Grand Banks Yachts (G50.SI)

Why we think the company has a long growth runway ahead

Today’s write-up covers a company with unique characteristics:

9 years of profitability in a cyclical sector

15% average growth since 2015

Hidden 100%+ growth in new orders in FY25

(Implied within revenue and backlog numbers)Growing while competitors decline

Reducing its own cyclicality

< 6x cash adjusted P/E

~20% ROIC

We watched this company since 2022, but new bookings and backlog evolution always kept us away. Recently, the CEO’s targeted actions led to explosive growth in new orders, increasing 110% over 2025, and 175% in H2 2025 (!!).

This is why, today we wanted to dive in with you!

Grand Banks Yachts

Ticker: G50 (SGX)

Price: SGD 0.775

FDSO: 190m (incl. 4m dilutive employee options)

Market Cap: SGD 147m (USD 113m)

Overview

Grand Banks Yachts is a company that builds and sells yachts under the Grand Banks, Eastbay and Palm Beach brands. The company is interesting because it:

Grew revenue from 39 mSGD to 162mSGD in the past 10 years led by CEO Mark Richards

Is expanding sales efforts in the USA and Europe, leading to 110% order growth in 2025, (also enabled by its recently expanded and optimized Malaysian production facility)

Trades at less than 6x earnings + cash, with ~35% gross margins

We cover a quick intro to the history and focus of the company, dive into the 3 points above, come up with a price target, and summarize after talking about the risks.

History & focus

Grand Banks Yachts was founded in 1956 as “American Marine”. The company in 1963 built the “Grand Banks 36” Yacht, which was the first trawler type yacht.

The boat was unique because of its shape, which is rather flat on the bottom, behind the sharp nose. This makes the boat sit less deep in the water, reducing its water contact surface and making it much more fuel efficient, and more stable or comfortable at sea.

This idea of creating a long range, slightly slower boat, intended for couples wanting to go on a comfortable trip at sea, was an innovation in boat design, and is still part of the company’s value proposition today.

Not spending too much time on the history, it’s further important to note that Grand Banks in 2014 acquired Palm Beach Motor Yachts, an Australian competitor who had started building similar trawler style yachts.

As of the acquisition, the Palm Beach CEO Mark Richards took over the CEO role of the entire Grand Banks company, leading it for the past 10 years. Mr. Richards is an excellent manager both on the operations and on the sales side, and he has contributed everything Grand Banks is doing today. Below is a recent interview showing his mindset on operations as well as sales.

An alternative (realistic) way to look at the acquisition, is that in 2012 the original Grand Banks was struggling and organized a refinancing with Malaysian billionaire Lim Kok Thay, who obtained 30% of the companies shares. As things didn’t turn around by 2014, he contacted Mark Richards of Palm Beach, and brought him in to turn around the company, while keeping the iconic Grand Banks name, given the heritage.

Past 10-year growth story

As mentioned, Mark Richards came in in 2014. He re-organized the factory in Malaysia to make it profitable and capable of producing the whole range of yachts of the combined Grand Banks and Palm Beach entity. The company even decided to produce less for a year, to focus on re-organizing the yacht designs and the factory operations, still retaining the same crew size, but setting up a better production model. Reading between the lines of the 2015 report, it sounds like Mark and his team also just replaced many of the management and workers to create a new way of working. After driving production improvements, Mark turned to the sales and product design side driving the company forward as a whole.

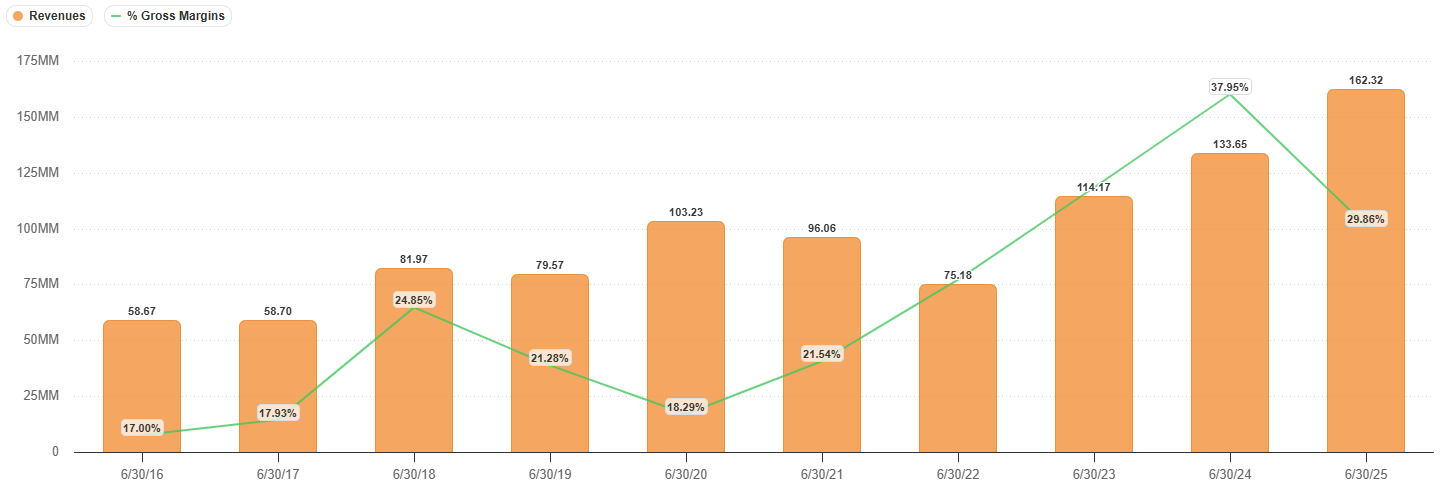

In the 10 years, since turning the ship around, Grand Banks Yachts under Mark’s leadership has grown ~15% per year while making profit every year after the turn-around.

Notice how the company struggled in 2021 and 2022. This is unusual for a boat/ship building company, because in 2020/2021, COVID created large demand for yachts, which lead to strong 21 and 22 revenues. In Singapore and Malaysia though, severe COVID shutdowns and travel restrictions were in place, that made it impossible for Grand Banks factory to produce during several months.

We see that in 2023 and 2024 the order backlog built up during the COVID years, is finally processed into actual deliveries and revenues. The same happens at other boat/ship builders like Catana or San Lorenzo, although slightly earlier.

Given the large 2021 demand spike, followed by a weaker economic/financial environment, many of the ship builders have been using up their order backlog. This created a situation where their stocks are very cheap, but are value traps. The companies are sitting on expanded factories that are slowly becoming idle due to sinking demand.

Look at Catana for example, a European Catamaran builder of similar size to GBY. Here’s what Catana says about their sales backlog:

Catana (~200mEUR revenue) has basically built a massive orderbook in the 2020 and 2021 heydays, and has then completely lost touch with its customers, while slowly delivering those orders. This leads to them now having ~20% less revenue than last year, while being unable to achieve a stabilization in the orderbook. In 2023, the company acquired a Portuguese motorboat production company, a move that created more trouble for the company, as it targets cyclical or price-sensitive customers.

We don’t blame Catana, it’s in fact an interesting company to follow, but it seems to have been trapped in a capacity overbuild, as many players have. We expected this to happen to Grand Banks Yachts as well, but the opposite actually started happening over the past couple of quarters.

Expanding sales efforts in the US and Europe, leading to 110% order growth in 2025

Grand Banks Yachts has taken excellent steps over the past years:

Strategically:

Merged Grand Banks and Palm Beach organizations and brands, coming out together as “Grand Banks and Palm Beach Motor Yachts”

Introduced larger ships (Grand Banks 85 in 2021/2022 and Palm Beach 85 in 2024/2025) which target less price-sensitive / macro-sensitive consumers

Commercially:

Increased physical US sales and service presence

2022: Purchased a marina in Florida

2024: Established a San Diego sales & service center

2025: Purchased a large marina in Rhode Island

Planned to increase presence in Europe through…

2026 upcoming San Remo sales and service center (recently announced)

Assigned a global CMO, Lynn Fisher, who previously worked as CMO at Vista, a private jet company

Operationally (all in 2025):

Expanded floor capacity by 25% at the Malaysian factory

Increased manufacturing efficiency by introducing robots in the new plant

Streamlined production steps & reduced energy costs through solar panels

Strategic focus

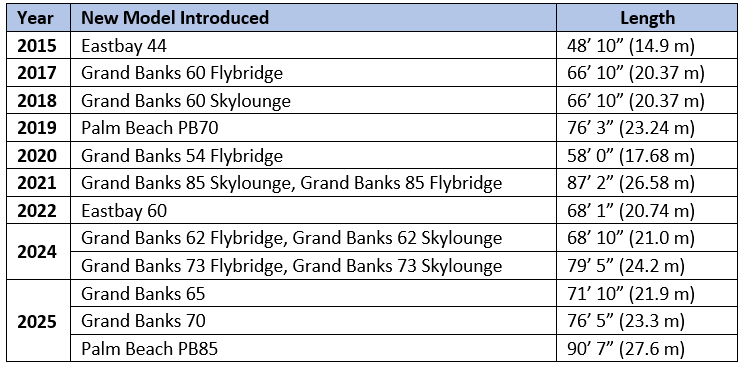

Throughout its growth journey, Grand Banks has continually expanded its product range, including increasingly larger yachts. Demand for larger ~20m+ long yachts bought by centimillionaires or billionaires, is much less cyclical than demand for smaller trawler yachts bought by millionaires. This is just like Hermès demand being much less cyclical than LVMH’s.

As Grand Banks production and design capabilities grew over the past decade, so did the max size of their yachts, gradually providing an entry in the more stable super yacht market.

Below table shows the gradual increase in Yacht sizes announced by Grand Banks Yachts:

They are slowly entering the super-yacht segment of less price-sensitive consumers.

Operational Excellence

Meanwhile, continuous improvement at the Malaysian production facilities, makes Grand Banks production more efficient over time, supporting gross margins of ~30-35%, driven by economies of scale creating labor efficiency.

Margins in 2025 came down a bit because of a higher mix of trade-in vs new construction, new construction GMs still being 36%. This was slightly lower than 2024 due to lower USD/MYR exchange rates.

Commercial Excellence

The commercial initiatives listed in the overview above, complement the operational and strategic initiatives. Grand Banks through its marinas and service centers, is getting closer to US customers, better positioned to hear their feedback, to support them with maintenance, and to help them consider a new ship purchase.

This is why, contrary to most boat/ship builders, Grand Banks Yachts sales team has been on fire this year. The company signed 199 mSGD in new orders, over 2x higher than prior years, and in particular signed 142 mSGD in yachts in the past 6 months, which was about as much as the 6 quarters before that, combined.

The momentum seems to continue into 2026. Mark Richards at the Annual Meeting in August 2025, mentioned:

“The Group is looking to accelerate the construction of larger boats to meet the growing demand for big yachts. Reflecting the strong demand, the Group is currently undergoing negotiations for seven PB85 contracts and expects the GT70 and GB73 to be the next major additions to its large yacht line up.“

These PB85’s are ships priced at ~9 mUSD each, so if only half of them lead to orders, and nothing else happens, Grand Banks Yachts sales team is off to a strong start of FY26.

Source: https://links.sgx.com/FileOpen/Minutes_of_AGM_2025.ashx?App=Announcement&FileID=867608

Valuation

Grand Banks Yachts trades at a 147 mSGD market cap, taking into account both outstanding shares and dilutive employee share options and grants. The company has a cash position of 47 mSGD, on which it earns ~1 mSGD per year. Removing cash from market cap, and interest income from the earnings, Grand Banks Yachts trades at:

Cash-adjusted P/E = (mkt cap – cash) / (net income – interest income)

= (147 - 47) / (18 - 1)

= ~ 6x earnings

We estimate Grand Banks Yachts revenue will be up ~22% in 2026, driven by a 30% higher orderbook to start the year. Gross margins will likely be a bit lower, caused by exchange rates, and a slightly higher contribution of repairs and trade-ins revenue. Net income margin % will likely be similar to 2025, driven by beneficial fixed cost leverage. This drives our 2026 earnings estimate of ~22 mSGD. (18 +22%). Taking out 1m interest income, we work with 21 mSGD cash adjusted earnings.

It’s hard to put a multiple on the company, as comparable companies trade anywhere from 10x to 65x earnings, mainly depending on size, growth stability, and size of boats/ships produced (which affects margins and competitive advantage in general).

At 10-12x cash adjusted forward P/E, we find a value at which Grand Banks Yachts can still be considered cheap. This drives a market cap of 47 + [10 to 12] x 21 = 257 – 300 m SGD, or a share price of 1.35 – 1.58 SGD.

Risks

There are 2 key risks to this idea:

Margins. Grand Banks Yachts is currently earning ~35% gross margins, higher than in pre-covid years, and higher than most competitors. We think this is the result of running an efficient, well-utilized, cheap production facility in Malaysia, and creating yachts with a unique value proposition. There’s a risk of gross margins coming down, due to overcapacity at competitors’ driving price decreases, or less optimal factory utilization as Grand Banks grows, or any other reason. Inflation can also affect margins, particularly because the company commits to build the yacht before building it, so any inflation between signing and building the yacht goes straight out of gross margins.

Macro/demand. Demand for yachts may fall driven by a global recession or by increasing interest rates. We think this risk is already partially affecting Grand Banks Yachts, driving their focus to larger ships purchased by more affluent less price or macro sensitive customers. A declining global economy and stock market though, would certainly further affect Grand Banks’ demand.

We made this a small starter position in our own portfolio, as we find these risks hard to rule out (hard to judge if margin follows from great execution or shorter term benefits). When the company shows consistency in order growth and high margin execution, we look forward to buying more shares higher.

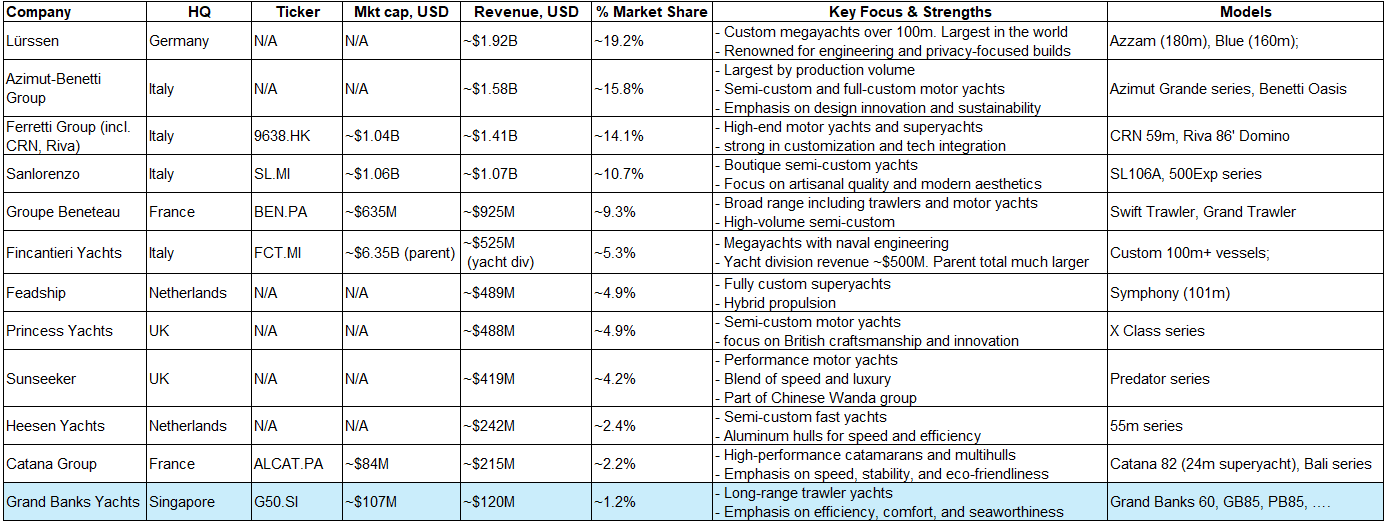

Other players

Here’s a quick overview of the players in the recreational boat/ship market, which is a market of ~9 bUSD per year, expected to grow 6-7% from 2025 to 2032, driven by increasing wealth concentration. (K shaped economy at work).

Catana, is mentioned is interesting to watch but might have to go down deeper or consolidate for a few years before turning around.

Ownership structure

Grand banks Yachts has ~7% insider ownership, almost all of which are held by the CEO. Other investors include billionaire Kok Lim who is not involved in the management of the company, and 2 other investors who are not involved in the day-to-day of the company. The company has a healthy free float providing

~50 kSGD in daily liquidity.

Summary

Grand Banks Yachts is a solid compounder, which under the leadership of Mark Richards has grown revenue over 4x in the past 10 years.

The company had strong new order inflow in 2025 as a result of well-targeted commercial efforts, a factory expansion, and continued addition of larger ships.

The near-term outlook looks positive, given a strong orderbook and ongoing sales of 7 PB85 ships providing visibility on short-term growth.

We think the shares look attractive at 6x earnings + cash and are undervalued at 0.775 SGD s a fair value range of 1.41-1.63 SGD per share. Main risks to watch are margin sustainability and global macro affecting demand for discretionary spending.

Disclosure

We own shares in Grand Banks Yachts (G50.SI) and may buy/sell shares at any time.

Disclaimer

This publication’s authors are not licensed investment professionals. Nothing produced by the Floebertus team should be construed as investment advice. Investing involves serious risks, including risk of capital. Do your own research before investing, and size your positions appropriately, in line with your own conviction and your own knowledge.

Appendix: Review of the 2021 launched Grand Banks 85 yacht, the largest ship produced by Grand Banks until the launch of their Palm Beach 85 model this year.

Hi Floe, this is a very interesting pick.I work in this sector(in one of the competitors), it is a very though industry, infact we have the division but we are loosing money on that so far.It is difficult to study the company because on their web site I can't find anything, where were you able to look at their documentation?Usually their orders growth is anticipated by a lot of hiring people activity but I cannot find anyhting on Linkedin for them...