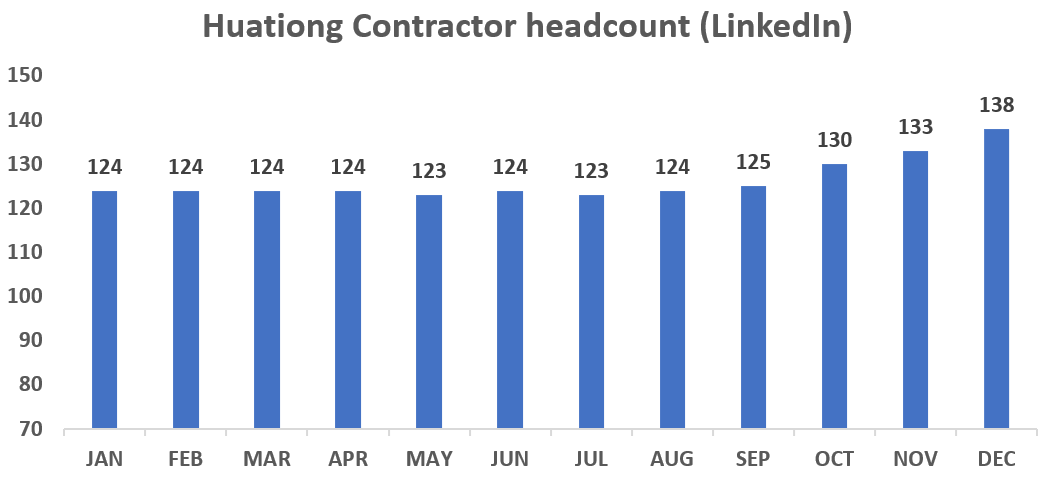

Recent headcount figures on LinkedIn indicate continued growth in H2, as can be expected from the backlog:

This is only a small subset of Huationg’s employees, as most workers don’t have a LinkedIn account, but it still provides a great KPI to track besides the order book evolution.

Cedergrenska AB

There are some stocks out there, that just have such an odd name that they just have to be cheap. This was the case with Vilkyškių Pieninė a few years ago, and it’s also the case with Cedergrenska AB. It just sounds like a Danish taxi company or something. Not exactly as fancy as Spyrosoft.

Like most of the companies above, Cedergrenska is the growing result of a strong founder, having a vision and executing well for several years in a row.

When I look at an interview with Niklas Pålsson, I want to be in the boat with this guy. Great vision, but more importantly great energy and storytelling, which I’m sure works well to create a strong culture.

If you don’t speak Swedish, it’s possible to turn on subtitles in your favorite language. First turn them on in Swedish, then use the settings wheel again to auto-translate them to your preferred language.

Cedergrenska is a Swedish private school group, that has grown through acquisition and operational excellence, professionalizing schools and building strong central support functions (for IT, facility management, canteen, … )

This company is also very cheap but plays on an uncertain regulatory field. It can easily be seen as the most risky company written up. Locals gave a lot of push-back to the pitch, saying politicians are already planning to ban the whole sector.

I did read these political opinions, but I don’t think it will be that bad. Unfortunately, and in this case fortunately, politicians don’t always implement everything they talk about. The reality is that Cedergrenska, before adding back goodwill amortization, makes less than 3 million USD annual net profit per year, bringing high quality education to ~10,000 students. I just don’t think governments will want to hurt their education sector, nor think they can do it better themselves.

Since the write-up we had some positive news with a debt-funded acquisition making the company ~8% bigger, and some negative news with the founders selling 2-3% stock to “improve liquidity”.

I still like and own the company and have also added a tiny position in Tellus Gruppen, a smaller company with a similar approach as Cedergrenska, trading at 3x net income + amortization a few weeks ago.

LGI Homes

The write-up on LGI is just about a month ago, so it’s too early to look at the scoreboard for how it did. The stock is up a bit though, so we might just act like it doesn’t matter and take the win.

Seriously though, LGI Homes was a bit of a different write-up. I bought this company once in 2020 or 2021 when it met my typical criteria of single-digit P/E multiple, and double digit growth over several years. Sold it in 2021 when it traded at 3x book value and it became clear that interest rates were going to have to go up a lot for a long time.

Since then, I kept looking at LGI and a few other builders, thinking I would like to once buy a home builder for less than its book value. These companies not only perform very well over time, since the 2005-2007 housing and financial crisis, their risks are highly overestimated by the market.

The home-builders trade at single-digit P/E multiples, as if the next US debt crisis will lead to austerity, creating a new housing crisis… In reality, we have learned during COVID, that when bad things happen in the economy, we turn on the fiscal and the monetary stimulus machine to create a way out. This thinking made the 2020 crisis much better than the 2008 crisis. (which ultimately was “solved” in the same way)

We can agree/disagree with the governments and central banks, on the merits of the stimulus approach to resolving crisis, but we have to be clear that this will be their approach when the next crisis hits, and this makes the probability of a large housing/credit crisis much lower at least in the next 5-10 years.

By November 2025, LGIH had traded down to ~50% of its book value, with limited leverage and a book of American residential construction land and homes. This is quite unique and presents an “easy double” in my personal non-investment advice view.

The company reported improving sales bookings in their Q3 call, which so far marked the bottom in the stock, providing the last reason I needed to make a write-up about it.

There is no catalyst here, so it will take time for the thesis to play out, making it different from my other ideas this year. I like the safety I perceive in LGIH and I have added to the position after the write-up.

Grand Banks Yachts

Finally, the most recent write-up I did was on Grand Banks. When I posted it for MicroCapClub, they asked me if I saw Iqbal’s write-up on it, which I hadn’t. Iqbal had written about the company ~ 2 months before me. If you don’t know him, I recommend following him on the bird app on “Iqbal_yusuf1994”.

I mentioned sales bookings vs. revenue above, when looking at Soilbuild. It is important here as well. I decided to write about Grand Banks Yachts after seeing their large updated backlog in their Q4 press release, which implies massive Q4 sales orders.

The high orders are likely the result of hiring a new Chief Marketing Officer, together with several other operational, commercial and strategic initiatives highlighted in the write-up about this company.

This company had almost 100% higher sales orders in 2025 vs 2024, but yes, you guessed it, it still trades at a single-digit P/E multiple in Singapore.

Summary

It was great searching companies in 2025. I found some interesting situations and had fun sharing them with you and discussing them in the chat. In 2026, the market will likely be more difficult, and so I look forward to search harder and potentially find even better companies. Below is link to the write-ups mentioned above:

Bridge Solutions Hub:

OKP Holdings:

Cycling higher

SummaryThis Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.

Soilbuild Construction:

LGI Homes

Today’s write-up covers a company we have been following for several years, and is highly misunderstood by the market today.

Grand Banks Yachts:

Small compounder at 6x earnings, hiding a potential 110% in future growth

Today’s write-up covers a company with unique characteristics:

Disclaimer

This publication’s authors are not licensed investment professionals. Nothing produced by Floebertus should be construed as investment advice. Investing involves serious risks, including risk of capital. Do your own research before investing, and size your positions appropriately, in line with your own conviction and your own knowledge.

Brazil Freezes Mining Rights Auctions & Serabi Gold's Permitted Production Advantage

https://www.cruxinvestor.com/posts/brazil-freezes-mining-rights-auctions-serabi-golds-permitted-production-advantage

You mentioned getting into MicroCapClub. Do you also find ValueInvestorsClub useful? Homebuilders that aren't small caps, such as LGIH, have some high quality writeups on there.